Callable Bonds: Risks, Taxation, And How They Work

A bond is usually a fixed-income instrument that provides investors with predictable returns at regular intervals. This stability against market volatility makes bonds attractive to many investors. However, callable bonds differ from traditional bonds. In this case, the issuer has the right to redeem the bond before its maturity date, which increases uncertainty for investors.

To make up for this added risk, callable bonds generally offer higher interest rates. For investors aiming to diversify their portfolios, understanding how callable bonds work is crucial to balancing the potential for higher returns with the risk of early redemption.

In the following sections, we will break down callable bonds in detail, covering how they work, their advantages, and the risks you should watch out for.

Callable Bonds: What Are They?

A callable bond allows the issuer to redeem the bond before maturity, usually after an initial call-protection period. The terms appear in the offer document when the bond is issued.

When exercising the option, the issuer pays the specified call price and any interest due under the bond terms. The call price may equal the face value or include an additional call premium.

Companies usually consider early redemption when market interest rates fall. They can repay a higher-cost bond and raise fresh debt at a lower rate.

For example, suppose a company issues a callable bond carrying an 8% annual coupon. If comparable borrowing rates later fall to 6%, the issuer may redeem the 8% bond and refinance at the lower rate.

The company reduces its borrowing cost. However, the investor loses the remaining 8% coupon payments and may only find new bonds offering around 6%.

The structure has appeared in both government and corporate debt in India. The RBI states that the 6.72% Government Security 2012, issued on 18 July 2002, was India’s first government security containing both call and put options. The options became exercisable after five years on subsequent coupon dates.

Key Terms to Know Before Investing In Callable Bonds

Investors need to understand more than the headline coupon. The following terms determine how long the investment may continue and what the investor could receive.

Term | Meaning |

Face value | The principal amount assigned to each bond |

Coupon rate | The annual interest calculated on the face value |

Maturity date | The final date for principal repayment if the bond is not called |

Call date | The date from which or on which the issuer can redeem the bond |

Call price | The amount paid when the issuer calls the bond |

Call premium | An amount paid above face value on early redemption |

Call protection period | The initial period when the issuer cannot exercise the call option |

Call notice | Advance communication issued before redemption |

Yield to maturity | The estimated annual return if the bond continues until maturity |

Yield to call | The estimated annual return if redemption occurs on a call date |

Yield to worst | The lowest calculated yield across possible call dates and maturity |

Reinvestment risk | The risk of reinvesting early redemption proceeds at lower rates |

Together, these terms show that the stated maturity may not be the investor’s actual holding period. The call date and call price can have a greater impact on returns when early redemption is likely.

Consider this callable bond example, REC Limited’s Series 211 bonds carried a 6.23% annual coupon and an INR 10 lakh face value. Although the final maturity was 31 October 2031, the issuer could exercise the call option on 31 October 2026 at the face value, subject to at least 21 days’ notice.

This example shows why investors should assess the return up to the call date, rather than relying only on the final maturity date. The issue details are used only to explain the structure and do not represent an investment recommendation.

How Do Callable Bonds Work?

Understanding how callable bonds work requires tracking the bond from issuance to either its call date or final maturity.

1. The issuer raises funds

A company, financial institution or government entity issues bonds to borrow money. The offer document states the coupon, maturity, call schedule and redemption price.

2. The investor receives coupons

The issuer pays interest according to the agreed frequency. These payments continue unless the issuer defaults or exercises the call option.

3. The call-protection period ends

The issuer cannot normally call the bond during the protected period. Once it ends, the issuer can assess whether early repayment makes financial sense.

4. The issuer compares refinancing costs

A call becomes more likely when prevailing borrowing rates are below the existing bond’s coupon. However, lower rates do not guarantee redemption.

The issuer must also consider the call price, refinancing expenses, regulatory requirements and available liquidity.

5. The issuer sends a call notice

If it decides to proceed, the issuer follows the notice process stated in the offer document. Investors cannot reject a valid call made under those terms.

6. Investors receive the redemption proceeds

The issuer pays the call price and applicable accrued interest. Future coupons stop after redemption.

For example onsider an investor who purchases the following bond at face value:

Bond feature | Details |

Investment | INR 10,000 |

Annual coupon | 8% |

Annual interest | INR 800 |

Final maturity | 10 years |

Earliest call date | End of year five |

Call price | INR 10,000 |

If the issuer does not call the bond, the investor receives INR 8,000 as total coupon income over 10 years. The issuer also repays the INR 10,000 principal at maturity.

If the bond is called after five years, the investor receives only INR 4,000 in coupons before getting the INR 10,000 principal back.

Assume the investor then reinvests that principal for the remaining five years at 6%. The new investment generates INR 3,000, taking total 10-year interest to INR 7,000.

Outcome | First five-year interest | Next five-year interest | Total interest over 10 years |

Bond continues at 8% | INR 4,000 | INR 4,000 | INR 8,000 |

Bond called and reinvested at 6% | INR 4,000 | INR 3,000 | INR 7,000 |

The early call reduces interest income by INR 1,000 in this simplified example. Actual callable bonds’ returns will also depend on purchase price, call premium, reinvestment rate and taxes.

How Is A Callable Bond Valued?

A regular bond is valued by calculating the present value of its future coupon and principal payments. A callable bond is more complex because the issuer may end these payments before maturity.

Investors should therefore compare two possible outcomes:

- The return if the bond continues until maturity

- The return if the issuer redeems it on the call date

Yield to maturity estimates the return if the bond remains outstanding until its final maturity. Yield to call estimates the return if the issuer exercises the call option on a specified date.

Consider the earlier INR 10,000 bond carrying an 8% annual coupon. Using a comparable market yield of 6% as the discount rate, its estimated value under each scenario is:

Valuation scenario | Estimated present value |

Bond is called after five years | INR 10,842 |

Bond continues until year 10 | INR 11,472 |

The second value is higher because the investor would continue receiving the 8% coupon for another five years.

However, if investors expect the issuer to exercise the call option, the bond’s price may be influenced more by the five-year cash flows. This limits the price appreciation available from falling interest rates.

The relationship can also be expressed as:

Callable bond value = Value of a comparable non-callable bond - Value of the issuer’s call option

The call option benefits the issuer. Therefore, an otherwise similar callable bond will generally be worth less than a non-callable bond.

Returns And Risks Of Callable Bonds

Callable bonds are attractive investments but come with certain risks. The issuer can always choose to pay them back early. This can affect your earnings.

Returns:

- As compensation for the issuer's call option, callable bonds typically pay higher yields than non-callable ones.

- If interest rates fall in the market and the bond is not called right away, its market value can increase.

Risks:

- The issuer may pay back your bond early, stopping your interest payments. You might have to invest your money again at lower interest rates.

- Once the bond reaches its call price, you can not make much extra profit from price increases.

Difference Between Callable Bonds And Non-Callable Bonds

Here are the key differences between Callable vs. Non-Callable Bonds:

Feature | Callable Bonds | Non-Callable Bonds |

Early Redemption Option | The issuer can redeem before maturity | It is held until maturity unless sold in the market |

Coupon Rate | Generally higher to compensate for call risk | Generally lower |

Risk of Losing Future Income | High, due to the call feature. | Low |

Capital Gains Potential | Limited after the call price is reached | Higher if rates fall significantly |

Investor Protection | It is lower as the issuer holds an advantage. | It is higher due to predictable income streams |

Taxation On Callable Bonds In India

Tax treatment depends on whether the investor earns coupon interest, sells the bond or receives repayment when the issuer exercises the call option.

The table below provides a broad overview for resident individual investors under rules applicable from 23 July 2024.

Income or event | Broad tax treatment |

Coupon interest | Generally taxed at the investor’s applicable income-tax rate |

Listed bond held for 12 months or less | Gain generally treated as short-term and taxed at the applicable rate |

Listed bond held for more than 12 months | Gain generally treated as long-term and taxed at 12.5% without indexation |

Unlisted bond sold, redeemed or matured | Gain treated as short-term regardless of the holding period |

TDS on interest on securities | Generally deducted at 10%, subject to applicable provisions and exemptions |

Source: Income Tax India

Coupon interest is generally reported under “Income from Other Sources” unless the investor holds the bonds as part of a business.

When an issuer calls a bond, the difference between the redemption amount and the eligible purchase cost may result in a capital gain. Its tax treatment depends mainly on whether the bond is listed or unlisted.

TDS is only an advance tax deduction. Investors may claim credit for it while filing their income-tax return, subject to the applicable rules.

How Interest Rates Affect Your Investment Returns

Callable bonds have a strong relationship with the movement of interest rates. When rates decline, issuers tend to call the bond and take new financing at lower rates. When rates increase, these bonds act similarly to ordinary bonds, except their prices will not appreciate as much because of the built-in call option.

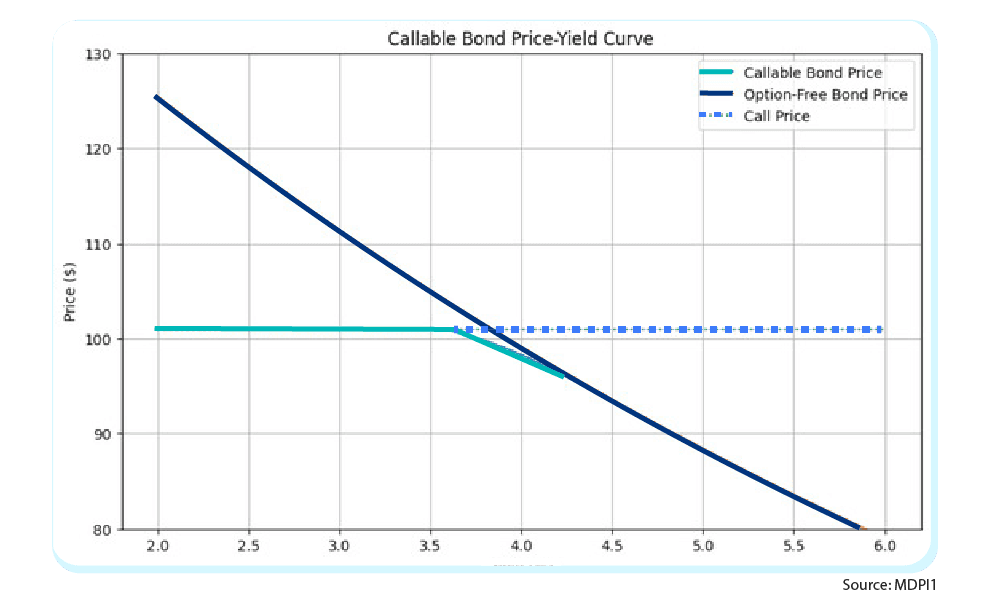

Source: MDPI1

This callable bond graph compares two bonds that are the same in every way. Both last 15 years have a face value of INR 100, and pay 4% interest every year. The only difference is that one is callable, meaning the issuer can buy it back early for INR 101, but only within the first 5 years. The chart shows how their prices change with interest rates, assuming a 2% volatility and a 4% risk-free rate.

Who Should Consider Callable Bonds?

Callable bonds are best used by investors who are aware of the trade-off between higher returns and the risk of early call. Although they can enhance value in a diversified portfolio, they need a certain appetite for risk as well as sensitivity to interest rate trends.

Suitable Investor Profiles

- Investors who want higher coupon payouts, in contrast to regular bonds or fixed deposits.

- Investors who are already familiar with the workings of the bond market can assess call schedules, yield-to-call, and reinvestment opportunities.

- Investors who expect interest rates to stay steady so the bond is less likely to have the bond paid back early.

Long-Term Vs Short-Term Use Case

- Long-Term Use: This is for investors who will settle for locking in greater yields for as long a period as possible and are aware that the bond may be redeemed earlier. Best in times when interest rates are firm or likely to increase.

- Short-Term Use: These bonds, bought for holding until the call date, can represent a high-yield bond substitute for short-term deposits. This holds if the call date coincides with individual cash flow demands.

Tips Before You Invest In Callable Bonds

Although callable bonds have high-yielding potential, their distinctive nature requires additional caution. When considering adding them to your investment portfolio.

Here are some points to remember:

1. Read The Call Schedule

Look out for when the issuer can redeem the bond initially (call protection period) and at regular intervals subsequently. This will give you an idea of how long your higher coupon rate may be for.

2. Compare Yield-To-Call Vs Yield-To-Maturity

Do not focus only on the yield-to-maturity (YTM). The yield-to-call (YTC) usually presents a more realistic picture of returns if the bond is called early.

3. Look At The Interest Rate Forecast

When callable bond interest rates are predicted to decline, the chances of early redemption rise. Rising or flat rates can be in your favour by decreasing call risk.

Conclusion

Callable bonds can be a strong addition to a fixed-income portfolio, often offering more potential than traditional investments. The real challenge, however, lies in predicting how long these higher returns will last, especially when interest rates start to decline. For Indian investors, success depends on carefully weighing factors such as interest rate trends, call schedules, and reinvestment options.

If you are exploring ways to diversify your fixed-income portfolio and want to see how callable bonds fit into the bigger picture of smart debt investing in 2025, there’s one platform you shouldn’t miss.

Log in to Grip Invest to discover expertly analyzed callable bonds and other high-quality fixed-income opportunities that can help you balance risk and returns while building a resilient portfolio.

FAQs On Callable Bonds

References:

1. MDPI, accessed from: https://www.mdpi.com/2227-9091/13/4/69

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks, including delay and/ or default in payment. Read all the offer-related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for the consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001