SIPs As A Successful Wealth-Building Tool: Investing With Just INR 1,000

Mastering a skill or an art form requires consistency, commitment, and fundamental knowledge of the same. Wealth building is no different. It requires patience, consistency, and commitment. This idea paves the way for Systematic Investment Plans or SIPs.

SIPs are structured investment tools that assist in wealth building over the long term. SIPs are primarily used in mutual funds as an investment method, through which investors can regularly (weekly, monthly, quarterly, or annually) contribute a fixed amount of money that is directly invested into the mutual fund.

Every investment, whether small or large, can benefit from the long-term compounding that is associated with SIPs. In this blog, we explore the stairway to building wealth, with an amount as small as INR 1,000.

Can An INR 1,000 SIP Make A Difference?

SIPs simplify investors’ wealth-building journey through their key benefit: the Power of Compounding. Through Compounding, investors can earn returns on both their invested SIP amount and the earned returns.

‘Net Asset Value’ or NAV is the fair value of a mutual fund unit. When investing through an SIP mode, units are allotted based on the prevalent NAV. Suppose an investor starts a monthly SIP worth INR 1,000 in a mutual fund. Every month, mutual fund units are allotted according to the NAV on the day of the SIP investment.

Let us understand how the power of compounding works, using this table.

Assuming a mutual fund interest rate of 12%, the INR 1,000 SIP returns in 5 years will look like:

| Starting balance | Total Investment | Interest Amount | Closing Balance | |

| Year 0 | 0 | INR 12,000 | INR 1,440 | INR 13,440 |

| Year 1 | INR 13,440 | INR 25,440 | INR 3,052 | INR 28,493 |

| Year 2 | INR 28,493 | INR 40,493 | INR 4,860 | INR 45,353 |

| Year 3 | INR 45,353 | INR 57,353 | INR 6,882 | INR 64,235 |

| Year 4 | INR 64,235 | INR 76,235 | INR 9,148 | INR 85,383 |

| Year 5 | INR 85,383 | INR 97,383 | INR 11,686 | INR 1,09,068 |

This table shows how the power of compounding exhibits its magic over a period of time. On a total investment of INR 72,000 (12,000*6), over 5 years, a mutual fund interest rate of 12% provides a total return of 8,640.

However, with the power of compounding in play, the returns have been compounded over time, earning returns on returns. This leads to a total return of INR 37,068, with the power of compounding.

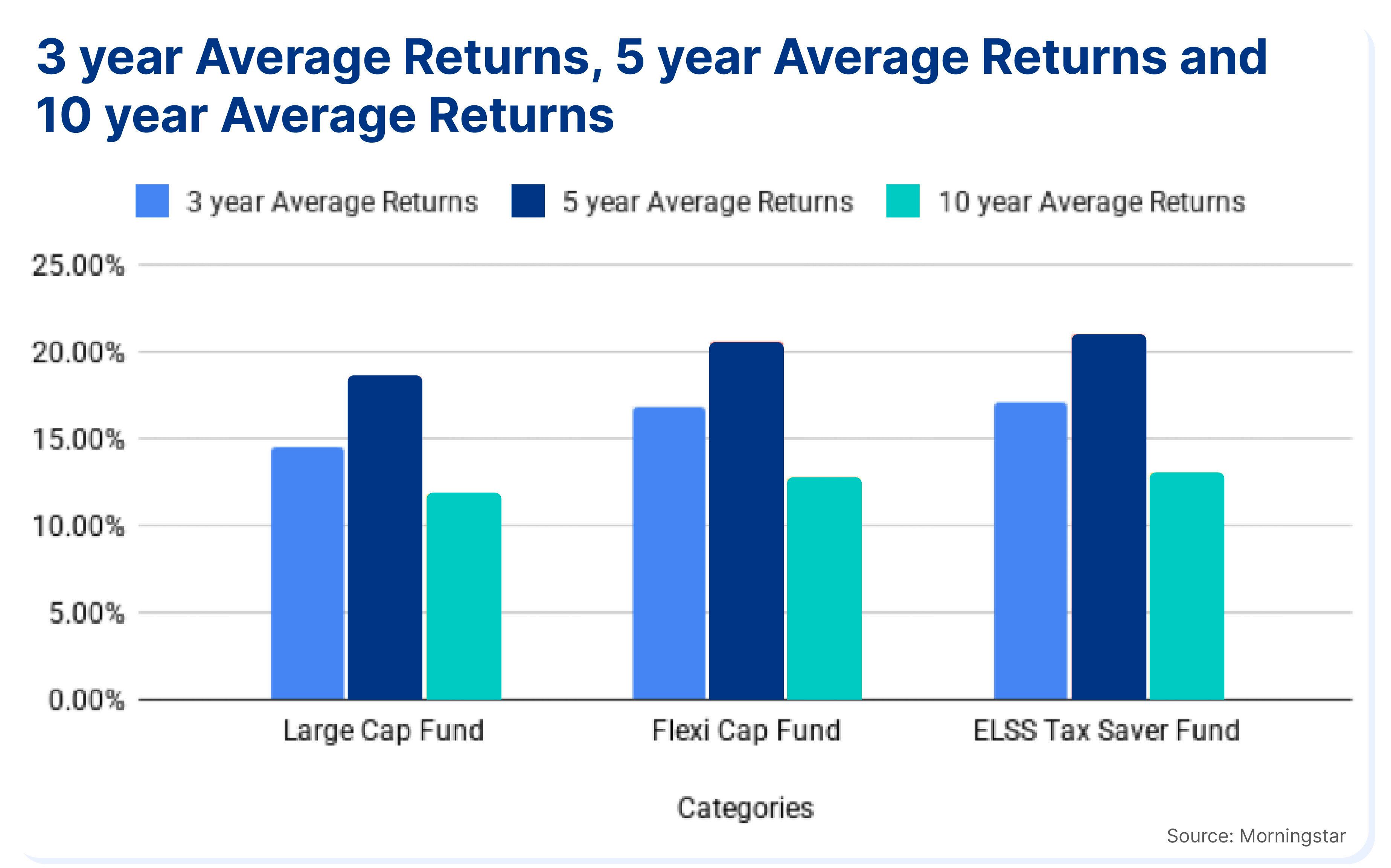

The effect of compounding is dependent on the investment amount and the returns. Let us look at the average returns on a large-cap, flexi-cap, and ELSS fund, over 3, 5, and 10 years (as of 6 August 2025).

Source: Morningstar

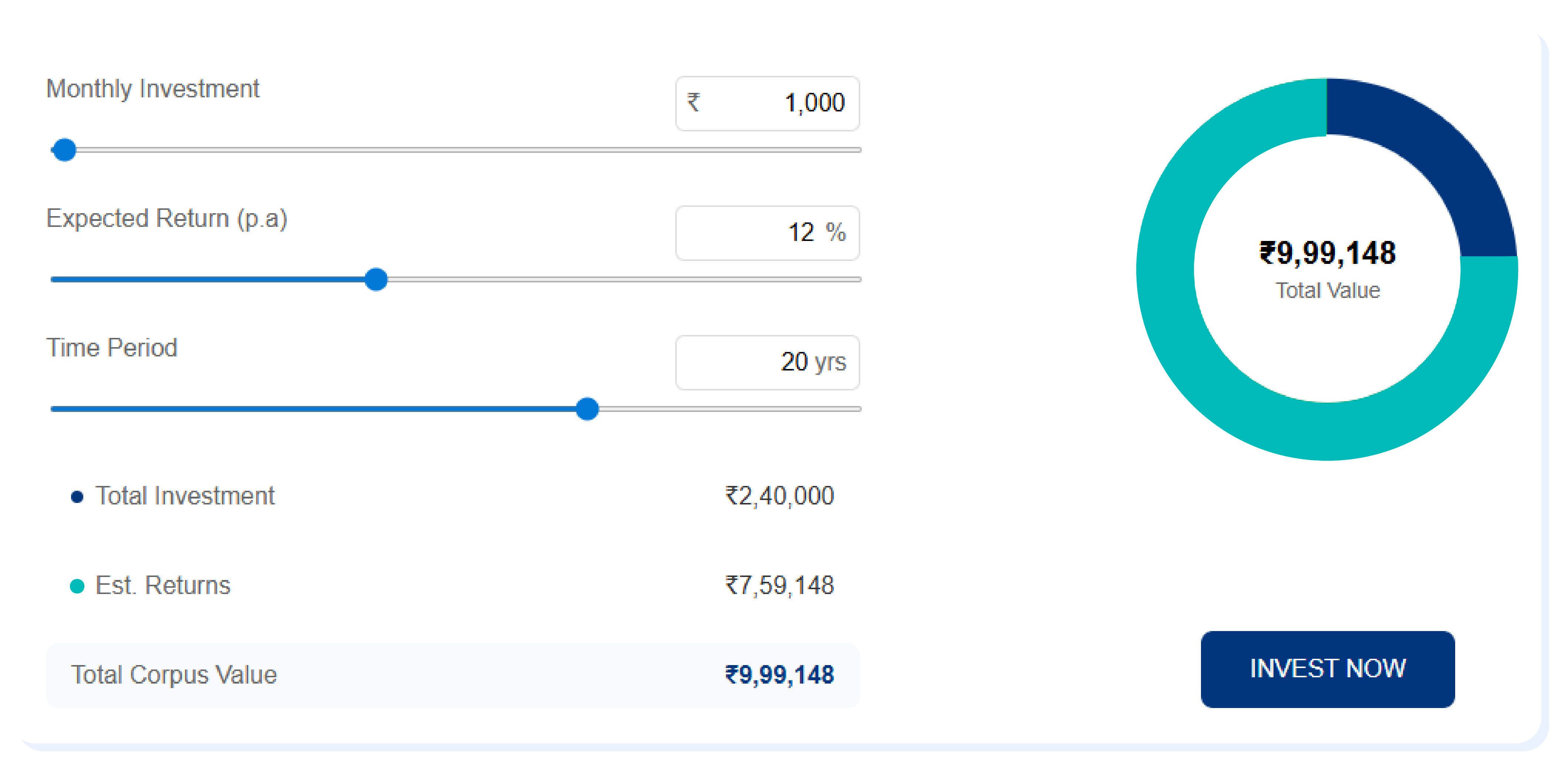

With an INR 1,000 SIP, an investor can create significant wealth over the long term. For instance, a long-term investment of 20 years in a low-risk mutual fund, such as a large-cap fund, can be expected to build an INR 10,00,000 corpus, as shown below through an SIP compounding calculator by Grip Invest.

Top SIP Plans To Consider In 2026

Each category of equity funds is suitable for different types of investors. Some categories are low-risk, such as large-cap, flexi-cap, and tax-saving funds. Whereas other categories may have high-risk yet growth potential, such as the mid-cap and small-cap categories.

Let us look into some equity funds that have given the highest returns over 10 years, in low-risk SIP mutual funds like large-cap and flexi-cap, and high-growth SIP mutual funds like mid-cap and small-cap.

Fund Name (Large-cap) | AUM (As of 5th Aug, 2025) | Annualised Returns Over 10 Years(%) |

| Nippon India Large Cap Fund | INR 44,123 Crores | 14.62% |

| Canara Robeco Large Cap Fund | INR 16,345 Crores | 14.43% |

| ICICI Prudential Large Cap Fund | INR 71,516 Crores | 14.40% |

Source: AMFI India

| Fund Name (Mid-cap) | AUM (As of 5th Aug, 2025) | Annualised Returns Over 10 Years(%) |

| Invesco India Mid Cap Fund | INR 7,804 Crores | 18.98% |

| Kotak Mid Cap Fund | INR 57,253 Crores | 18.62% |

| Edelweiss Mid Cap Fund | INR 11,100 Crores | 18.37% |

Source: AMFI India

| Fund Name (Small cap) | AUM (As of 5th Aug, 2025) | Annualised Returns Over 10 Years(%) |

| Nippon India Small Cap Fund | INR 65,755 Crores | 21.26% |

| Quant Small Cap Fund | INR 29,436 Crores | 20.33% |

| Axis Small Cap Fund | INR 26,059 Crores | 19.11% |

Source: AMFI India

| Fund Name (Flexi cap) | AUM (As of 5th Aug, 2025) | Annualised Returns Over 10 Years(%) |

| Quant Flexi Cap Fund | INR 6,939 Crores | 18.93% |

| Parag Parikh Flexi Cap Fund | INR 1,13,130 Crores | 18.05% |

| JM Flexi Cap Fund | INR 5,889 Crores | 16.48% |

Source: AMFI India

Choosing The Right SIP For Your Goals

Understanding which SIP is right for you involves building a financial plan suitable for you. This includes assessing your risk appetite, investment goals, and time horizon. There is no right age to start investing through an SIP. You can start when you want to.

There is no rule of thumb to follow when choosing the right SIP for your goals. However, it is observed that:

- Age 20-30: Young investors in the 20-25 age bracket are considered to have more time on hand to save and invest. Typically, their risk level is considered very high. Therefore, the best SIP plans for young investors are usually aggressive funds such as small-cap, mid-cap, contrarian funds, thematic funds, etc.

- Age 30-40: Mid-aged investors in the 30-40 age bracket are still considered to have a high risk tolerance. This makes them more inclined to invest in relatively risky categories such as mid-cap, thematic, and sectoral funds, etc.

- Age 40-50: Investors in the 40-50 age bracket have a lower investment horizon and therefore a lower risk tolerance. Their ideal investment categories are stable and secure funds such as large-cap, flexi-cap, and hybrid funds, etc.

- Age 50-60: Close to retirement age, investors in the 50-60 age group usually want to preserve their wealth and therefore look for investments in categories such as large-cap funds, debt funds, etc.

Once risk appetite is established and assessed, evaluating the chosen fund is vital. Depending on the category of fund, you can check out their past performance through their monthly-released fact sheets, official mutual fund platforms such as AMFI, or through the fund’s official website. Instead of relying on the short-term performance of the given fund, one should look at long-term returns, such as 10 or 15 years, to get a comprehensive view of the fund’s performance.

Another aspect to consider is the expense ratio of a fund. An expense ratio is the annual maintenance fee a mutual fund charges from its investors. Comparing expense ratios across different funds in the same category can help make an informed decision.

Tips To Maximise SIP Benefits

To maximise the benefits of SIP, consider the following:

- Start early: The exclusive benefit of SIP, the power of compounding, multiplies with time. Therefore, the longer your investment horizon, the more benefits and amplified returns.

- Avoid missing SIP payments: It is crucial to stay consistent and not miss an SIP payment, as the growth of your portfolio may get disrupted. It also breaks consistency and leads to a less optimal corpus.

- Increase your SIP amount: You can choose to step up your SIP amount, with gradual growth in your income. For example, if your salary increases by 10% every year, you can set up a step-up of 10% in your SIP amount too. This practice helps in boosting your SIP returns, without putting a strain on your finances.

- Infinite by Grip Invest: Tools that help you automatically reinvest returns from Bonds or Securitised Debt Instruments (SDI) investments into a mutual fund SIP. Upon a certain level of growth in the SIP, this corpus can be reinvested back into a new bond/SDI. This way, the loop continues infinitely. You can activate this feature through Infinite by Grip Invest.

Conclusion

To summarise, SIPs are a convenient tool for wealth creation over the long term. This method of investing in a mutual fund builds discipline, consistency, and steady wealth over time. The key is to start early and stay invested for the long term.

An amount as little as INR 1,000 invested in a monthly SIP can build a corpus of INR 10 Lakhs in 20 years. Committing to an SIP could help you reach your financial goals in a planned, systematic manner. However, choosing the right SIP mutual fund for yourself requires assessment and evaluation of your investment goals, risk appetite, and time horizon.

FAQs On SIPs

1. How much return can I expect from a 5,000 SIP in 5 years?

Based on the long-term average returns of a low-risk mutual fund category such as large-cap, one can expect a 12% return over the long term. Therefore, with an INR 5,000 monthly SIP investment in a large-cap fund, an investor can expect to build a total corpus of INR 4,12,432, with INR 1,12,432 worth of returns.

2. What are the best mutual funds for an INR 1,000 SIP in 2026?

High-risk investors can look at the following options ( based on 10-year returns) for an INR 1,000 SIP in 2026:

| Fund name | 10-year returns (%) |

| Nippon India Small Cap Fund | 21.26% |

| Quant Small Cap Fund | 20.33% |

| Axis Small Cap Fund | 19.11% |

Source: AMFI India

Whereas low-risk investors can consider these options based on the highest 10-year returns.

Fund Name (Large-cap) | AUM (As of 5th Aug, 2025) | Annualised Returns over 10 years(%) |

Nippon India Large cap fund | INR 44,123 Crores | 14.62% |

Canara Robeco Large cap fund | INR 16,345 Crores | 14.43% |

ICICI Prudential Large cap fund | INR 71,516 Crores | 14.40% |

Source: AMFI India

3. Are there any low-risk SIP options for conservative investors?

Equity funds invest in equities that have high risk. However, there are many fixed-income SIP alternatives in India that may be suitable for conservative investors. Debt mutual funds are ideal for investors seeking stable returns.

References:

- UTI Mutual Fund accessed from:

https://www.utimf.com/articles/sip-at-1000-rs - Tata Capital Moneyfy accessed from:

https://www.tatacapitalmoneyfy.com/blog/sip/best-sip-plans-for-1000-per-month/ - Mint accessed from:

https://www.livemint.com/money/personal-finance/sip-calculator-how-to-become-crorepati-saving-rs-1000-a-month-in-mutual-funds-11639182719038.html - AMFI accessed from:

https://www.amfiindia.com/research-information/other-data/mf-scheme-performance-details

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans that take place in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer-related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for the consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001