Gilt Funds Taxation In India: How Your Returns Are Taxed In 2026

Investing in debt mutual funds is generally more suitable for risk-averse investors, as they carry lower risk. Even though market risk with debt mutual funds is lower, they still carry interest rate and credit risk. A specific type of debt mutual fund called the gilt funds almost reduces the credit risk to nil as they invest in government securities. This makes them more suitable for investors with low-risk appetites. Let's explore the taxation of gilt funds to find out whether they fit your financial goals.

Understanding Gilt Funds

Gilt funds are open-ended debt mutual fund schemes where 80% of the investment is in government securities with different maturities. These are commonly referred to as G-Secs.

The RBI issues government securities like bonds on behalf of the government when the government needs funds for its expenses. Financial institutions like banks, insurance companies, mutual fund companies, and individual investors can buy these bonds. Government securities are usually available as treasury bills (suited for short-term borrowing) and government bonds (ideal for mid-to-long-term borrowing).

As these securities are backed by the central and state governments, they have almost no credit risk. The government pays the interest on these securities and repays the principal amount on maturity.

Gilt funds are one of the 16 debt mutual fund categories classified by SEBI.

Investors can expect stable and safe returns when they invest in gilt funds. The changing interest rates can impact the returns of gilt funds.

Since gilt funds have a low correlation to the equity market, they can serve as ideal tools for portfolio diversification.

Taxation Of Gilt Funds In 2026

1. Recent Tax Changes

Gilt funds are debt mutual funds and are taxed as such. The tax will be applicable at the time of redemption. The Union Budget 2025 didn’t introduce significant changes, but the 2023 Budget had already implemented key revisions.

As per the new changes, all gains from investments in gilt funds on or after April 1, 2023, are added to your total income and taxed according to your applicable slab rate. There is no distinction between short-term and long-term gains. So, essentially, in 2026, if you invest in gilt funds and earn returns, they will be considered as additional income and will be taxed as per your slab rate1.

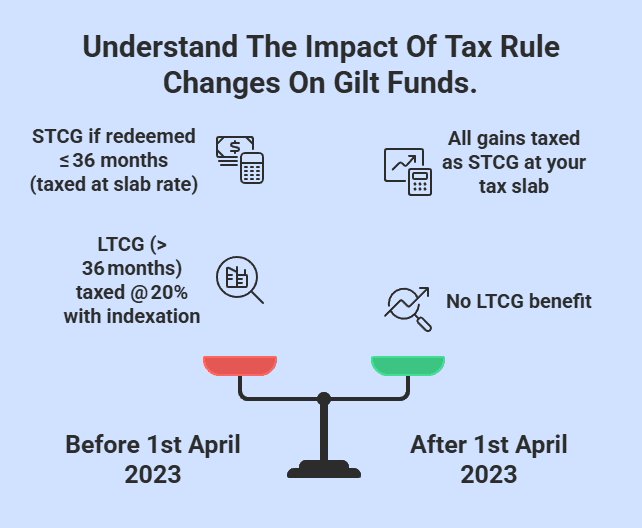

2. Taxation For Investments Made Before April 1, 2023

If you invested in gilt funds before April 1, 2023, your tax treatment depends on how long you held the investment and when you sold it.

Short-Term Capital Gains (STCG)

- If you sold your gilt fund before July 23, 2024, and held it for less than 36 months, your gains are considered short-term and taxed at your income tax slab rate.

- If you sold it on or after July 23, 2024, and held it for less than 24 months, the gains are still treated as short-term and taxed at your slab rate2.

Long-Term Capital Gains (LTCG)

- For gilt funds bought before April 1, 2023 and sold before July 23, 2024, if held for more than 36 months, gains are considered long-term and taxed at 20% with indexation benefits.

- For those sold on or after July 23, 2024, if held for more than 24 months, the gains are taxed at a flat 12.5% rate, without indexation2.

3. Taxation For Investments Made On Or After April 1, 2023

All types of investments in gilt funds made after April 1, 2023, are considered short-term gains, regardless of the holding period. So, the returns are taxed based on your applicable slab. There are no indexation benefits.

Given below is an overview of the taxation of gilt funds:

Investment Type | Holding Period | LTCG Tax | STCG Tax |

Acquired before 1st April 2023 | >36 months (sold before July 23, 2024) | 20% with indexation benefit | Slab rate |

Acquired before 1st April 2023 | >24 months (sold on or after July 23, 2024) | 12.5% (no indexation) | Slab rate |

Acquired on or after April 1, 2023 (any sale date) | No holding period is required | Slab rate (LTCG concept not applicable) | Slab rate |

4. Taxation Of IDCW (Income Distribution Cum Capital Withdrawal)

IDCW plans provide dividend payouts, depending on the scheme’s performance and declared frequency. Investors who receive these payouts are taxed on the returns. The dividend payouts are also considered ordinary income, and they are added to the income of the investors and taxed at a slab rate.

In case the dividend income is more than Rs. 5000 in a financial year, the fund house offering gilt funds may charge 10% TDS on such income3.

Using Gilt Funds For Tax Planning

Newer investments in gilt funds after April 1, 2023, carry no significant tax benefits as they are taxed at the slab rate. Pre-April 2023 investments that are held for more than 24 months can access an LTCG rate of 12.5%.

When the slab rate favours you, you may hold gilt funds for longer for maximum capital appreciation. If your total income is less than INR 7,00,000 under the new tax regime, you may be eligible for a INR 25,000 rebate under Section 87A. For low-income earners following the old tax regime, the tax rebate applicable is INR 12,500 for income less than INR 5,00,000.

Conclusion

Gilt funds offer a sovereign-backed, interest-sensitive investment avenue. However, taxation rules shifted dramatically in April 2023, marking a transition from indexation-linked LTCG benefits to uniform slab-based taxation. Understanding these nuances helps you invest in gilt funds strategically, especially in tax planning and liquidity management. To learn more about investments and tax planning sign-up on Grip Invest today.

Frequently Asked Questions On Gilt Fund Taxation

1. What’s the tax rate on gilt fund returns in 2025?

Following are the tax rates applicable on Gilt Fund returns in 2025:

- Pre-2013 units (?24 Months): LTCG @ 12.5%

- Others: Slab rate (likely 20–30%)

2. Are gilt funds suitable for tax-saving purposes?

No specific deductions are available. Gains follow slab or LTCG, depending on the period. They are best suited for portfolio diversification and adding stable income to overall portfolio returns.

3. Can NRIs invest in gilt funds, and what are the tax implications?

Yes, NRIs can invest in gilt funds. However, the applicable TDS is 20%, and income is taxed at the slab rate.

References:

- The Economic Times, accessed from: https://economictimes.indiatimes.com/mf/analysis/how-are-gilt-mutual-funds-taxed/articleshow/107865360.cms?from=mdr

- ET Money, accessed from: https://www.etmoney.com/learn/mutual-funds/taxation-in-mutual-funds/

- AMFI, accessed from: https://www.amfiindia.com/investor-corner/knowledge-center/tax-corner.html

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001