How To Build A 5-Year Investment Plan That Actually Works?

As of July 2025, the total mutual fund investment in FY 2025-26 through SIP stood at INR 1,09,053 crores1. Despite this growing investment landscape, the fiscal discourse is often skewed heavily towards short-term vs long-term investments. However, medium-term plans, such as a 5-year investment plan, are equally important, as they bridge the gap between the high liquidity provided by short-term investments and the exponential growth prospects of long-term investing.

Therefore, for all investors who wish to get the best of both worlds and create a portfolio that gives liquidity and growth, this deep dive into short to medium-term investments is a must-read.

Best 5-Year Investment Options In India For Medium-Term Investment

Goal-based investing in India is incomplete without dedicating a suitable investment portfolio to medium-term investments, like a 5-year investment plan. Therefore, let’s explore the various categories of investment and their performance over the medium term.

A. Fixed-Income Investments For Medium Term

While Indian markets witness participation from a wide range of investors, with different fiscal goals and financial temperaments, the need for passive income generation and high-return, low-risk investments in India is substantial. Therefore, discussed below are some popular fixed-income investment options.

1. Bond Investment: A debt security that generates fixed returns, in the form of an interest rate or coupon rate, is called a bond. Being a debt instrument, they are lower in risk compared to equity or market-linked securities. Moreover, they have regular interest payouts. Bond investments for short-term or long-term are not the only option available. We can choose bonds for medium-term as well.

For instance, suppose Mr A invests INR 1,00,000 in 12% bonds for 5 years. His total payout after 5 years would be INR 60,000.

The table below shows some key features of bonds listed on Grip Invest.

Particulars | Description |

Yield to Maturity (YTM) | Up to 14% |

Repayment | Periodic - Monthly, Semi-Annually, Annually |

Risk | Low to medium (Only investment-grade bonds are available on Grip) |

Inflation Protection | Yes |

Security Cover | Yes |

For example, Keertana Finserv is a bond on Grip that offers up to 12.85% YTM.

Also Read: Is Putting Rs.50k In FD for 10 Years Worth It?

2. Securitised Debt Instruments (SDIs): SDIs are the debt instruments that let you invest in a pool of loans. There are interest-bearing assets that are pooled together and converted into tradable securities by a special purpose vehicle (SPV) appointed by SEBI. These underlying assets can be loans, invoices, or lease receivables. All these SDIs are rated by independent credit rating agencies and are regulated by the SEBI/RBI.

For instance, LoanX by Grip is an SDI that enables you to invest in a pool of loans offered by the NBFCs in India. Thousands of loans are analysed, and high-quality loans are pooled together to form this SEBI/RBI-compliant LoanX product. LoanX offers up to 14% fixed returns to the investors and is manageable in a demat account.

The table below shows some key highlights of the best SDIs for 5 years, available on Grip.

Particulars | LoanX | InvoiceX |

Return | Up to 14% | 10% to 14% |

Regulated | RBI and SEBI | RBI and SEBI |

Rating | AAA to BBB | A2 to A1+ |

Security Cover | Yes | Yes |

Diversification | High | High |

The InvoiceX opportunity is usually of 6-9 months tenure, therefore offering high liquidity. LoanX opportunities come with a range of tenures starting from 6 months to 5 years. Therefore, LoanX can be a good fit in your 5-year investment plan for earning stable fixed returns.

Apart from debt securities, other alternative investment platforms can fit into the 5-year investment plan of certain investors. Let’s explore them as well, beginning with mutual funds.

B. Balanced Mutual Funds

Investors are aware that mutual funds invest a pool into a range of assets. However, for some mutual fund categories, the diversification is done within a particular asset class. For instance, according to the SEBI mutual fund categorisation, small-cap equity mutual funds need to invest at least 65% of their pool into small-cap stocks2.

In such a scenario, balanced mutual funds offer investors a diversified blend across investment types. For instance, the table below shows the asset allocation and anticipated return from one of the best mutual funds for 5 years, called balanced hybrid funds, which are a type of balanced mutual fund.

Particular | Minimum % allocation of portfolio |

Equity and related assets | Between 40% and 60% |

Debt | Between 40% and 60% |

| The category average return of this 5-year investment plan is 13.33% | |

Source: Morning Star

C. Real Estate

Often, investors consider real estate as a long-term investment medium suitable for investors with a high investment corpus. However, thanks to the Real Estate Investment Trusts or REITs, real estate investment has become a possibility for medium-term investors with limited funds. REITs allow deriving both fixed income in the form of rental yield distributed among investors and capital gain by trading REIT units.

REITs pool the funds of individual investors and invest in commercial properties that are rented out. According to guidelines, at least 90% of distributable surplus has to be distributed among the unitholders3.

Let us now look at some actual 5-year investment plans for safe investment options in India.

Example Of A Realistic 5-Year Investment Strategy

Two key aspects must be considered by investors to optimise their 5-year investment plan. Today, investors can easily utilise the SIP returns calculator for 5 years to customise their investment strategy.

1. SIP-Based Approach

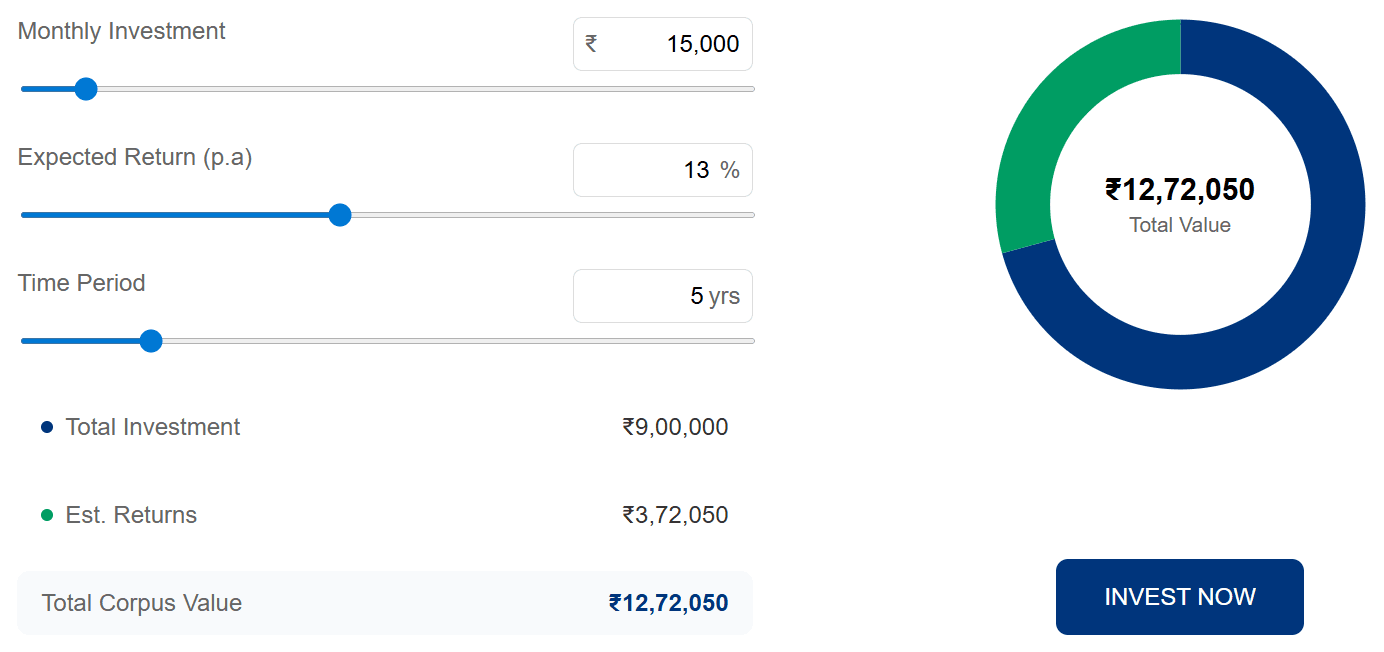

If Mr A invested INR 15,000 per month in a mutual fund through SIP for 5 years. Assuming a return of around 13%, he can generate a total corpus of INR 12,72,050.

Grip SIP Return Calculator for 5 years

But a portfolio creation should not only be done based on the amount of return an investor wishes to generate after a tenure. The asset allocation and portfolio diversification should also be maintained to control the risk.

2. Rebalancing Yearly

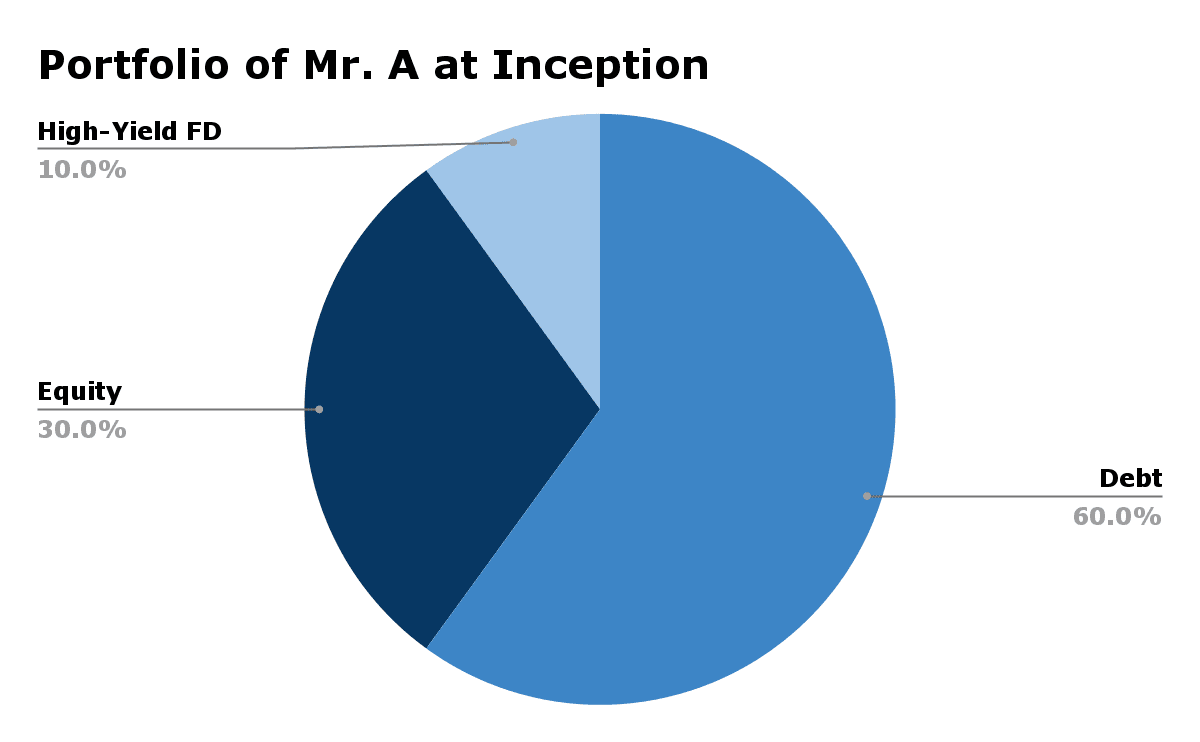

Suppose the same Mr A is a 53-year-old retired man. Therefore, he prioritises liquidity and security over growth. Hence, 60% of his portfolio is invested in debt instruments, 30% in equity, and 10% in high-yield FDs.

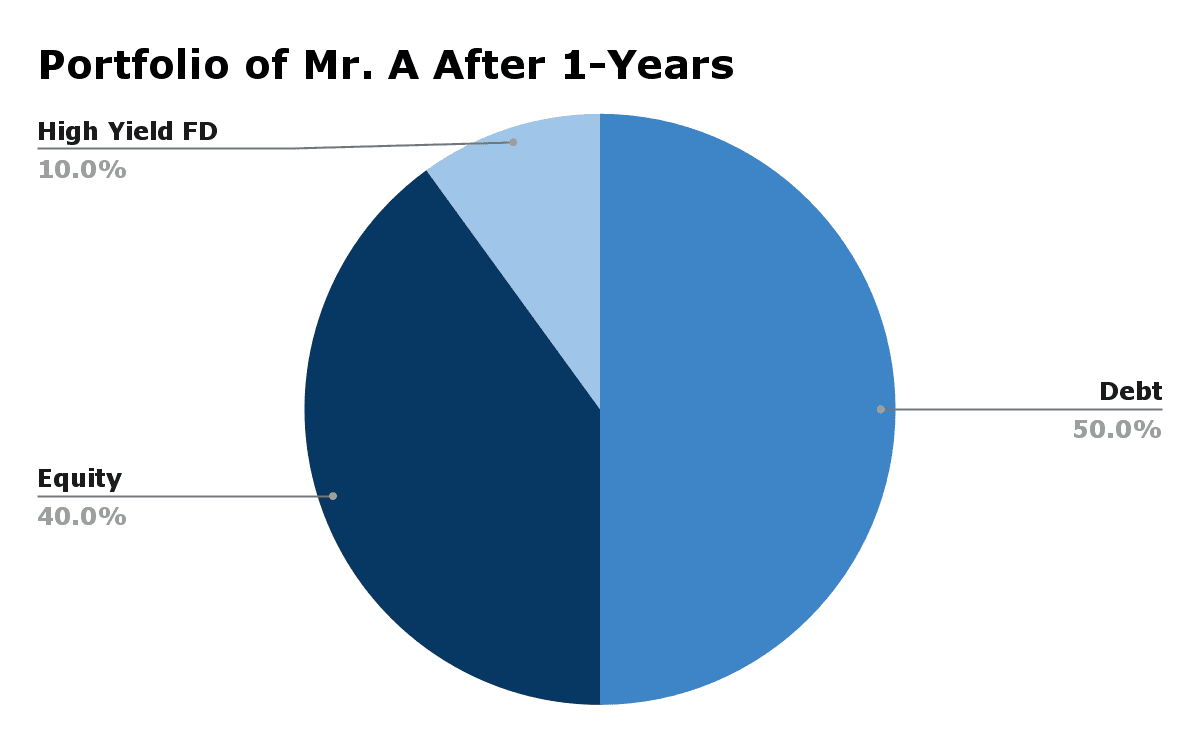

Now, after a year, the asset allocation has changed due to changing market conditions. For instance, when equities performed well, Mr A invested more in them and so on. So, after 1 year, his portfolio has 50% debt, 40% equity, and 10% FD.

Therefore, to maintain the previous asset allocation, Mr A liquidates some equity investments and buys more debt fund units. This process is called portfolio rebalancing. It is done in periodic intervals, like once or twice a year, to control risk.

However, these measures aren’t enough. Investors must avoid making common mistakes to ensure the success of their 5-year investment plan.

Also Read: Best Short-Term Investment Plans For 3 Months

Mistakes To Avoid For A 5-Year Investment Plan

Discussed below are some common mistakes that investors must avoid:

- Overcommitting to illiquid assets: Irrespective of investor temperament or fiscal goal, the liquidity of an asset is as important as its growth prospect, given the intrinsic market volatility. Therefore, a certain portion of the asset portfolio must be dedicated to liquid securities to control risk and maintain flexibility to adapt to changing market dynamics.

- Ignoring inflation or taxation: While calculating the prospective return from any investment medium, investors must consider the impact of inflation and taxation because they reduce the real return of an investor. Suppose the rate of return on investment is 6% but the rate of inflation is 4%. Therefore, the inflation-adjusted returns would be 2%.

Conclusion

A well-structured 5-year investment plan offers the right balance between growth and liquidity, helping investors navigate medium-term goals with confidence. By diversifying across bonds, SDIs, mutual funds, and even REITs—while avoiding common mistakes—you can create a resilient portfolio that grows steadily, manages risk, and stays aligned with your financial objectives. To learn more about investing, sign up on Grip Invest today and choose from a range of fixed-income investment options.

Frequently Asked Questions On 5-Year Investment Plan

1. Are bonds a good option for a 5-year investment horizon?

Yes, bonds are a good option for a 5-year investment horizon as they offer fixed, stable returns. However, it is advised that you add them to your portfolio, considering your risk appetite and liquidity needs. Bonds with higher ratings are more secure and safer, but they offer lower returns compared to bonds with a lower rating.

2. What return can I expect from a SIP over 5 years?

SIP returns depend upon the mutual fund category and choice of fund house. Evaluating the fund performance through fact sheets can aid in understanding returns over particular tenures. SIPs can be done in mutual funds or bonds as well. The returns will depend upon the underlying assets. For example, if you are doing SIP in a large-cap equity mutual fund, the returns can be lower than those of SIP in a small-cap equity mutual fund. However, the small-cap mutual fund comes with high risk, too.

3. Is it better to invest in mutual funds or fixed deposits for 5 years?

Both mutual funds and high-yield FDs can aid in optimal investment. The choice between the two should be made after considering individual financial goals and investment philosophy.

References:

1. AMFI India, accessed from: https://www.amfiindia.com/mutual-fund

2. SEBI, accessed from: https://www.sebi.gov.in/legal/circulars/oct-2017/categorization-and-rationalization-of-mutual-fund-schemes_36199.html

3. Economic Times, accessed from: https://economictimes.indiatimes.com/wealth/invest/how-to-invest-in-reits-and-earn-rental-income-without-owning-property/how-reits-generate-returns/slideshow/123132675.cms

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks, including delay and/ or default in payment. Read all the offer-related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for the consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001