Best Liquid Funds in India 2026: Top Picks, Returns, Risks And Comparison

As of 31 May 2026, the total number of mutual fund folios in India stood at 27.66 crore1. The Indian mutual fund industry’s AUM stood at INR 81.58 lakh crore on the same date, up from INR 13.82 lakh crore on 31 May 2016.

This implies nearly 19.43% CAGR over 10 years. However, there might be some investors who are reluctant to take advantage of this trend due to their risk-averse nature or need for liquidity.

For such investors, the best liquid funds can yield optimal returns whilst controlling risk and liquidity requirements. Therefore, this blog aims to list the best liquid mutual funds in India.

What Are Liquid Funds?

Liquid funds are debt mutual funds that invest in treasury bills, commercial papers, certificates of deposit and similar money market instruments with maturities of up to 91 days. They help investors place surplus cash for brief periods while retaining swift access, moderate risk and market linked return potential.

Liquid Fund Comparison 2026

Before getting into the list of top liquid funds in India, understanding the meaning of these funds can reveal key features.

Liquid funds invest in short-term money markets and debt securities. According to the SEBI categorisation, the maturity period of these assets held by the liquid funds should not exceed 91 days3.

The short maturity period is the key to low risk and high liquidity. Some common assets held by the best liquid funds are commercial papers, treasury bills, certificates of deposits, etc.

Risks And Liquidity Features

Liquid mutual funds are considered a popular short-term parking option due to the fact that they offer high liquidity. They are also considered low-risk liquid funds due to their short maturity, but are not completely risk-free.

Liquidity

Many liquid funds offer same-day redemption or next-day redemption, which depends on the cut-off timing. The price sensitivity is lower compared to long-term debt funds since the maturity is shorter. They work well for short-term goals such as upcoming bills, short-term travel funds, or keeping money ready for investment opportunities.

Risks

A credit can impact the return if the funds hold low-quality debt. There are also risks to the interest rate. They are usually low and limited due to short maturity. So funds also impose exit loads for withdrawals within a few days. Compared to a savings account, returns may fluctuate slightly based on portfolio yield.

Best Liquid Funds In India In 2026

Which Is The Best Liquid Fund In India?

No single scheme leads for all investors. A sound choice blends high credit quality, lean costs, adequate scale, prompt redemption and steady near term performance. The final pick should match cash flow needs, holding period, tax position and comfort with market linked debt products.

The table below lists some of the top liquid funds in India based on AUM. All schemes mentioned below are direct growth plans2. AUM and expense ratio are based on 31 May 2026, while one-year returns are as of 15 June 2026.

| Fund | AUM (INR crore) | Expense ratio (%) | 1-year return (%) |

| SBI Liquid Fund | 79,363 | 0.17 | 6.25 |

| HDFC Liquid Fund | 67,998 | 0.17 | 6.28 |

| ICICI Prudential Liquid Fund | 58,096 | 0.17 | 6.26 |

| Axis Liquid Fund | 56,168 | 0.10 | 6.37 |

| Aditya Birla Sun Life Liquid Fund | 47,520 | 0.18 | 6.36 |

| Kotak Liquid Fund | 40,018 | 0.16 | 6.29 |

| UTI Liquid Fund | 33,248 | 0.14 | 6.33 |

| Nippon India Liquid Fund | 31,752 | 0.17 | 6.33 |

| Tata Liquid Fund | 30,449 | 0.19 | 6.31 |

| DSP Liquidity Fund | 19,019 | 0.10 | 6.34 |

Source: Valuesearchonline4

Discussed below are some key takeaways from the best-performing liquid mutual funds in India. These analytical pointers can aid in formulating an optimal investment strategy.

- SBI Liquid Fund, HDFC Liquid Fund and ICICI Prudential Liquid Fund occupy the upper end of the table by asset size. Their scale indicates broad usage across retail and institutional accounts. In this category, size matters because redemption flows can be frequent.

- Axis Liquid Fund and DSP Liquidity Fund stand out on pricing, with an expense ratio of 0.10% each. The gap may look minor, but liquid fund performance usually moves within a tight band. Lower charges can therefore protect net gains over repeated or sizeable transactions.

- Aditya Birla Sun Life Liquid Fund combines a large corpus of INR 47,520 crore with a one year return of 6.36%. Its performance is close to Axis Liquid Fund, although the expense ratio is higher at 0.18%. This makes cost comparison essential.

- Kotak Liquid Fund, UTI Liquid Fund, Nippon India Liquid Fund and Tata Liquid Fund form the middle cluster by asset base. Their one year returns range between 6.26% and 6.33%. The narrow spread shows that recent performance alone gives an incomplete picture.

- Minimum investment can influence first time allocation. HDFC Liquid Fund, Axis Liquid Fund, Aditya Birla Sun Life Liquid Fund and DSP Liquidity Fund allow smaller entry amounts. Tata Liquid Fund requires INR 5,000, which may not suit every small ticket investor.

Overall, a suitable liquid fund should balance liquidity, expense ratio, credit quality and redemption convenience. A large corpus or a marginally higher one year return should not be the only basis for selection.

Which Liquid Fund Is Best for You?

The best liquid fund depends on the purpose of investment. A fund suitable for emergency money may not be the same as one preferred for a large corporate style cash allocation.

The table below is for comparison and example only. It does not indicate suitability for every participant. Final selection should depend on cash access needs, risk appetite, holding period, tax position and the latest portfolio details.

The AUM and expense ratio are as of 31 May 2026, while one year returns are based on around 15 June 2026.

| Investor profile | Example | Suitability note |

| First-time allocation | HDFC Liquid Fund | Low minimum investment makes entry easy; large AUM adds comfort. |

| Emergency corpus | ICICI Prudential Liquid Fund | Very low minimum withdrawal suits irregular cash needs. |

| Large corpus parking | SBI Liquid Fund | Highest AUM in the list, useful for sizeable temporary parking. |

| Cost-focused allocation with scale | Axis Liquid Fund | Low expense ratio can matter meaningfully in liquid funds. |

| Small ticket and low-cost allocation | DSP Liquidity Fund | Low entry amount with a competitive expense ratio. |

| Short-term surplus parking | Aditya Birla Sun Life Liquid Fund | Flexible redemption and decent returns for short-term use. |

| Mid-sized established option | Kotak Liquid Fund | Balanced choice with moderate AUM and reasonable cost. |

| Lower expense among mid-sized funds | UTI Liquid Fund | Lower expense ratio makes it attractive for cost-conscious investors. |

| Higher entry amount investor | Tata Liquid Fund | Suitable for investors comfortable with a higher minimum investment. |

However, only comparing liquid fund AUM and returns is not enough for profitable portfolio creation. Some other analytical parameters must be considered before choosing the right liquid fund.

Key Metrics: Expense Ratio, Sharpe, Standard Deviation

It is important that investors not only rely on AUM and 1-year return liquid but also be able to select from the best liquid funds. You can make better decisions when comparing costs and risk metrics, including expense ratio funds, standard deviation, and Sharpe ratio of liquid funds.

1. Expense Ratio

By definition, the annual ratio is the fee charged annually by the fund house to manage the fund. It directly reduces the investor's returns. Small differences in expense ratios can impact net gains over time because liquid mutual funds generate similar return ranges.

This is why, while selecting the best liquid funds, investors prefer funds with a consistently low expense ratio, especially when parking money for months rather than days.

2. Standard Deviation

The standard deviation tells us how much a fund’s returns fluctuate from its average. A longer standard deviation indicates more stable and predictable performance for investors seeking low-risk liquid funds.

While comparing, standard deviation is important because a fund having slightly lower returns but higher consistency can be a safer choice for short-term money management.

3. Sharpe Ratio

With the Sharpe ratio, you can understand whether the fund’s return is worth the risk taken. A higher value indicates better risk-adjusted performance, which means the fund is delivering stronger returns with lower volatility. Comparing the Sharpe ratio alongside returns can provide a clear view of liquid funds that are actually efficient and not just high-returning.

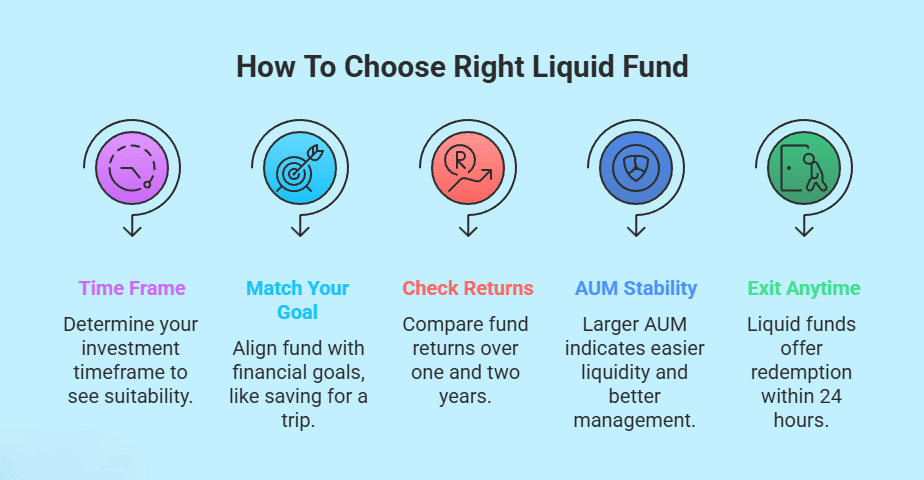

How To Select The Best Liquid Funds?

Discussed below are some parameters that can aid in understanding how to choose liquid funds optimally.

1. How to Select Liquid Funds by Time Horizon?

Based on how long you plan to stay invested decides which liquid funds you choose. They work best for short-term cash parking since liquid mutual funds invest in short-term duration, which can be up to 91 days.

The table below shows the best-case use and what to prioritise based on your time horizon.

| Time Horizon | Best Use Case | What to prioritise |

| 1 day – 1 week | Temporary holds, emergency cash | Faster redemption with low exit load |

| 1 week – 3 months | Surplus cash, short-term parking | Low standard deviation and stability |

| 3 – 12 months | Planned expenses | Lower cost with higher 1-year return liquid funds |

| 1 – 2 years | Short-term, conservative investing | Higher Sharpe ratio liquid funds and consistent performance |

2. Check Returns, Costs And Risks Before You Invest

Along with considering the investment tenure, the investor should also monitor the category average and benchmark to choose the best liquid funds for short-term investment. If the fund performance in terms of returns and risk metrics is better than the benchmark or category average, it implies optimal fund performance.

The factsheet of a mutual fund usually mentions the benchmark it tracks and relevant details.

For instance, two key benchmarks mostly followed by liquid funds are the CRISIL Liquid Debt A-I Index and NIFTY Liquid Index A-I6. The table below shows the one-year annualised return of both.

Benchmark | One-year annualised return |

CRISIL Liquid Debt A-I Index | 5.95% (Average YTM) |

NIFTY Liquid Index A-I | 7.07% (One-year return) |

Source: CRISIL7

Similarly, comparison with the category is also key. Discussed below are some key category metrics that can be compared to fund-specific metrics.

Return metrics | |||

Years | Average | Top | Bottom |

One-year | 5.36 | 12.84 | -1.49 |

Risk-adjusted Metric | |||

Parameter | One Year | Three Year | Five Year |

Standard deviation | 0.2801 | 0.3539 | 0.5105 |

Sharpe ratio | 0.6119 | 0.9827 | 0.3837 |

Sortino Ratio | 18.581 | 10.5857 | 2.0737 |

Alpha | -0.2201 | -0.3068 | -0.2968 |

Beta | 1.1017 | 1.2547 | 1.1963 |

Source: Morningstar8

However, no matter how profitable a particular investment medium might seem, over-reliance of a portfolio on an asset can increase risk.

3. Tax Treatment of Liquid Fund Gains

Considering taxation while choosing from the best liquid funds can affect post-tax returns significantly, depending on holding periods. Gains in liquid mutual funds are taxed as capital gains when the units are redeemed, unlike savings accounts, in which interests are taxed annually.

- Short-term Capital Gains: The gains are treated as short-term capital gains when the units of liquid funds are sold within 36 months. They are also taxed as per your income tax slab rates.

- Long-term Capital Gains: The gains become long-term capital gains if funds are held for more than 36 months and are taxed at 20% with indexation benefits. This improves post-tax returns for long-term investors.

4. Smart Diversification

Complementing liquid funds with other alternative investments can aid in optimal diversification. Discussed below are some popular instruments on Grip.

| Instrument | Minimum investment | Return | Security cover | Backed by or Rated by |

INR 1,000 | 9% to 12.5% | Yes | ICRA, CRISIL | |

High-yield FDs | INR 1,000 | Up to 10% | Yes | Rated and backed by RBI |

LeaseX | INR 1,00,000 | Up to 16% | Yes | SEBI regulated and rated |

InvoiceX | INR 1,00,000 | Up to 14% | Yes | RBI or SEBI-regulated and rated |

LoanX | INR 1,00,000 | Up to 14% | Yes | RBI or SEBI-regulated and rated |

Benefits of Investing In Liquid Funds

Liquid funds with highest returns help manage surplus capital without committing it for a long tenure. They are commonly used for near term parking, contingency reserves and temporary allocation before shifting capital into other assets.

1. High liquidity

These schemes provide faster withdrawal flexibility than many traditional debt products. Redemptions follow mutual fund settlement timelines, while select plans offer instant access within stated limits.

2. Low risk

The portfolio usually holds short maturity debt and money market instruments. This structure reduces sensitivity to interest rate movements, although capital protection and assured income are not guaranteed.

3. Better returns than savings account

A regular savings account often offers lower income on unused balances. Liquid funds may provide better return potential when surplus cash remains unutilised for a few weeks or months.

4. SIP availability

Several plans allow systematic investment plans. This helps individuals build a reserve gradually, instead of waiting to deploy a lump sum.

5. Diversification

Liquid funds add a separate cash management layer to an investment portfolio. Their holdings usually span treasury bills, certificates of deposit, commercial papers and other near-term instruments.

Liquid Funds vs FD vs Savings Account

Are Liquid Funds Better Than FDs?

Liquid funds may work well for temporary cash deployment where faster withdrawals and market-linked gains matter. Fixed deposits offer rate certainty, defined tenure and clearer capital protection. The stronger option depends on liquidity needs, tax slab, holding period and tolerance for small NAV movements.

Liquid funds, fixed deposits and savings accounts serve different cash management purposes. Here is a comparison of the investment options available:

Feature | Liquid fund | Fixed deposit | Savings account |

Return | Market linked. | Fixed when the deposit is booked. The rate depends on the bank, tenure, deposit size and depositor category. Senior citizens generally receive a higher rate. | Usually lower than the other two options. Banks set the rate and may apply different slabs based on account balance. |

Liquidity | Allows fairly quick withdrawal, although settlement follows mutual fund timelines. Some schemes also provide instant redemption within specified limits, which helps in very short holding periods. | Premature closure is usually allowed. The bank may reduce the applicable rate or levy a penalty, which can lower the final payout. | Offers immediate usability. Money can move through ATM, UPI, cheque, net banking, debit card or branch withdrawal without a redemption process. |

Risk | Carries low to moderate risk. These schemes invest in debt and money market instruments maturing within 91 days, but they do not guarantee capital protection or fixed gains. | Considered relatively low risk when placed with a regulated bank. Deposit insurance covers up to INR 5 lakh per depositor per bank, including principal and accrued interest. | Carries low risk for routine banking needs. The balance also comes under deposit insurance cover of up to INR 5 lakh per depositor per bank. |

Taxation | Gains from most debt fund units bought on or after 1 April 2023 are taxed as per the applicable income tax slab. | Interest earned is added to income and taxed at the applicable slab rate. Banks may deduct TDS when the annual threshold is crossed. | Interest earned is added to income. Eligible individuals and HUFs can claim deduction up to INR 10,000 under Section 80TTA, while senior citizens may use Section 80TTB. |

Conclusion

Any investment must align with your unique risk profile, goals, and timeline. Liquid mutual funds serve as an ideal entry for conservative investors seeking steady fixed-like returns (typically 6-7% annualized) and same-day liquidity for emergency funds or short-term parking. Yet, chasing top 2026 liquid fund returns alone misses the bigger picture—true wealth growth demands diversification via alternative investments like AIFs, offering 12-18% potential yields with low equity correlation.

Grip can offer up to 12.5% post-tax returns through a range of assets. Don’t forget to visit Grip Invest today!

FAQs On Best Liquid Funds

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001