ETF Vs Mutual Fund In 2026: Which Investment Is Better For Indian Investors?

For Indian investors, both Exchange Traded Funds (ETFs) and Mutual Funds offer a gateway to the world of diversified investing through pooled investment vehicles. While both products pool money from various investors and invest in a basket of securities, their structure, trading mechanisms, and costs differ. Understanding these differences is crucial before making any investment decision.

In this blog, we will break down what ETFs and mutual funds are, compare them across key parameters, and help you decide which might be a better fit for your financial goals in 2026.

What Is An Exchange Traded Fund (ETF)?

An ETF is a type of pooled investment instrument that is actively traded on stock exchanges, much like shares. ETFs typically track an underlying market index (like Nifty 50 or Sensex), a commodity (like gold), or a basket of assets.

ETFs in India are passively managed, meaning they aim to replicate the performance of their underlying benchmark. Common types of ETFs in India include Index ETFs, Gold ETFs, and Sectoral ETFs.

You can buy or sell ETFs through your trading account on platforms like Zerodha, Groww, or Upstox. All you need is a demat and a trading account.

Examples Of ETFs

Name | What It Tracks/Invests In |

Nippon India ETF Nifty 50 BeES | Nifty 50 Index |

Nippon India ETF Gold BeES | Domestic price of gold, through physical gold |

Nippon India ETF Nifty Next 50 Junior BeES | Nifty Next 50 Index |

Motilal Oswal S&P BSE Healthcare ETF | S&P BSE Healthcare Total Return Index |

UTI BSE Sensex ETF | S&P BSE Sensex Index |

What Are Mutual Funds?

A mutual fund, similar to ETFs, pools money from multiple investors and invests it in stocks, bonds, or other securities. These funds are offered by Asset Management Companies (AMCs) and are managed by professional fund managers.

Mutual funds can be actively managed (where fund managers try to outperform the market) or passively managed (trying to replicate the performance of the underlying index, much like ETFs).

You can invest in mutual funds through platforms like Coin by Zerodha, Groww, or directly with AMCs. You only need a bank account with KYC compliance. You will also need a demat account if you’re investing through stock brokers.

Types Of Mutual Funds

Type | Where They Invest |

Equity Mutual Funds | Primarily in equity stocks |

Index Mutual Funds | Track a specific stock market index |

Debt Mutual Funds | Fixed income securities (bonds, etc.) |

Hybrid Mutual Funds | Mix of equity and debt |

Thematic/Sectoral Mutual Funds | Focus on specific sectors/themes |

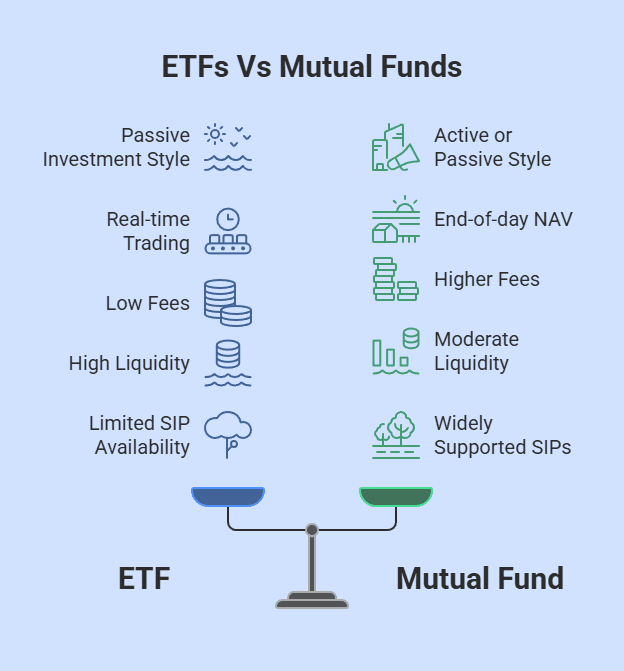

ETF Vs Mutual Fund: What’s The Core Difference?

The primary difference lies in their trading and management. ETFs are traded on exchanges in real time, like stocks. Their prices fluctuate throughout the day. Mutual funds, on the other hand, are bought or sold at the end-of-day Net Asset Value (NAV), and are not actively traded on the stock exchanges. In terms of management, while most ETFs in India are passively managed and simply replicate the underlying index or commodity performance, mutual funds can be both actively and passively managed. However, they are primarily known for their active fund management by professional fund managers.

1. Investment Approach and Management: Both ETFs and Mutual Funds are pooled investment vehicles. ETFs are mostly passive, tracking indices. Mutual funds can be active (trying to beat the market) or passive (index funds).

2. Trading Flexibility: ETFs offer intraday trading, allowing you to buy and sell anytime during market hours on recognised stock exchanges. Mutual funds only allow transactions at the day's closing NAV, and cannot be listed or traded on exchanges.

3. Cost Efficiency: ETFs generally have lower expense ratios, sometimes as low as 0.05%, while actively managed mutual funds can charge up to 2%.

4. Liquidity & Accessibility: ETFs are highly liquid if traded in large volumes, but require a demat account. Mutual funds are accessible through brokers as well as directly through AMCs, require no demat, and are easy to manage for long-term investors.

5. Ease of Investing: Mutual funds allow SIPs (Systematic Investment Plans) for disciplined investing, which is not usually available for ETFs.

ETFs Vs Mutual Funds - Key Differences

Parameter | ETFs | Mutual Funds |

Investment Approach | Usually passive, tracks an index or price of a commodity. | Primarily active, but can be active or passive. |

Management Style | Passively managed | Primarily actively managed, while index funds are passively managed. |

Trading and Liquidity | Intraday trading on stock exchanges is allowed. Liquidity depends on trading volume. | Trading on stock exchanges is not permitted. Bought/sold at end of day NAV. |

Exit Strategy or Redemption | Sold on exchange anytime; however, the exit may depend on the liquidity available based on trading volume. | Redeemed at NAV. |

Cost (Expense Ratio/Fees) | Lower expense ratios, brokerage fees apply for a trading account. | Higher expense ratios, no brokerage. |

Tracking Error | Low | Can be relatively higher, for index funds. |

Minimum Investment | Comparatively lower. | Varies, often higher minimums. |

Time Horizon | Short, medium or long term, depending on investment goals. | Typically long-term. |

Lock-in Period | Generally none. | Some funds have lock-in (e.g. ELSS). |

Risks | Market, liquidity risk. | Market, manager risk. |

Which One Offers Better Control And Lower Costs?

ETFs can be bought and sold anytime during market hours, offering more control for active traders. Mutual funds, with their end-of-day pricing, suit investors who prefer a hands-off approach. Even though ETFs provide better control, ETFs having lower trading volumes can have liquidity issues, and at the same time, mutual funds can be a better fit for those looking for professional management.

ETFs have lower expense ratios and no exit loads, but you pay brokerage and demat maintenance charges. Mutual funds may have higher expense ratios (especially active funds), exit loads if redeemed early, but no brokerage or demat fees.

ETFs Vs Mutual Funds: Expense Ratios

The following table gives a comparison of expense ratios for ETFs and Mutual Funds that invest in or track the same underlying asset class or index. This is to illustrate how ETFs often have a lower expense ratio compared to mutual funds while making similar investments.

Fund Name | Expense Ratio (%) |

Nippon India ETF Nifty 50 BeES (tracks Nifty 50 Index) | 0.04 |

UTI Nifty 50 Index Fund (an Index Mutual Fund that tracks the Nifty 50 Index) | 0.19 |

Nippon India ETF Gold Bees (tracks the price of physical gold) | 0.80 |

Nippon India Gold Savings Fund (Mutual Fund that tracks the price of physical gold, by investing in Gold ETFs) | 0.13 (will also incur the expense of the underlying Gold ETFs) |

ETFs Vs Mutual Funds: Different Use Cases

Both ETFs and mutual funds can be part of your investment strategy for different goals. For instance, you can invest in long-term mutual fund portfolios through automated monthly SIPs, and at the same time, you can trade ETFs depending on market movements, making short-term gains.

1. Long-Term SIP: Suppose you invest INR 5,000 monthly via SIP in an index mutual fund for 10 years. The process is automated, and you benefit from rupee cost averaging.

2. Tactical ETF Trades: If you prefer timing the market or want to buy on dips, ETFs let you act instantly. For example, you can buy NiftyBees during a market correction and sell when the index recovers, potentially capturing short-term gains.

Both approaches suit different investor mindsets. While SIPs are for disciplined, long-term growth, ETFs can be used for tactical, hands-on strategies.

ETFs Are Efficient, But Are They Enough?

ETFs are great for investors who want low-cost, transparent, and flexible investing and are comfortable using trading platforms. They suit those who prefer passive management and can monitor markets.

Mutual funds, especially via SIPs, are ideal for investors seeking ease, automation, and professional management. For most Indians looking for long-term, stable wealth creation, mutual funds remain the preferred choice due to their simplicity and accessibility.

ETFs, Mutual Funds, And The Case For Diversified Alternatives

While ETFs and mutual funds can offer both equity and debt exposure, adding fixed-income assets like corporate bonds, securitised debt instruments, or corporate FDs can further stabilise your portfolio.

These alternative fixed-income instruments act as a cushion during market volatility and help balance risk, making your portfolio strategically diversified with appropriate hedging, thus making it more resilient.

Conclusion

Both ETFs and mutual funds have their unique advantages. ETFs offer flexibility and lower costs, while mutual funds provide ease of investing and professional management. The right choice depends on your investment style, goals, and comfort with trading platforms. For most Indian investors, a blend of both, along with some fixed-income products, can create a balanced and robust portfolio.

Want to explore stable fixed-income options beyond mutual funds and ETFs? Start investing with Grip Invest today.

Frequently Asked Questions

1. Which is better for beginners in India, ETFs or Mutual Funds?

Mutual funds are generally better suited for beginners due to their ease of investing, availability of SIPs, and professional management. ETFs require a demat account and understanding of market timings.

2. Are ETFs safer than mutual funds?

Both ETFs and mutual funds carry market risks. ETFs may face liquidity risk, while mutual funds can carry fund manager risk. Neither is inherently safer; it depends on the specific fund and your investment goals.

3. Can I start SIPs in ETFs like mutual funds?

SIPs are widely available for mutual funds. While some brokers offer SIP-like features for ETFs, they are not as seamless or automated as mutual fund SIPs.

4. Why are ETFs cheaper than mutual funds?

ETFs are passively managed and track an index, which reduces fund management costs. This leads to lower expense ratios compared to actively managed mutual funds.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001