Tax on Debt Mutual Funds (2026): STCG, LTCG, New Rules Explained

Understanding the tax on debt mutual fund investments is crucial, especially after the 2023 rule changes. While these funds are preferred by low-risk investors for stability, their post-tax returns can vary widely. This makes it essential to know how capital gains from debt mutual funds are taxed in 2025 and how it impacts your overall investment returns.

In this blog, we will take a detailed look at the tax on debt mutual funds in 2025.

Understanding Debt Mutual Funds And Their Taxation

A mutual fund scheme is considered a debt mutual fund if it invests more than 65% of its portfolio in debt and debt-related instruments. Debt mutual funds invest in fixed-income securities and carry less risk as compared to equity mutual funds.

The taxation rules for debt mutual funds are based on holding periods, types of income like capital gains or interest income, and the residency status of the investors.

Latest Tax Rules For Debt Mutual Funds

Let us understand the latest 2025 debt mutual fund taxation rules in detail:

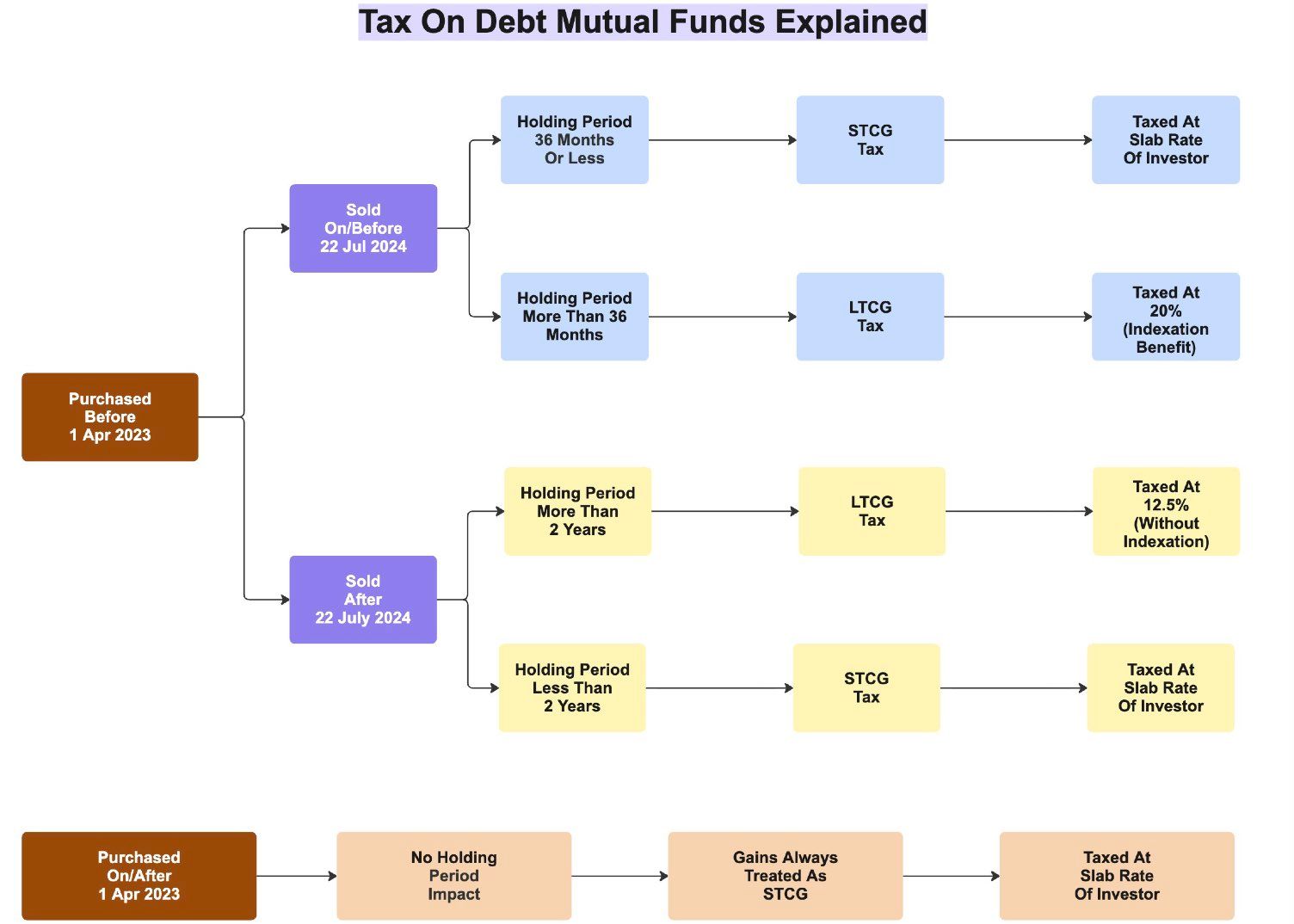

1. Taxation For Investments Made (BEFORE) April 2023

Tax on Debt mutual fund investments made before 1st April 2023 is as follows -

1. It will be treated under long-term capital gains (LTCG) if held for longer than 24 months in the case of unlisted schemes and 12 months for listed schemes. (being sold on or after 23rd July 2024)

2. LTCG on debt mutual funds will be taxed at 12.5% without indexation benefit. The benefit of indexation has been completely removed.

3. If the debt mutual fund returns are redeemed before 24 months, it will be taxed as short-term capital gains, based on the individual tax slab.

2. Taxation For Investments Made (AFTER) April 2023

The debt fund capital gains tax on investments made after 1st April 2023 will be added to an individual's taxable income and taxed at their respective slab rates.

Irrespective of the holding period, there will be no classification as long-term or short-term capital gains. There will be no debt mutual fund indexation benefit either.

For example: Mr A invested INR 20,00,000 in a debt mutual fund on 10th April 2023 and sold the investment for INR 24,00,000 on 30th March 2025, making a profit of INR 4,00,000. Assuming he has no other income, the gains will be taxed on his applicable tax slab.

| Particulars | Amount |

| Slab Applicable (FY24 - 25) | 3,00,001 - 7,00,000 |

| Slab Rate | 5% above INR 3,00,000 |

| Tax Applicable | 5% of INR 1,00,000 = INR 5,000. |

Mr. A will be paying a STCG of INR 5,000 according to his applicable slab rate.

We can understand that the new tax rules for debt mutual funds are a little complex due to the different timelines of purchase and redemption dates involved. Hence, we have prepared a flow diagram below to make it clear for everyone:

Important Note:

There is no LTCG exemption limit for debt mutual funds—entire long-term gains are taxable at the prescribed rate, with no threshold exemption. The INR 1,25,000 limit applies only to equity-oriented mutual funds and shares.

3. Post-July 2024 Updates: The definition of “specified mutual funds” has been clarified. The holding period for LTCG on the legacy investments is now the same as the holding period for the current investments, a minimum of 24 months. The new legislation will clarify how to handle fund-of-funds and hybrid mutual funds.

The evolution of tax treatment over time has followed similar lines to fixed income products such as fixed deposits, resulting in a shift toward increased consistency.

Budget 2026 Impact On Debt Funds

No major modifications were introduced in the Budget 2026 with regard to tax implications for debt mutual funds. The slab-rate structure under Section 50AA remains unchanged from previous years. While there were some minor changes made to general capital gains, borrowing from a debt fund will continue under the same framework as in the past to provide security to investors planning for 2026 and beyond.

1. Section 87A Rebate and Its Benefit for Debt Fund Investors

The Section 87A Rebate on taxes will remain applicable for individual residents of India. If you have an overall income, inclusive of your debt fund income, below the eligibility limits then you should be able to claim this rebate.

This will thus help to significantly reduce or eliminate tax due on your slab-rate gains. This rebate continues to provide relief for both middle and lower-middle income investors even with the introduction of slab-rate taxation going forward.

2. NRI Investors: TDS and Taxation Rules

All foreign investors will have to pay TDS on the gains from their debt investments at applicable non-resident TDS rates when making distributions on their debt fund.

If they file for an income tax return in India and claim credit for the TDS that has been paid then they will be subject to the provisions of double taxation agreements between India and their county of residence which may provide additional benefits. Therefore, proper documentation should be kept by NRIs to comply with TDS regulations.

3. Current Tax Rules for Debt Mutual Funds in 2026

Tax rules as of 2026 for debt mutual fund investments will largely follow simple taxation. Specifically, those investment units purchased after April 1, 2023 will be taxed as 100% STCG on debt funds at your applicable income tax rate.

There is no separate ‘long-term’ category of investment to be recognised, nor will you have any indexation benefit associated with these investments.

As for assets acquired prior to April 2023, debt fund LTCG after July 2024 will become eligible after 7/31/2024 provided they are held for at least 24 months. These capital gains will be taxed at a flat rate and without any indexation benefit. Thereby providing some degree of support to existing long-term holders of legacy debt mutual funds.

4. Section 50AA Income Tax Explained Simply

In Section 50AA, debt mutual fund taxation 2026 are defined to be those mutual funds that invest at least 65% of their total assets in specified types of debt and money market securities.

Capital gains on these types of mutual funds will be treated as short-term capital gains starting in the 2026 tax year.

This change will put all debt mutual funds on a tax basis equal to that of bank fixed deposits and will eliminate the previous tax advantage associated with debt mutual funds.

Comparison With Fixed Deposits Taxation

Here is the comparison between fixed deposits and debt mutual funds taxation:

Particulars | Debt Mutual Funds | Fixed Deposits |

| Tax on Gains | Taxed on slab rates | Interest income taxed at slab rates |

| Indexation benefit | Not available | Not available |

| Holding Period | No impact | No impact |

After April 2023, debt mutual funds and fixed deposits will have similar taxation. The gains on debt funds and interest income on fixed deposits are taxed at individual income tax slab rates.

Neither debt mutual funds nor fixed deposits are impacted by holding periods or tenure, and neither of them offers indexation benefits.

Types Of Taxes On Debt Mutual Funds

Here are the different types of debt mutual funds' tax charges:

1. Short-Term Capital Gains (STCG) on Debt Funds

A debt mutual fund investment will be treated under STCG if:

- Investment is made before 1st April 2023 and held for less than 24 months.

- Investment is made after 1st April 2023, regardless of the holding period.

STCG on debt funds will be taxed at the slab rate of the individual.

2. Long-Term Capital Gains (LTCG) and Indexation Changes

LTCG in debt mutual funds is applicable only if the investment was made before 1st April 2023 under the following conditions -

- Investment is held longer than 24 months and is being sold on or after 23rd July 2024.

- A tax of 12.5% is applicable.

- No indexation benefit.

Earlier, the gains on debt mutual funds, sold before 23rd July 2024, where investment was made before 1st April 2023, were –

- Taxed at 20% LTCG tax2.

- The indexation benefit was available.

- The holding period cut-off was 36 months.

3. Dividend Taxation on Debt Mutual Funds

The Income Distribution cum Capital Withdrawal or IDCW option in debt mutual funds allows investors to receive periodic payouts from the scheme’s profits (not guaranteed).

Since April 1, 2020, payouts or dividends from IDCW are added to the investor’s total income and taxed according to their income slab, as the Dividend Distribution Tax (DDT) has been abolished.

A TDS of 10% is deducted if the dividend income is higher than INR 5,0005.

4. Tax Deducted at Source (TDS) For NRIs

Debt mutual funds tax for NRI or Non-Resident Indians consists of a tax deducted at source:

- A 20% TDS (or the rate specified under the relevant Double Taxation Avoidance Agreement, whichever is lower) is deductible for NRIs on dividends from debt mutual funds.

- For redemption on debt mutual funds, a TDS of 30% is levied on capital gains.

For resident investors, a 10% TDS is deducted on IDCW payouts exceeding INR 5,000 in a financial year, while no TDS applies on capital gains.

Also, no Securities Transaction Tax or STT is levied on debt mutual fund transactions, only on equity-oriented schemes.

Strategies To Save Tax On Debt Mutual Funds

Let us look at some tax strategies for debt mutual fund investors:

1. Use Growth Option: Instead of availing dividends, you can choose a growth option in debt mutual funds, where your dividends are reinvested and allow your investment to compound.

Otherwise, if you receive dividends each year, you will be liable to pay taxes.

2. Utilise 87A Rebate Benefit: In FY26, under section 87A of the IT Act, a tax rebate of INR 60,000 is allowed on incomes up to INR 12 lakhs. This effectively makes income up to INR 12 lakhs tax-free. This includes gains from debt mutual funds.

This creates a significant opportunity for middle-income investors to realise capital gains on debt mutual funds tax-free, provided they stay within the threshold.

How To File ITR For Debt Fund Gains (Step-by-Step)

With new technologies, filing taxes on redemptions from a debt fund is now much simpler:

Step 1. Visit either the mutual fund company or an aggregator site to download your Capital Gain statement.

Step 2. Use apps such as Groww or ClearTax that allow for the direct import of your transaction data.

Step 3. On your ITR-2 or ITR-3, report the capital gains under the Capital Gains Schedule.

Step 4. The software will automatically apply slab rates, as of about 2023, to all capital gains that were created from the post-2023 investment.

Step 5. When you complete filing your taxes, ensure all entries were entered correctly, and file your tax return before the date shown on your form.

These tools minimise errors and save time, especially if you have multiple redemptions.

Fund-of-Funds And Gold Fund Tax Treatment

When it comes to Fund of Funds (FoF), it is a debt-oriented FoF that primarily invests in other legal Funds (FoFs). They are treated like a direct debt fund under Section 50AA, meaning any gains from the FoF will be taxed at slab rates.

Gold Funds and Gold ETFs or exchange traded funds are technically not a class of debt funds because they invest primarily in gold assets. All long-term capital gains from gold funds will qualify as long-term capital gains for any investment held longer than 24 months. Gold Funds and Gold ETFs will be treated differently when it comes to filing taxes under the current capital gains rules.

Therefore, always review the Asset Allocation of any fund in which you are considering investing in order to determine the exact tax treatment of your investment.

Tax-Saving Alternatives To Debt Mutual Funds

If you're considering an investment in fixed income securities but would like more tax-efficient options, there are a few possibilities that can help you achieve your goal.

- Corporate Bonds and Government Securities: These can create less complexity with tax issues when held directly until maturity over time, typically at a lower cost than purchasing through a broker.

- Sovereign Gold Bonds (SGBs): Interest on these bonds is taxable; however, capital gains will not be taxed for the original subscribers at maturity.

- Tax-free bonds (where still available): The interest on the bonds is fully tax exempt.

- Fixed Deposits (FD) with special senior citizens benefits or similar targeted investment schemes, typically offering a slightly higher interest rate compared with other aged-related savings accounts.

Companies such as Grip Invest list specifically curated bond options and should be considered by those seeking to help replace or supplement debt funds within their portfolios.

Debt Fund vs FD Taxation: Which is Better?

Now that debt funds are taxed like Fixed Deposits (FDs), there are still some clear differences:

1. Debt funds have a lot better liquidity, you can redeem anytime without breaking the deposit.

2. Since professional management runs debt funds, they tend to produce slightly more than FDs in stable interest rate environments.

3. Ds offer guaranteed returns and more straightforward methods of tracking interest earned.

4. Debt Funds can expose you to low interest rate and credit risk, but unlike banks that offer FDs, they are not guaranteed to protect your against default loss (up to INR 5 Lac per depositor).

As such, many investors now use liquidity and maximum expected return as their chief way to compare the tax implications of debt funds versus FDs instead of just tax savings.

Currently, the Debt mutual fund taxation 2026 structure is changed to no longer having the former indexation provisions; nevertheless, you can benefit from using the indexation as a reference for you in your overall asset investment management plan through a debt-oriented mutual fund's portfolio.

By understanding STCG on debt funds, Section 50AA income tax, and available rebates, you can optimise your fixed-income portfolio effectively.

With the rules now stable, focus on selecting funds that match your risk profile and liquidity needs. Regular review and use of helpful platforms will make tax compliance hassle-free.

Conclusion

The capital gains on debt mutual funds are taxed at the slab rate of the individual if the investment is made on or after 1st April 2023. If the investment is made before that date, a LTCG tax is levied on the gains. The dividends received from debt mutual funds are also taxable at the slab rate of the individual. Investors must properly understand the tax implications of debt mutual funds before investing.

Sign up to Grip Invest and explore more!

FAQs On Debt Mutual Fund Taxation

References

1. The Business Today, accessed from: https://www.businesstoday.in/personal-finance/tax/story/as-mf-investor-are-my-gains-excluded-from-the-section-87a-rebate-calculation-under-new-tax-regime-in-fy2025-26-474519-2025-05-02

2. The Business Today, accessed from: https://www.businesstoday.in/personal-finance/tax/story/budget-2025-ltcg-for-mutual-funds-got-revised-in-budget-2024-how-investors-got-impacted-457885-2024-12-19

3. The Economic Times, accessed from: https://economictimes.indiatimes.com/wealth/tax/dividend-received-from-shares-and-mf-is-taxable-heres-how-to-reduce-your-tax-outgo-from-dividend-income-in-your-itr/articleshow/111655050.cms

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001