Complete Guide To Taxation On Bonds In India (2026)

In today's dynamic investment landscape, bonds have emerged as a compelling choice in the investment landscape. These fixed-income instruments offer a unique blend of benefits – lower risk compared to stocks, better returns than traditional fixed deposits, and a steady income stream.

Like other investment avenues, it is crucial to consider the taxation on bond investments in India. Before investing in bonds, study all the information and pay close attention to decoding the tax effects.

Taxation On Bonds In India And It's Impact

1. Taxable Bonds

Regular bonds generate returns through dual channels: periodic interest income and capital gains. The interest income is incorporated into the investor's annual taxable income and is subject to taxation on bonds at the applicable marginal rate. Capital gains taxation follows a structured framework based on listing status.

Capital gains occur when a bond is sold for more than its purchase price. It is different for listed and unlisted bonds. For listed bonds, short-term capital gain (STCG) is taxed at applicable slab rates if a bond is redeemed before 12 months; otherwise, long-term capital gain (LTCG) is taxed at 10% without indexation.

For unlisted bonds, short-term capital gain (STCG) is taxed at applicable slab rates if a bond is redeemed before 36 months. If the holding period is more than 36 months, LTCG is taxed at 20% without indexation.

2. Tax-Free Bonds

Government institutions and Public Sector Undertakings frequently issue tax-free bonds to facilitate infrastructure development. These instruments offer the distinctive advantage of tax-exempt interest income, enhancing effective yields for investors. However, it should be noted that capital gains realised upon disposal remain within the tax framework, with applicable rates determined by the holding duration.

3. Tax-Saving Bonds

There are two types of tax-saving bonds:

- Tax- Saving Bonds Under Section 80CCF

Tax-saving bonds under Section 80CCF are government-issued securities that provide investors with tax advantages. Section 80CCF bonds serve a dual purpose, generating returns while enabling investors to claim deductions up to INR 20,000 from their taxable income.

These Section 80CCF bonds allow an additional deduction of up to INR 20,000, over and above Section 80C. They were issued mainly by government-backed bodies like NHAI and REC. Although no new issuances have come recently, older investments still follow their original tax rules.

Example: If your taxable income is INR 10 lakh and you invest INR 20,000 in 80CCF bonds, your taxable income becomes INR 9.8 lakh.

- Capital Gains Exemption Bonds Under Section 54EC

Capital gains exemption bonds under Section 54EC are government-issued instruments that allow individuals to save tax by investing capital gains from selling assets like stocks or property. Investors can invest in these bonds within six months of sale to avoid long-term capital gain tax (LTCG). Section 54EC bonds provide an intricate tax management system, particularly valuable for investors seeking to optimise capital gains tax exposure from asset disposals.

54EC bonds let investors avoid paying LTCG tax from the sale of property or other long-term assets. The maximum investment allowed is INR 50 lakh in one financial year. These bonds have a 5-year lock-in period and offer around 5% annual interest (taxable).

Example: If you sell property and make LTCG of INR 30 lakh, investing the full INR 30 lakh in 54EC bonds exempts the entire gain from tax.

To understand how much your bond investment can grow over time, use a bonds calculator to calculate estimated returns and compare different investment scenarios

4. Zero-Coupon Bonds

Zero-coupon bonds have a different type of investment structure, and they are not like other interest-bearing securities. These instruments are issued at a discount on face value, and the difference between the two represents the investment return at maturity. The returns are taxed according to the holding period, which creates opportunities for strategic tax planning across financial years.

Tax Treatment of Accrued Interest

Zero-coupon bonds don’t pay interest every year. Instead, you buy them at a discount and get the full face value at maturity. The difference is treated as your income. For tax purposes, this amount is considered capital gains. If you hold the bond for more than a year, it is taxed as long-term capital gains at 10%. If you sell it earlier, it becomes short-term capital gains and gets taxed according to your income slab.

Indexation Benefits

These bonds do not offer indexation benefits anymore. This simply means you cannot adjust your purchase cost for inflation, so the taxable gain may end up being slightly higher.

Strategic Tax Planning

Even without indexation, zero-coupon bonds can be used smartly for tax planning. You can choose a maturity year when your income is lower, reducing your short-term tax impact. And if you hold the bond for more than a year, you automatically benefit from the lower long-term capital gains tax rate.

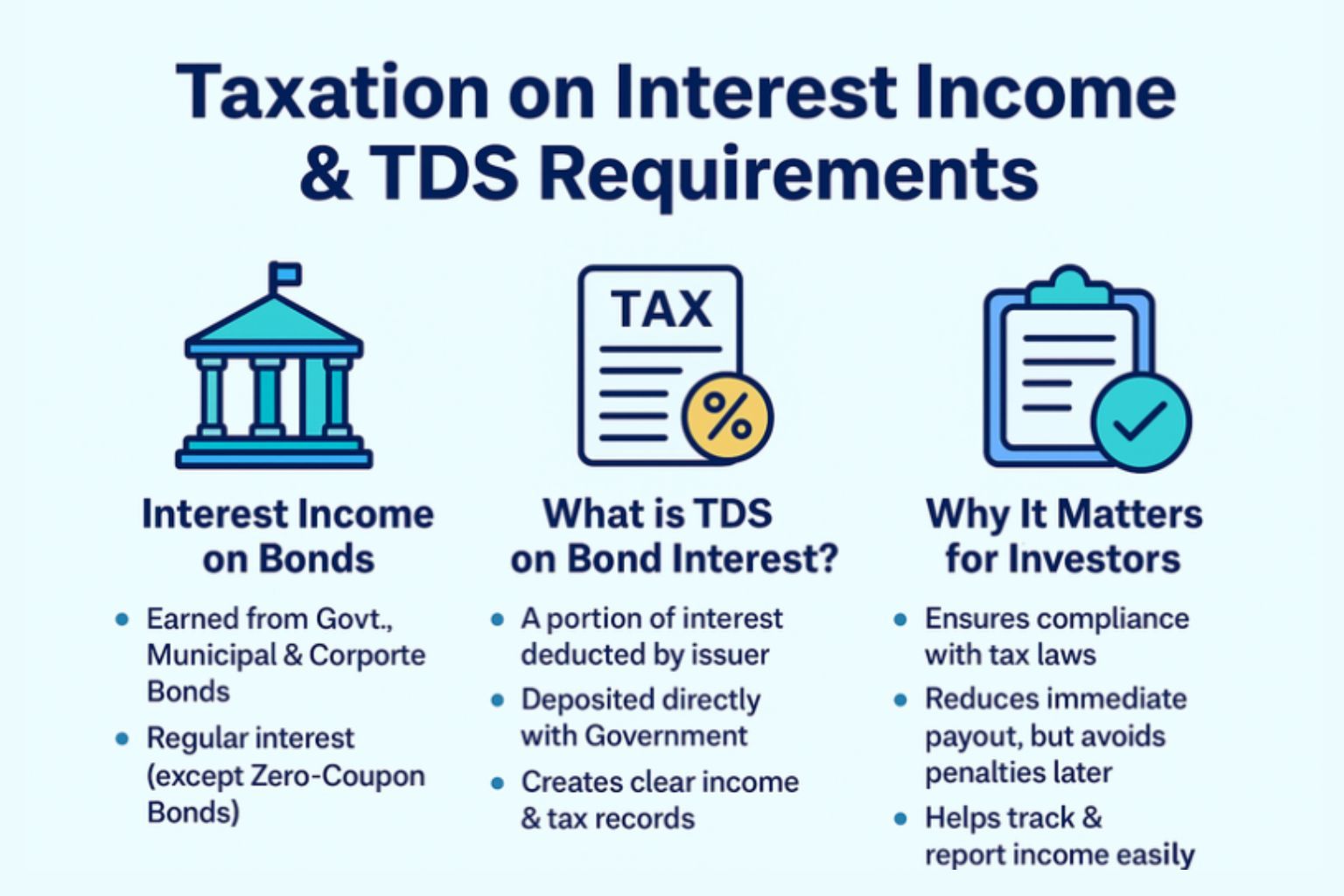

Taxation On Interest Income And The TDS Requirements

When you step into the world of bond investments, understanding taxation on bonds - whether government, municipal, or corporate bonds - you will earn regular interest payments (except for zero-coupon bonds). This interest income, similar to what you earn from bank deposits, is subject to taxation and typically involves tax deduction at source (TDS). Understanding how this works is crucial for managing your investment returns effectively.

The concept of TDS on bond interest is straightforward but important to understand. When bond issuers pay you interest, they're required by law to deduct a portion of it as tax and deposit it with the government on your behalf. This process ensures regular tax collection and helps maintain clear income records for both investors and tax authorities.

Let us give you an example to help you understand:

Consider an investment in a State Bank of India (SBI) infrastructure bond that generates quarterly interest payments of INR 25,000. The bond issuer will automatically deduct 10% TDS, which amounts to INR 2,500, before transferring the remaining INR 22,500 to your account. Over the course of a year, your total interest earnings would be INR 100,000, from which INR 10,000 would be deducted as TDS, leaving you with net receipts of INR 90,000. This systematic deduction process simplifies tax compliance while ensuring steady government revenue collection.

When filing your tax return, you must report the entire interest amount of INR 100,000, not just the amount you received after TDS. If you're in the 30% tax bracket, your total tax would be INR 30,000. With INR 10,000 already paid through TDS, you'd need to pay the remaining INR 20,000.

Looking for fixed-income opportunities that align with your financial goals? Explore corporate bonds, SDIs, and other fixed-income investment options on Grip Invest and make informed decisions while optimizing tax efficiency.

Differences In Taxation For NRIs On Bonds In India

Investing in Indian bonds can be attractive for NRIs, but their tax treatment differs from resident investors. Understanding bond taxation for NRIs in India is essential because the rules differ significantly from those for resident investors.

Tax On Interest Income

NRIs earning interest on bonds held in an NRO account are taxed at a flat 30% TDS, plus surcharge and cess. If the investment is made through an NRE account, certain bonds may offer tax-free interest, depending on eligibility and RBI rules. Unlike residents, NRIs do not get basic exemption limits on interest income; TDS is deducted upfront.

Tax On Capital Gains

Capital gains rules for NRIs mirror those for residents. Short-term gains are taxed at slab rates, while long-term gains on listed bonds are taxed at 10% without indexation. However, NRIs are subject to automatic TDS on capital gains, regardless of whether the gain is short-term or long-term.

DTAA Benefits

NRIs living in countries that have a Double Taxation Avoidance Agreement (DTAA) with India can claim relief on interest income. DTAA may reduce the TDS rate to 10–15%, depending on the treaty. To avail the benefit, NRIs must provide a Tax Residency Certificate (TRC), Form 10F, and a self-declaration.

Repatriation Rules

Investments made from an NRE account are fully repatriable, including interest and maturity proceeds. NRO investments are repatriable up to USD 1 million per financial year, subject to documentation and tax clearance.

Capital Gains Tax On Bond Investments Made In The Secondary Market

When investors trade bonds in the secondary market, they look to make a profit from the difference between the purchase and selling prices, which is referred to as capital gains. The tax on these gains depends on the holding period of the bond and whether it is listed or unlisted. For listed bonds, a shorter period of holding results in short-term capital gain taxable at the investor's applicable income tax slab rate. It gets taxed at a flat rate of 10 percent in case of holding periods beyond 12 months. The rules differ for unlisted bonds, which fall under corporate bond taxation norms.

If the bonds are held for 36 months or less, then the short-term capital gains are taxed according to the investor's income tax slab rate. However, if they are held for more than 36 months, then the long-term capital gains are taxed at 20%, without indexation. Knowing these tax implications helps investors make better decisions while trading bonds in the secondary market and comply with tax laws.

Tax Implications of Bond Redemption vs Sale in the Secondary Market

Understanding how tax differs between redeeming a bond at maturity and selling it in the secondary market helps investors plan their exits better. The tax outcome mainly depends on the holding period and whether the gain arises from maturity value or market-driven pricing.

Redemption at Maturity

When a bond is redeemed on its maturity date, taxes apply only if there is a gain. If the bond was bought at face value, no capital gain arises. But if it was purchased at a discount, the difference is treated as capital gains. For listed bonds held over 12 months, this is taxed at 10% without indexation, while unlisted bonds held over 36 months attract 20% tax without indexation.

Sale in the Secondary Market

Selling a bond before maturity triggers capital gains based on how long it was held. Short-term gains are taxed at slab rates, while long-term gains follow the 10% (listed) or 20% (unlisted) structure. Unlike redemption, sale prices can fluctuate, which means investors may also incur capital losses.

Difference: Redemption usually results in little to no taxable gain unless the bond was bought below face value. Secondary-market sales, however, are influenced by market conditions, creating the possibility of higher gains or losses.

Types Of Debt Investment With Tax Benefits

The table below highlights the type of debt investments and taxation on interest income.

Bond | Description | Interest Income And Taxation | Capital Gain |

54EC | Investors can avoid capital gains on bond taxes on long-term asset sales by buying 54 EC bonds and investing in them within six months of the sale. This helps the investor by preserving their hard earned money as they would have to pay less bond taxes. | The 54 EC bonds have a fixed interest rate of 5% p.a. The interest income is taxable at the normal rates. | 54 EC bonds have a 5-year lock-in term. They are exempt from capital gain tax if held till maturity. |

Bonds issued by government agencies like HUDCO and IREDA are not subject to income tax up to a maximum capital of INR 20,000. | These bonds have a tax free interest as per Section 10 of the Income Tax Act of 1961. | Profits that are made after selling these bonds attract capital gains tax. | |

Sovereign Gold Bonds (SGBs) | The Gold Monetisation Scheme introduced Sovereign Gold Bonds in November 2015. It enables individuals to invest in gold with denominations starting at 1 gram. | The proposed interest rate on SGBs is 2.5% per annum. It is taxable under the income category from other sources at the investor’s applicable slab rates. | According to Section 47 (VIIC) of the Income Tax Act, SGBs are tax-exempted if held until their 8-year maturity. |

Conclusion

Bonds are a reliable investment option, offering predictable fixed-income returns with low risk. However, understanding bond taxation is crucial for effective financial planning. Familiarity with concepts like taxation on bonds in India, provisions like 80CCF, and corporate bond taxation helps investors optimise their portfolios. Stay informed about the latest in investments and taxation by following Grip Invest.

Frequently Asked Questions on Taxation On Bonds In India

1. Is TDS applicable on bonds?

Yes, Tax Deducted at Source (TDS) is applicable on bond interest and is generally charged at 10%.

2. How much TDS is deducted from bonds?

The rate of TDS deducted on bonds can vary, but the standard rate is typically around 10%.

3. How do I claim TDS on bond interest?

To claim TDS on bond interest, you need Form 16A or a TDS certificate from the bond issuer. Ensure the deducted TDS is reflected in your Form 26AS for the relevant financial year. This information can be used when filing your income tax return to claim credit for the TDS amount.

4. Are RBI bonds tax-free?

No, RBI bonds are not tax-free; their interest income is taxable as per your income tax slab.

5. How to calculate capital gain on bonds?

Capital gain is calculated as the difference between the selling price and the purchase price of the bond.

6. Do bonds pay interest monthly?

Most bonds pay interest semi-annually or annually, but some may offer monthly payouts.

7. What is the difference between tax on bond redemption and sale?

Tax on redemption applies when the bond matures, while tax on sale applies when you sell it earlier; both are treated as capital gains based on the holding period.

8. How do Section 54EC bonds help in saving capital gains tax?

Section 54EC bonds allow you to invest your capital gains within six months and get an exemption from tax

9. What documents are required to report bond income on tax returns?

You need the bond purchase details, the sale or redemption statement, and the capital gains report or broker statement.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001