Gilt Funds vs Fixed Deposits: Which Offers Better Returns In 2026?

Fixed deposits are considered a low-risk investment because they offer capital protection with low returns. It is common, especially for senior citizens, to invest in fixed deposits after retirement to secure their investment.

In recent times, government-backed gilt funds have been gaining popularity. It is a type of debt mutual fund where investments are mostly in government securities. Gilt funds offer market-linked returns.

Keep reading to learn more about gilt funds vs fixed deposits and choose a risk-free investment with high returns suitable for your financial goals.

What Are Gilt Funds?

Gilt funds are a type of debt mutual fund. According to SEBI, these must invest 80% in government securities (G Secs). The central or state governments issue these bonds to generate revenue for government operations. As these are backed by government securities, they have minimal credit risk. However, they are highly sensitive to changes in interest rates.

The fund manager is free to invest the remaining 20% of the funds in debt instruments with similar risk profiles. Based on the fund manager’s management, the risk profile of the gilt funds may also vary.

How Does It Work?

The mutual fund house pools money from investors and uses it to buy long-term government bonds. The debt mutual funds earn returns based on the bond yields and interest rate movements. Interest rates and bond rates move in opposite directions.

While they have the potential to earn double-digit returns in falling interest rates, higher interest rates can erode returns. These mutual funds are suitable for investors who can manage interest rate risks and have a longer investment horizon.

What Are Fixed Deposits?

Fixed deposits are term-based savings instruments offered by many banks and NBFCs. These are low-risk investments as the principal remains protected, and the interest rate is pre-determined. The interest earned from fixed deposits is not linked to the market, and it remains constant throughout the deposit period.

How Does It Work?

You can invest any amount of money based on the bank's policy and choose a tenure varying from 1 to 5 years or more. At the time of deposit, you will know the interest rate and returns you may receive at the end of the maturity period. At maturity, you will get back your principal and interest earned.

Key Differences: Risk, Returns, And Liquidity

As FDs have no correlation with the market, they carry low risk and offer modest returns. Gilt funds have a higher risk as they offer market-linked returns and are sensitive to interest rate changes. Breaking your fixed deposit prematurely results in a penalty, but gilt funds are more liquid compared to fixed deposits.

Here are the key differences between gilt funds and fixed deposits:

| Feature | Fixed Deposits (FDs) | Gilt Funds |

| Issuer | Banks/NBFCs | Government of India |

| Return Type | Fixed interest | Market-linked returns |

| Typical Returns (2025) | 6.5% – 7.5% | 6% – 9% (depending on interest cycle) |

| Risk | Low credit risk, no market risk | No credit risk, high interest rate risk |

| Liquidity | Premature withdrawal is allowed with a penalty | High liquidity but market-linked NAV |

| Tenure | Fixed (e.g., 1–5 years) | No fixed tenure, open-ended funds |

| Safety | Insured up to INR 5 lakh (DICGC) | Backed by the government, no default risk |

| Exit Load | Not applicable | May apply if redeemed within 3 years |

| Tax Efficiency | Interest taxed as per the slab | LTCG benefits after 3 years |

Let us now compare the historical returns of fixed deposits and gilt funds:

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||

Taxation And Exit Loads: What You Need To Know

Knowing taxation on FDs and gilt funds can help you choose the right investment1.

Taxation

For fixed deposits:

1. Interest income is added to the taxable income and taxed based on the income slab.

2. TDS of 10% (20% for NRIs) applies if the fixed deposit interest is greater than INR 50,000 for the general population and INR 1,00,000 for senior citizens.

For gilt funds:

Taxation varies based on when the investment was made.

For investments before April 1, 2023,

1. If you hold investments for less than 36 months, they will be considered short-term capital gains, and the STCG tax is based on the income slab rate.

2. If you hold the investments for more than 36 months, then the gains are long-term capital gains, and the LTCG tax of 20% applies with indexation benefits.

For investments made after April 1, 2023,

1. Income from gilt funds will be considered taxable income and taxed as per the applicable tax rate, regardless of short-term gains or long-term gains.

Exit Load

When you close fixed deposits on maturity, you will get the entire principal amount plus earned interest. If you close FDs prematurely, a penalty of 0.5% to 1% applies to the prevailing interest rate, and it can affect your returns.

For gilt funds, there is generally no exit load. However, some mutual fund houses may charge an exit load if you withdraw before a certain period. You should check the scheme and policy documents to know the exact exit load.

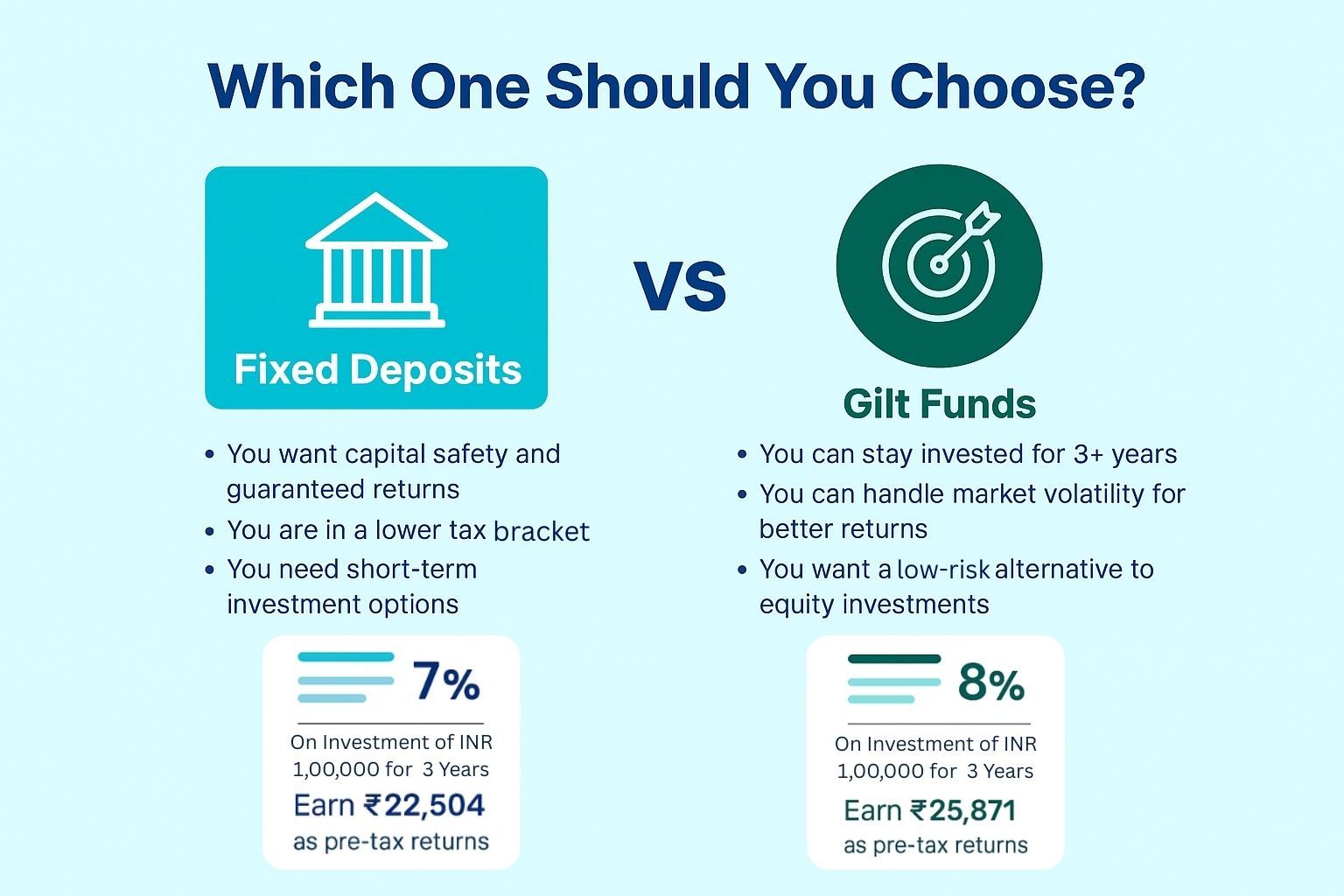

Which One Should You Choose?

Investing in gilt funds or fixed deposits depends on your risk appetite, financial goals, and investment horizon. During falling interest rates, gilt funds have historically performed better. Fixed deposits, on the other hand, offer predictable returns and capital safety, regardless of the market conditions.

Choose fixed deposits if:

- You want capital safety and guaranteed returns

- You are in a lower tax bracket

- You need short-term investment options

Choose gilt funds if:

- You can stay invested for 3+ years

- You can handle market volatility for better returns

- You want a low-risk alternative to equity investments

Let us say, for example, you invest INR 1,00,000 in 2026. FDs offer an average return of 7% for 3 years, and you can earn INR 22,504 as pre-tax returns. Gilt funds offer an average return of 8% CAGR, and you can earn INR 25,971 as pre-tax returns.

As the investment is made in 2026, taxation is similar for fixed deposits and gilt funds. Returns are added to the taxable income and taxed at your slab rate.

Conclusion

Choosing between gilt funds and fixed deposits (FDs) isn’t about which one is better, it is about what aligns with your financial goals. If you prioritise capital safety, fixed and guaranteed returns, and short-term stability, fixed deposits may suit you best. On the other hand, if you are investing for the long term, can handle interest rate fluctuations, and want exposure to government securities, gilt funds could offer better returns with relatively low credit risk.

For most investors, a smart strategy is to diversify across fixed-income instruments, combining the stability of FDs with the potential upside of gilt funds to balance risk and returns.

Explore all your options and choose an investment that fits your risk appetite, investment horizon, and financial goals.

Login to Grip Invest to discover curated opportunities in bonds, fixed-income products, and more tailored to your investment needs.

FAQs on Gilt Funds vs Fixed Deposit

1. Are gilt funds safer than fixed deposits?

In terms of credit risk, gilt funds are safer as they invest in government-backed securities, but the returns vary based on prevailing interest rates. In terms of capital protection and stable returns, fixed deposits carry lower risk.

2. Can I lose money in a gilt fund?

Yes, gilt funds offer market-linked returns, and there is a potential for short-term loss. If interest rates increase, the bond prices fall, which lowers the fund's NAV. Historically, gilt funds offer better returns if you stay invested for a longer term, such as 3-5 years, as the impact of market volatility goes down with a longer investment horizon.

3. How do interest rates impact FD vs gilt fund performance?

FD rates increase with interest hikes to benefit new investors. Gilt funds lose value when interest rates increase, but gain during falling interest rate cycles.

References:

1. The Economic Times, accessed from: https://economictimes.indiatimes.com/wealth/tax/new-tds-rules-from-april-1-higher-limit-for-tax-deduction-on-fd-interest-lottery-winnings-check-its-impact/articleshow/118889546.cms?from=mdr

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001