Top Alternative Investment Funds (AIFs) In India 2026: Categories, Returns And How To Choose

The Indian investing environment has shifted dramatically in recent years, with more investor engagement and the rising popularity of different investment products.

Along with traditional opportunities, innovative routes such as top alternative investment funds in India have gained prominence in investor portfolios.

The Securities and Exchange Board of India (Alternative Investment Funds) Regulations 2012 were implemented by the Securities Exchange Board of India (SEBI) on May 21, 2012, with the objective of regulating the private fund pool. This blog delves into the Alternative Investment Funds India 2026.

What Are Alternative Investment Funds India 2026?

A privately pooled investment medium that combines the money from both domestic and foreign investors and makes investments in accordance with a specified investment strategy is known as an alternative investment fund. It can be incorporated as a corporation, body corporate, trust, or limited liability partnership in India. An AIF investment involves three parties. Below is an inquiry into each of them.

| Setlor | Establishes the trust which operates as an AIF. |

| Trustee | Manages the pool of funds collected privately. |

| Contributor | Investors who commit capital to the AIF. |

An AIF invests in alternative assets such as commodities, real estate, private equity and hedge funds in India and abroad.

For instance, the table below shows key insights on an AIF called 360 One Asset1.

| Global presence | Spread across countries like India, Singapore, Mauritius, UAE, Canada. It invests in both onshore and offshore assets2. |

| Portfolio | Mutual funds, alternative investment funds, Portfolio Management Services. |

| Target investors | High Networth Individuals (HNIs), Ultra High Networth Individuals (UHNIs), Foreign Institutional Investors (FIIs) |

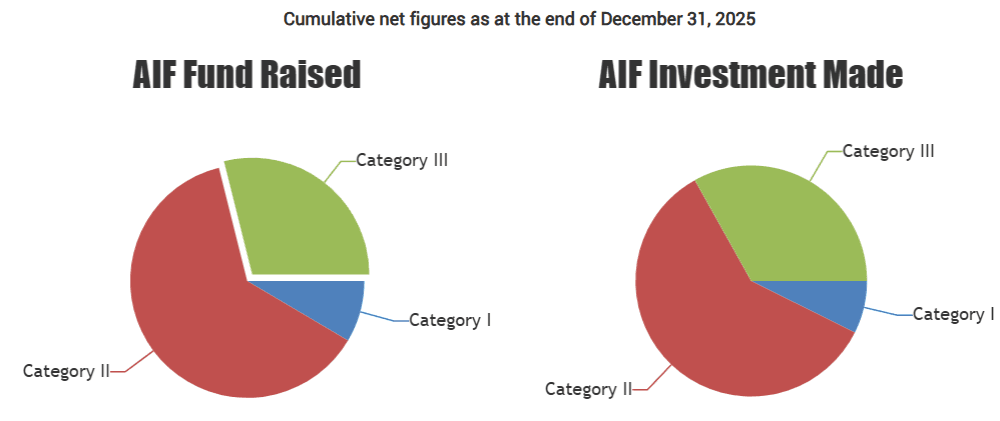

The cumulative investment made and funds raised by the AIF sector across different categories have increased significantly over the years.

As of 31 December 2025, the funds raised by AIF Category I, II, and III in India stood at INR 57,679 crores, INR 424,964 crores, and INR 196,086 crores, respectively. Similarly, the AIF investments made across categories 1,11, and III are INR 47,316 crores, INR 384,169 crores, and INR 213,541 crores, respectively.

The pie charts below illustrate the given mix.

Various factors have contributed to AIF growth in India. A few of the most important factors are covered here.

- Economic Growth: The economic progress of the country in terms of its GDP, per-capita income, etc. are significant contributors to this rising trend.

- Increase in HNIs: Alternative investment platforms are predominantly targeted towards HNIs, UHNIs and FIIs. 2024 reports state that India has the sixth-highest UHNI population in the world4. Moreover, its ranking in Asia in the UHNI population category stands at number three. The rise in HNI and UHNI populations directly impacts the growth of AIFs.

- Regulatory support: Regulators like SEBI and RBI have extended significant support to the AIF ecosystem, aiding the top alternative investment funds in India further. For instance, reports dated 19 May 2025 state the RBI’s proposals to relax investment norms in regulated AIFs5.

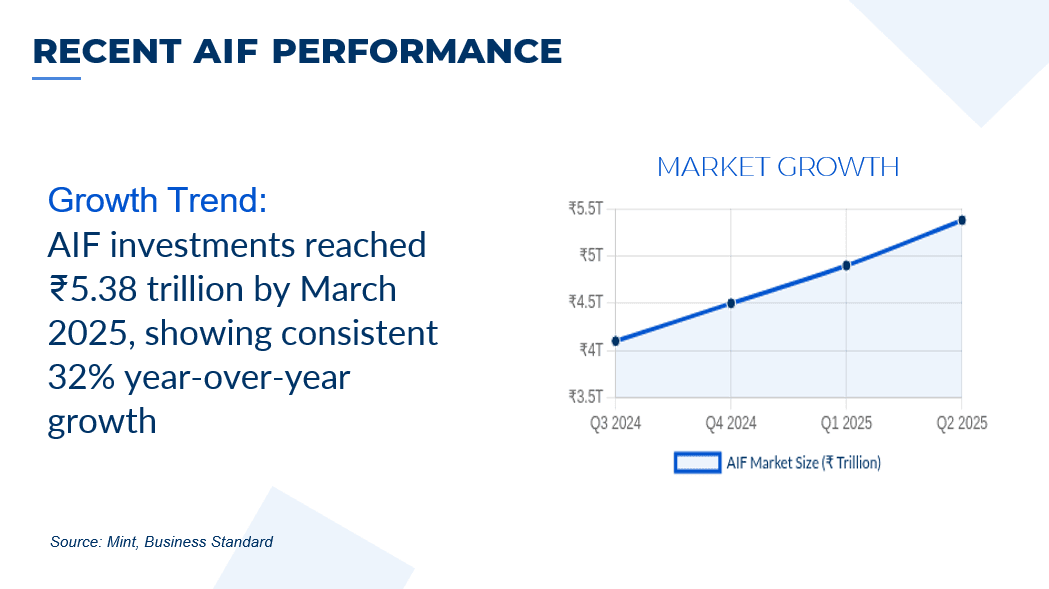

Rising trends of AIFs and their contributing factors impact the performance of the top Alternative Investment Funds in India to a significant extent.

SEBI 2026 AIF Regulatory Update

In addition to the Reserve Bank of India's (RBI) continuous attempts to strike a balance between financial stability and market flexibility with regard to institutional investments, SEBI's initiatives to simplify compliance and reporting define the regulatory environment for Alternative Investment Funds (AIFs) in India in 2026. Discussed below are key points that investors must note.

- AIF minimum investment SEBI: In order to reduce the entrance barriers, the Securities and Exchange Board of India (Alternative Investment Funds) (Amendment) Regulations, 2026 drastically lowered the minimum threshold specified in Regulation 10(c) from INR 2 lakh to INR 1,000. Therefore, AIF investments in Social Impact Funds can start from INR 1,000, instead of INR 2 lakhs.

- Reporting Framework Reform: A new regulatory reporting structure was implemented in March 2026, replacing the earlier, more burdensome quarterly reporting method. AIFs must now file an Annual Activity Report, complemented by a restricted-scope quarterly report.

AIF Category I, II, and III India: Categories Of Alternative Investments In India

Three AIF types must be understood to compare AIFs optimally. Thus, the various AIF classifications are described below to facilitate investor comprehension of these high-return investment funds in India.

- Category I AIFs: These funds make investments in infrastructure, SMEs, start-ups, early-stage businesses, and social projects that are deemed to be economically or socially advantageous. Infrastructure funds, SME funds, and venture capital funds are a few examples of Category I AIFs.

- Category II AIFs: This category covers funds like private equity and debt funds that do not fall under Category I or III. They typically avoid leverage, except for daily operations, and focus on investments in unlisted companies or debt instruments.

- Category III AIFs: These funds use complex trading strategies, including leverage and derivatives, to generate short-term returns. Important examples in this area include hedge funds and some PIPE (Private Investment in Public Equity) funds.

Top Alternative Investment Funds In India (2026)

Multiple Alternative Investment Funds (AIFs) exist today. However, like in the case of any investment medium, certain AIFs perform better than the rest. This section takes a closer look at the top Alternative Investment Funds in India as of 2026.

Overview of Leading AIFs This Year

Despite fluctuating market conditions, the majority of Alternative Investment Funds (AIFs) in India have produced positive returns in 2026, demonstrating their strong performance. 110 out of 123 monitored AIF strategies had gains in April 20256.

The best AIFs in India yielded single-month yields that range from 5 to 9%. Due to robust economic growth and widespread sectoral gains, long-only Category III AIFs fared better than long-short strategies.

The table below lists the top five industries with the most cumulative net investments.

| Sector | Cumulative Net Investment (INR Crores) |

| Real Estate | 69,896 |

| IT/ITes | 34,553 |

| Financial Services | 27,223 |

| NBFCs | 25,564 |

| Banks | 23,793 |

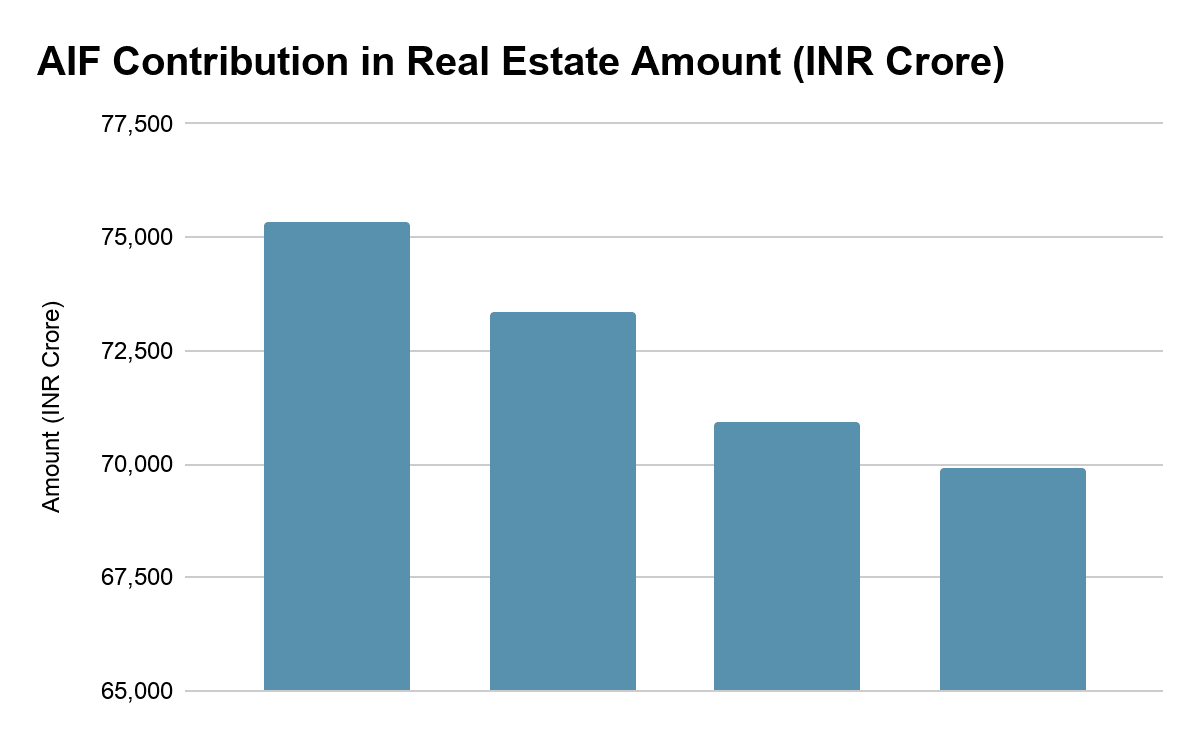

Real Estate AIFs in India

The real estate sector has received the maximum contributions from AIF over the years. The inflows are primarily through Category II AIF contributions and revitalise the opportunities in the Indian real estate sector. The graph below illustrates the growth in AIF contributions in real estate over different tenures.

While traditional methods of real estate financing continue to face constraints, this emerging trend of real estate financing through AIFs not only creates opportunities for AIF investors but also eases financing sources for the real estate sector.

AIF Returns India: Choosing AIFs Based on Returns

The primary objective of any investment is to earn sufficient gains, provided the degree of risk taken. Therefore, the historic risk metrics can serve as key parameters to shortlist AIF investments. The table below lists the top five AIF investments based on their one-year CAGR, as of 31 March 2026.

| AIF | One-Year Return (%) | Return Since Inception (%) |

| Sundaram Alternate Assets Ltd.- Opportunities Series | 22.07 | 18.22 |

| Abakkus Asset Managers Pvt Ltd.- Growth Fund 1 | 13.22% | 17.21% |

| Pluswealth Capital Management LLP- Plus Wealth Assets LLP | 12.44% | 15.46% |

| Neo Asset Management Pvt Ltd- Treasury Plus Fund | 12.00% | 13.15% |

| Whitespace Alpha- Whitespace Fund II- Debt Plus | 11.31% | 13.32% |

Other Factors to Choose AIF

The top-performing alternative funds in India are the flag bearers of the growth trends discussed above. However, selecting the top Alternative Investment Funds in India requires analysis of certain key parameters. These parameters are discussed below.

1. Risk: The cost of return is a risk. Investors have to bear the risk burden to derive returns. Nonetheless, the risk needs to align with the investor's risk profile. Investors can compare the returns delivered by AIFs with market indices like Nifty 50, BSE 500 over a specific period to gauge the degree of risk. Moreover, the disclosures made by the AIF about parameters like portfolio holdings, performance updates, etc., can provide important insights.

2. Track record: Track record is the term used to describe the past performance of AIF funds and their managers over time. Parameters like experience, knowledge, and prior success are evaluated by rating agencies and investors as indicators of potential performance.

3. Lock-in Period and Liquidity Risks: Category I and II AIFs are usually close-ended and have a minimum tenure of three years. On the other hand, Category III AIFs can be both open and closed-ended. Exploring the fund documents to understand liquidity helps plan the timeframe for AIF investments efficiently and avoid future cash flow crunches

How To Compare AIFs ?

There are various Alternative Investment Funds in India. For instance, the Real Estate AIFs in India have got significant traction because real estate tops the list of sectorwise cumulative net investments.

Therefore, choosing the best AIFs in India requires optimal comparison of different parameters. Some of these parameters are discussed below.

Investors must identify the category of funds they wish to invest in. Comparison of key metrics like AIF returns within a particular category is important to ensure optimum portfolio diversification.

Standard performance metrics like annualised returns, internal rate of return, etc., can help gauge the return of the top-performing alternative funds. Some key metrics are discussed in the table below.

| Distribution to Paid in Capital (DPI) | Calculates the amount of money that investors have received back compared to their initial investment. |

| Residual Value to Paid in Capital (RVPI) | Shows how much of the outstanding investments have not yet been realised. |

| Total Value to Paid in Capital (TVPI) | Shows the overall value generated (realised + unrealised) compared to invested capital by combining the DPI and RVPI. |

For instance, if DPI is 10 and RVPI is 12, then TVPI will be 10 + 12 = 22.

1. Benchmark: Comparing the performance of AIFs with various benchmarks and indices typical to specific categories can help optimum portfolio diversification. Crisil AIF benchmarks and Nifty AIF benchmarks provide data across categories.

For instance, in FY2024, the benchmark TVPI of Category I stood at 1.19.

2. Qualitative analysis: Analysing the past performance of fund managers, including their experience, educational background, etc, can also aid decision making.

3. Expenses: Fund managers charge management fees and other fees for investing in an AIF. These parameters add to the cost of investment and are thus crucial for optimum investing.

Categories Of Alternative Investments In India

Optimum comparison of AIFs requires an understanding of three AIF categories. Therefore, to ease investor understanding of the high-return investment funds in India, listed below are the different AIF categories.

1. Category I AIFs:

These funds invest in start-ups, early-stage ventures, SMEs, infrastructure, and social ventures that are considered socially or economically beneficial. Examples include venture capital funds, SME funds, and infrastructure funds.

2. Category II AIFs:

This category covers funds like private equity and debt funds that do not fall under Category I or III. They typically avoid leverage, except for daily operations, and focus on investments in unlisted companies or debt instruments.

3. Category III AIFs:

These funds use complex trading strategies, including leverage and derivatives, to generate short-term returns. Hedge funds and certain PIPE (Private Investment in Public Equity) funds are key examples in this category

Choosing The Right Alternative Investment Funds

The success of an investment depends on choosing the right investment medium. However, the process of selecting the right medium is based not only on the characteristics of the assets in question but also on individual investor characteristics.

1. Assessing Risk Appetite and Investment Goals

Investors must consider their risk profile before investing. If the risk of an asset is beyond the risk-bearing capacity, the investor may face capital depreciation of their asset portfolio. The risk metrics of an investment might be in tandem with the risk-bearing capacity. Moreover, fiscal goals are also a key influencer. For instance, a risk-averse investor might find equity funds undesirable.

2. Evaluating Fund Manager Track Record

The top Alternative Investment Funds in India employ highly experienced and skilled fund managers to manage the AIF portfolio. Optimum evaluation of an AIF involves understanding the team of fund managers and their track records. In this case, the word track record refers to the performance of funds managed by these experts.

3. Understanding Fee Structures and Minimum Investment

SEBI AIF regulations stipulate that individual investors must invest at least INR 1 crore8. Moreover, there are various fees associated with the AIF investment, such as management fees, performance fees and so on. It is similar to the fees involved in mutual funds. These fees act as a cost to investment and must be considered for optimum investment.

4. Regulatory Compliance and Transparency

AIF due diligence incorporates an array of regulatory compliance aimed at promoting transparency. Since AIFs are targeted predominantly towards HNIs, UHNIs and FIIs, regulatory compliance is necessary to avoid illegal transactions like money laundering. For instance, the number of investors of an AIF cannot be more than 1000, other than angel investors. Ensuring strict adherence to these frameworks must be ensured by any AIF9.

Step-by-step Guide On How To Evaluate And Invest In An AIF

Discussed below are milestones that can help HNI investors select an AIF that suits their investment needs and goals.

Step 1: Assessing Risk Appetite and Investment Goals

Before investing, investors must think about their individual risk tolerance. An investor may experience capital depreciation of their asset portfolio if an asset's risk exceeds their risk-bearing capability. The risk metrics of an investment might be in tandem with the risk-bearing capacity. Moreover, fiscal goals are also a key influencer. For instance, a risk-averse investor might find equity funds undesirable.

Step 2: Assessing the return and risk profile of AIF

Based on their historic returns, an investor can shortlist the AIFs. Using screeners or individual AIF documents, an investor can create a list of possible AIF investments, using their annualised return or other historic yield parameters.

Step 3: Understanding Fee Structures and Minimum Investment

Investors should analyse the minimum investment required in their AIF. Moreover, there are various fees associated with the AIF investment, such as management fees, performance fees and so on. It is similar to the fees involved in mutual funds. These fees act as a cost to investment and must be considered for optimum investment.

Step 4: Evaluating Fund Manager Track Record

To manage the AIF portfolio, the Alternative Investment Funds in India use highly qualified and experienced fund managers. Understanding the group of fund managers and their performance history is essential for the most effective assessment of an AIF. The performance of the funds overseen by these professionals is referred to here as the “track record.”

Step 5: Assessing AIF Tax Treatment in India to Gauge Real Returns

The amount of taxation reduces the real rel returns anticipated from an investment medium. In the case of AIFs, Category I and II AIFs are taxed in the hands of the investor. In this case, AIFs can withhold tax on income credited to resident investors at 10%. For Category III AIFs, there is no specific tax regime. Therefore, in this case, taxability depends on the legal structure of the AIF, that is, LLP, trust, company, etc.

AIF vs PMS vs Mutual Fund

The table below compares Alternative Investment Funds with Portfolio Management Services and Mutual Funds.

| Particulars | AIF | PMS | Mutual Fund |

| Basic structure | A pooled vehicle that allows rich individuals, like HNIs, to invest in listed, unlisted securities, real estate, PE/VC, and other investments based on Category I, II, and III. | Investors obtain a separate demat account in their name, and the portfolio manager constructs and trades a portfolio directly on their behalf. | Investors indirectly hold a mix of securities through units in a pooled structure where several investors possess units of a single scheme. |

| Investor type | HNIs and experienced investors | HNIs and UHNIs | Retail, small ticket investors and beginners |

| Customisation of the scheme | Schemes are usually strategy-driven | Highly customisable schemes | Standardised schemes |

| Liquidity | Low to medium | Medium to low | High |

Conclusion

Alternative Investment Funds were brought under the regulatory jurisdiction of SEBI in 2012. These are privately pooled funds targeted towards HNIs, UHNIs and FIIs. Presently, the investment landscape is witnessing a significant increase in AIF popularity. This trend is influenced by several factors, such as increased HNI population and economic prosperity.

However, investment in the top Alternative Investment Funds in India requires a thorough analysis of their risk, return, benchmark comparisons and much more. Moreover, regulatory compliance is also necessary for successful investing.

Optimum portfolio diversification requires a fine blend of traditional and modern investment avenues. Grip Invest offers you a range of rated fiscal instruments that can offer up to 14% returns!

Join Grip’s 4 Lakh+ community today!

FAQs on Top AIFs In India

1. Is AIF better than mutual funds?

AIFs and mutual funds meet distinct investor demands. AIFs provide accessibility to unique assets and possibly better returns, but they need more capital, carry more risk, and have less liquidity.

Mutual funds are more accessible, regulated, and liquid. So they are suited for most investors seeking higher stability and flexibility.

2. What are the benefits of AIF?

AIFs have substantial advantages, including access to a variety of asset classes such as private equity, real estate, and hedge funds, which are sometimes inaccessible through standard investment vehicles.

They provide portfolio diversity, the possibility for better returns, and exposure to innovative methods, making them appealing to investors seeking growth and risk management.

3. Is AIF tax-free?

All income earned by Category I and II AIFs will be subject to 12.5% capital gains tax. The same revenue would be subject to 30% tax for residents and up to 39% tax for non-residents if it were classified as business income.

Therefore, both category I and II AIFs have acquired the pass-through status, which means that they are taxable in the hands of the investor. However, Category III AIFs have not acquired pass-through status and the taxes are borne by the fund. This implies that the dividend earned by the investor is tax-free.

4. What is the minimum investment required to invest in an AIF in India?

To invest in an Alternative Investment Fund (AIF) in India, the Securities and Exchange Board of India (SEBI) mandates a minimum investment of INR 1 crore for individual investors. For employees, directors, or fund managers of the AIF, the minimum is INR 25 lakh. The only exception is for angel funds, where the minimum investment is INR 25 lakh. This high threshold ensures that AIFs remain accessible mainly to high-net-worth and sophisticated investors.

5. Who is allowed to invest in alternative investment funds in India?

Alternative Investment Funds (AIFs) in India are open to a range of sophisticated investors: Resident Indians, NRIs, and foreign nationals are all eligible to invest.

AIFs are designed primarily for high-net-worth individuals and institutional investors who can accept higher risks and longer lock-in periods.

AIFs are not intended for small retail investors, ensuring participation is limited to those with the financial capacity and risk appetite for such investments.

6. How many AIFs are there in India?

As of July 2025, India has over 1,600 registered Alternative Investment Funds (AIFs), according to data from the Securities and Exchange Board of India (SEBI). This number reflects rapid growth in the AIF sector, driven by increasing interest from high-net-worth individuals and institutional investors seeking diversification beyond traditional assets. The AIF landscape continues to expand, offering a wide range of investment strategies and asset classes.

References:

1. Securities and Exchange Board Of India, accessed from: https://www.sebi.gov.in/sebiweb/other/OtherAction.do?doRecognisedFpi=yes&intmId=16

2. 360 One, accessed from: https://www.360.one/asset-management/disclosures/

3. Securities and Exchange Board Of India, accessed from: https://www.sebi.gov.in/statistics/1392982252002.html

4. The Hindu, accessed from: https://www.thehindu.com/real-estate/the-rise-of-indian-hnis-and-uhnis-in-2024/article69022791.ece

5. The Economics Times, accessed from: https://economictimes.indiatimes.com/news/economy/policy/rbi-proposes-relaxing-rules-for-investments-in-aifs/articleshow/121269381.cms?from=mdr

6. PMSBazaar, accessed from: https://pmsbazaar.com/Blogs/110-of-123-AIFs-Deliver-Gains-in-April--Top-Performers-Log-5%E2%80%939percentage-Returns

7. Money Control, accessed from: https://www.moneycontrol.com/news/business/markets/top-10-aif-performance-for-the-month-of-april-2025-13027174.html

8. CNBCTV18, accessed from: https://www.cnbctv18.com/alternative-investment-fund/aif-investment-how-much-corpus-do-you-really-need-19564077.htm

9. Securities and Exchange Board Of India, accessed from: https://www.sebi.gov.in/sebi_data/attachdocs/1471519155273.pdf

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001