Best Large Cap Mutual Funds In India 2026: Top Picks, Returns And How To Choose

Why Large-Cap Funds Are Popular Among Indian Investors

Large-cap mutual funds are a cornerstone for Indian investors seeking stability and consistent returns. These funds invest primarily in companies with large market capitalisations, typically the top 100 companies, which are listed on Indian stock exchanges such as BSE or NSE.

Their popularity stems from their predictable performance, transparency, and lower volatility compared to mid or small-cap funds.

For investors motivated by long-term wealth creation, large-cap funds offer a balanced approach, combining growth potential with reduced risk. Whether you are a seasoned investor or a beginner exploring the best mutual funds for SIP in 2026, large-cap funds are often a go-to choice.

Top 5 Large Cap Mutual Funds In India (2026)

In order to shortlist the top 5 large-cap mutual funds in India in 2026, the following parameters have been considered:

1. AUM of the fund is not below INR 10,000 crores

2. The expense ratio should be a maximum 1%

3. The 3-year and 5-year historical performance of the fund should be positive

4. All funds are direct plans only; no regular plans are considered

Fund Name | 3-Year CAGR | 5-Year CAGR | AUM (INRCr) | Expense Ratio |

Nippon India Large Cap Fund - Direct Plan - Growth | 18.20% | 17.60% | 46,521 | 0.70% |

ICICI Prudential Large Cap Fund - Direct Plan - Growth | 16.80% | 15.40% | 69,948 | 0.80% |

HDFC Large Cap Fund - Direct Plan - Growth | 14.20% | 14.40% | 35,458 | 1.00% |

Aditya Birla Sun Life Large Cap Fund- Direct Plan -Growth | 14.50% | 13.00% | 26,702 | 1.00% |

DSP Large Cap Fund-Direct Plan- Growth | 17.20% | 13.00% | 6,620 | 0.80% |

Source: Data has been taken from Moneycontrol (As of 11 April 2026).

NOTE: Please note that the historical performance of a mutual fund does not guarantee future performance. It is just one way of analysing the performance of a mutual fund. Investors are advised to check all the offer-related documents carefully before selecting any mutual fund.

These top 5 large-cap mutual funds are selected on the basis of above mentioned criteria; however, the top 5 funds can be different for different individuals if they change their criteria.

For example, an individual may not want to omit the funds having an AUM less than INR 10,000 crores, or he/she may also want to consider the regular plans too while shortlisting. We have removed regular plans as they come with extra expenses for the investors.

Benefits Of Large-Cap Funds

Large-cap funds offer several benefits that make them an attractive choice for investors, including:

- Lower Downside Risk: Large-cap companies are well-established with strong fundamentals, making them less susceptible to market fluctuations.

- Ideal For SIPs: Their stability makes them perfect for Systematic Investment Plans (SIPs), allowing investors to build wealth gradually.

- Strong Historical Performance: Historically, large-cap funds have delivered steady returns, often outperforming inflation over the long term.

For example, Priya invests INR 10,000 each month in a large-cap fund delivering an average annual return of 12% over 10 years. Thanks to the power of compounding, her investment grows to about INR 23.23 lakh, highlighting the impact of consistent investing.

Large-Cap Mutual Fund vs Index Fund - Key Differences

If you have been studying about the large-cap mutual funds, then there might be a time when you have questioned yourself if it is better to invest in the Nifty 50 index funds instead. This is a valid concern, but the true answer to this would depend on what you expect from your investments.

The thing that you need to know is that both these investments target the most valuable firms in India.

Parameter | Large Cap Mutual Funds | Nifty 50 Index Fund |

Management style | Actively managed by a fund manager | Passively tracks the Nifty 50 Index |

Aim | Beat the beachmark index | Match the benchmark index |

Expense Ratio | 0.50%-1.00% | 0.10%-0.30% |

Flexibility | Allocations can be shifted tactically | No flexibility |

Return potential | Can outperform the index in skilled hands | Returns mirror the index, excluding costs |

Tracking error | Not applicable | Low tracking error means a better fund. |

It all comes down to one basic tradeoff. The former will pay off if the fund manager is able to generate returns above the market rate. The latter will deliver market-level returns but at significantly lower costs.

According to previous data, over the last decade or so, there have been very few active large-cap funds that have delivered consistent outperformance over the Nifty 50 index.

There are only two such examples, viz. Nippon India and ICICI Prudential. On average, the remaining active large-cap funds have been generating similar returns to or below those offered by the index.

Who picks what then? If you belong to a passive lot of investors, then you will want to invest in the index itself to ensure that your returns are consistent and that you incur minimal costs.

Alternatively, if you are keen to do your research and select an active large-cap fund, then it makes sense from an investment perspective. Most investors have typically been investing in both.

Should You Invest In Large-Cap Funds Now?

The decision to invest in large-cap funds in the year 2026 relies on the financial goals and risk appetite. With India’s economy projected in order to grow steadily, large-cap companies are always well-positioned to benefit from market stability.

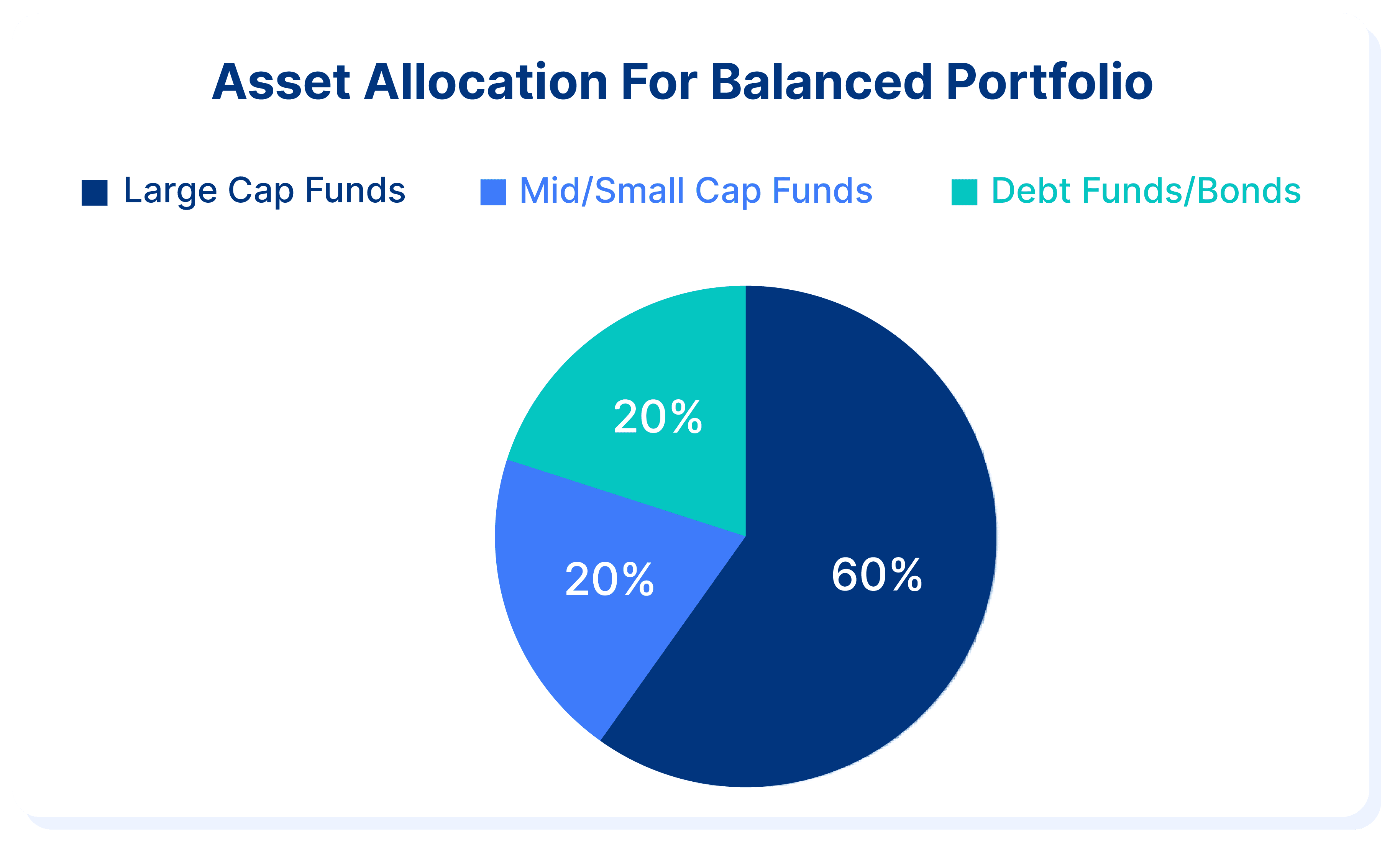

Moreover, global uncertainties or interest rate fluctuations could also impact the returns. For conservative investors, large-cap funds remain a safe bet just because of their resilience. Experts suggest allocating 40-60% of your portfolio to large-cap funds for equivalent and balanced growth.

- 60% Large Cap Funds: Stability and growth

- 20% Mid/Small Cap Funds: Higher growth potential

- 20% Debt Funds/Bonds: Risk mitigation

Taxation Of Large Cap Equity Funds In India

Many investors think only about returns and do not consider taxes, which may cut into their profits without them being aware of it. The taxation laws for large-cap equity funds are easy to understand, but understanding them helps you manage redemptions better.

Mutual funds are categorised as equity funds according to the Indian taxation laws because they have at least 80 per cent of their portfolio invested in equity stocks. Here is how they are taxed:

1. Long Term Capital Gains (LTCG)

Any gain that you realise from the redemption of your large-cap fund units, when you have held such units for more than 12 months before redemption, will be considered a long-term capital gain.

- Rate of Taxation: 12.5% on gains above INR 1.25 lakh per financial year

- Gains less than INR 1.25 lakh within a financial year: exempt from taxation

- Indexation facility not applicable anymore (abolished in Budget 2024)

For instance, if you redeem your units at gains amounting to INR 3 lakh in a financial year, you will be taxed 12.5% on just INR 1.75 lakh (INR 3 lakh minus INR 1.25 lakh exemption), which equals INR 21,875.

2. Short-Term Capital Gains (STCG)

In case you sell before fulfilling the one-year requirement, such gains will be termed short-term capital gains.

Rate of tax: 20%, flat, irrespective of your income slab. There is no exemption limit in this regard.

How To Select A Large-Cap Fund - Criteria Checklist

Selecting a large-cap mutual fund is not about selecting the top-performing fund of the previous year. You should be looking for a fund that has consistently delivered strong performance over different market cycles.

These are some of the important criteria that you need to consider before investing:

Criteria | What to look for |

3Y & 5Y CAGR | Consistently above category average |

Alpha | Positive |

Sharpe ratio | Above 1 |

Tracking error | Low |

Expense Ratio | Below 1% for direct plans |

AUM | Above INR 10,000 crore |

Tenure for Fund Manager | Minimum 3-5 years |

Portfolio turnover | Moderate |

How about using this method as quickly as possible? Simply shortlist those funds that have alpha greater than zero, a Sharpe ratio above 1, and an expense ratio less than 1%. Finally, confirm the tenure of the fund manager.

Large-Cap Fund Performance During Market Downturns

Despite being affected by market correction phases, large-cap schemes experience fewer drawdowns than mid and small-cap schemes. Recent market events clearly demonstrate this point.

COVID-19 Market Correction (March 2020)

Nifty lost value from its level of about 12,400 to about 7,500. In that event, Nifty 100 TRI shed about 28.86% of its value, while mid and small-cap indices shed even more. However, a swift recovery followed, with markets having recovered within about six months. Investors who continued investing recovered their money and saw significant growth by the end of 2021.

Market Correction of 2022

Between October 2021 and June 2022, Nifty shed about 18.39% of its value because of the effects of global inflation, interest rate increases, and the Russia-Ukraine conflict. During this period, large-cap schemes outperformed other market segments such as mid and small-cap.

| Market Event | Approximate Drawdown | Recovery Time |

| COVID-19 craze (Jan-Mar 2020) | ~28.86% (Nifty 100 TRI) | ~6 months |

| 2022 correction (Oct 2021- Jun 2022) | ~18.39% (Nifty 50) | ~8-10 months |

Conclusion

As per the above discussion, it is concluded that large-cap mutual funds are a reliable choice for investors seeking stability and growth in the financial year 2026. Their lower risk profile and consistent returns make them ideal for long-term wealth creation, especially through SIPs. Moreover, in order to mitigate the risks further, it is recommended to diversify the fixed-income securities, such as bonds or Securitised debt instruments (SDIs). Combining large-cap funds with debt instruments can easily improve the portfolio stability.

For investors looking to complement their mutual fund portfolio with stable, fixed-income options, log in to Grip Invest-India’s one-stop destination for high-quality fixed-return investments.

FAQs On Best Large-Cap Mutual Funds

1. Are large-cap funds safer than mid or small-cap funds?

Yes, large-cap funds are generally safer due to their investment in well-established companies with stable earnings, reducing volatility compared to mid or small-cap funds.

2. What is the tax on large-cap mutual funds in India?

Long-term capital gains (LTCG) above INR 1.25 lakh are taxed at 12.5% for equity-oriented large-cap funds. Short-term gains (less than 1 year) are taxed at 20%.

3. Can I invest monthly in large-cap funds via SIP?

Absolutely! Large-cap funds are ideal for SIPs, allowing you to invest small amounts regularly for long-term growth. Learn more in our guide on Best SIP Plans for 2026.

References

1. ET Money. (2025). Large Cap Mutual Funds. https://www.etmoney.com/mutual-funds/equity/large-cap/32

Want to stay at the top of your finances? Don’t forget to sign up!

Join the community of 4 lakh + investors and learn more about Grip, the latest financial knick-knacks, and shenanigans that take place in the world of investing.

Happy Investing!

Disclaimer: This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip Invest Technologies Private Limited ("Grip", formerly known as Grip Invest Advisors Private Limited) is not registered with SEBI in any capacity and does not advise, encourage, or discourage its users to invest or not invest in any securities. Grip is solely an execution-only platform and does not guarantee or assure any return on investments made by you in any opportunities sourced by Grip and accepts no liability for consequences of any actions taken based on the information provided. Your investment is solely based on your judgement. Investments in debt securities are subject to risks. Read all the offer-related documents carefully.