SIP Investment Tax Benefits: What Indian Taxpayers Must Know In 2026

What Is SIP And How Does It Work In Mutual Funds?

A Systematic Investment Plan (SIP) allows investors to contribute a fixed amount regularly (such an example- monthly or quarterly) into mutual funds, fostering disciplined investing. SIPs are highly popular in India just because of their affordability, flexibility, and potential for prosperity creation through the method of compounding. Investors can start with as little as INR 500 per month, making it accessible for beginners and seasoned investors alike.

SIPs work by pooling money from multiple investors to buy a diversified portfolio of stocks, bonds, or other securities. The investment amount is deducted automatically from the investor’s bank account and it’s allocated to the chosen mutual fund scheme. Over the period, SIPs give the benefits from rupee cost averaging, which mitigates market volatility by spreading investments across market cycles (SEBI, 2023).

For an illustration, investing INR 5,000 monthly in an equity mutual fund over 10 years at an average annual return of 12% could grow to approximately INR 11.6 lakh, as calculated using the compound interest formula:

FV = P × [(1 + r/n)^(nt) - 1] / (r/n),

where FV is future value, P is the periodic investment, r is the annual rate, n is the number of compounding periods per year, and t is the time in years.

Are SIPs Eligible For Tax Deductions Under Section 80C?

Under Section 80C of the Income Tax Act, 1961, Indian taxpayers can claim deductions up to INR 1.5 lakh annually on eligible investments, including certain mutual funds. However, not all SIPs qualify for this benefit.

Only SIPs in Equity-Linked Savings Schemes (ELSS) are eligible for Section 80C deductions, subject to a three-year lock-in period.

Comparison: ELSS vs. Regular Equity/Debt Mutual Funds

Feature | ELSS Mutual Funds | Regular Equity Mutual Funds | Debt Mutual Funds |

Section 80C Eligibility | Yes, up to INR 1.5 lakh | No | No |

Lock-in Period | 3 years | No lock-in | No lock-in |

Risk Level | High (equity-based) | High (equity-based) | Low to moderate (bond-based) |

Expected Returns | 12–15% (historical average) | 10–14% (historical average) | 6–8% (historical average) |

Taxation on Gains | LTCG > INR 1.25 lakh taxed at 12.5% | LTCG > INR 1.25 lakh taxed at 12.5% | Taxed as per income slab (post-2023) |

Source: AMFI, 2024

ELSS funds are ideal for taxpayers seeking both tax savings and wealth creation. For instance, investing INR 1.5 lakh annually via SIPs in an ELSS fund can reduce taxable income while offering equity market exposure. Regular equity or debt mutual funds, while flexible, do not offer Section 80C benefits (Income Tax Department, 2024).

Taxation On SIP Returns: Capital Gains Rules

The tax treatment of SIP returns depends on the type of mutual fund (equity or debt) and the holding period. As of 2025, recent budget changes have updated capital gains tax rates.

Equity vs. Debt Fund Taxation

Understanding how mutual fund returns are taxed is essential for effective financial planning. This section compares the tax treatment of equity mutual funds (including ELSS) with that of debt funds, reflecting the latest changes introduced in the Union Budget 2024.

From holding period rules to applicable tax rates, here's how your gains may be taxed depending on the type of mutual fund you invest in.

Equity Mutual Funds (including ELSS):

- Long-Term Capital Gains (LTCG): Gains from units held for more than 12 months are taxed at 12.5% (previously 10%) if they exceed INR 1.25 lakh annually (Union Budget, 2024).

- Short-Term Capital Gains (STCG): Gains from units held for less than 12 months are taxed at 20% (previously 15%).

Example: If you redeem ELSS SIP units worth INR 2 lakh after 3 years, with a gain of INR 50,000, only INR 25,000 (INR 50,000 - INR 1.25 lakh exemption) is taxable at 12.5%, resulting in a tax of INR 3,125.

Debt Mutual Funds:

As per the Finance Act 2023, gains from debt mutual funds (irrespective of holding period) are taxed at the investor’s income tax slab rate.

Example: A INR 50,000 gain from a debt fund SIP for an investor in the 30% tax bracket incurs INR 15,000 in taxes.

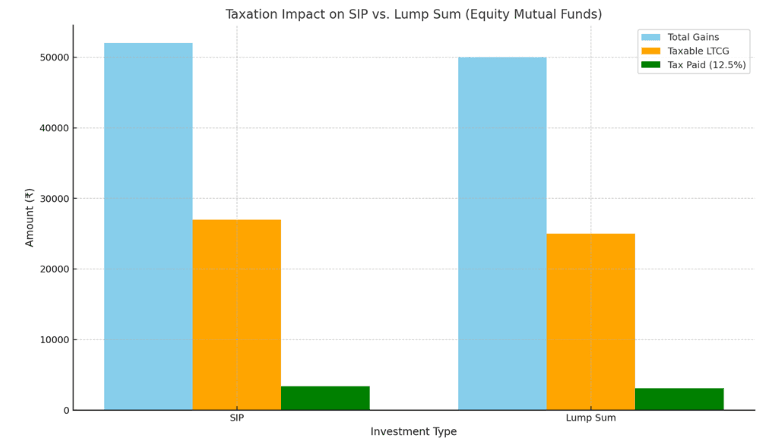

SIPs vs. Lump Sum: How Taxation Differs

SIPs involve multiple purchase dates, so each installment is treated as a separate investment for tax purposes. The holding period for each SIP unit is calculated individually, which can complicate tax calculations compared to lump-sum investments, where all units have the same purchase date.

(Hypothetical scenario: INR 1.5 lakh invested, 12% annual return, redeemed after 3 years)

Investment Type | Total Gains | Taxable LTCG | Tax (12.5%) |

| SIP | INR 52,000 | INR 27,000 | INR 3,375 |

| Lump Sum | INR 50,000 | INR 25,000 | INR 3,125 |

Note: SIP gains vary slightly due to rupee cost averaging.

Source: Calculated using standard mutual fund return formulas.

How To Maximize Tax Savings With SIPs

1. Invest in ELSS Funds: Allocate the full INR 1.5 lakh Section 80C limit to ELSS SIPs to combine tax savings with potential high returns.

2.Spread Investments Across Tax Years: Start SIPs early in the financial year to maximize compounding benefits within the lock-in period.

3. Monitor Holding Periods: Hold equity fund SIPs for over 12 months to benefit from lower LTCG tax rates.

4. Use Tax Harvesting: Redeem and reinvest gains below INR 1.25 lakh annually to utilize the LTCG exemption (AMFI, 2024).

5.Consult a Financial Advisor: Tailor SIP investments to your risk profile and tax bracket for optimal results.

Conclusion

SIP investments provide a disciplined path to long-term wealth creation, and ELSS funds offer the added benefit of tax savings under Section 80C. By understanding capital gains taxation and strategically planning their SIPs, Indian taxpayers can optimise returns while minimising tax liabilities. It’s always advisable to consult a financial advisor to ensure your investments align with your financial goals. Login to Grip Invest if you wish to explore diversified investment options beyond mutual funds and get access to curated fixed-income opportunities.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001