Profectus Capital: Empowering India’s MSMEs With Customized And Secured Financing Solutions

Introduction To Profectus Capital Pvt. Ltd.

Profectus Capital Pvt. Ltd. (PCPL) is a systemically important Non-Banking Financial Company (NBFC) that focuses on secured lending to Micro, Small and Medium Enterprises (MSMEs) in India. Backed by global private equity firm Actis, the company provides financing solutions across key segments such as enterprise mortgage, school loans, equipment finance, and supply chain finance.

With a strong focus on empowering small businesses, Profectus Capital offers tailored loan products designed to help entrepreneurs expand operations, upgrade technology, and manage working capital efficiently.

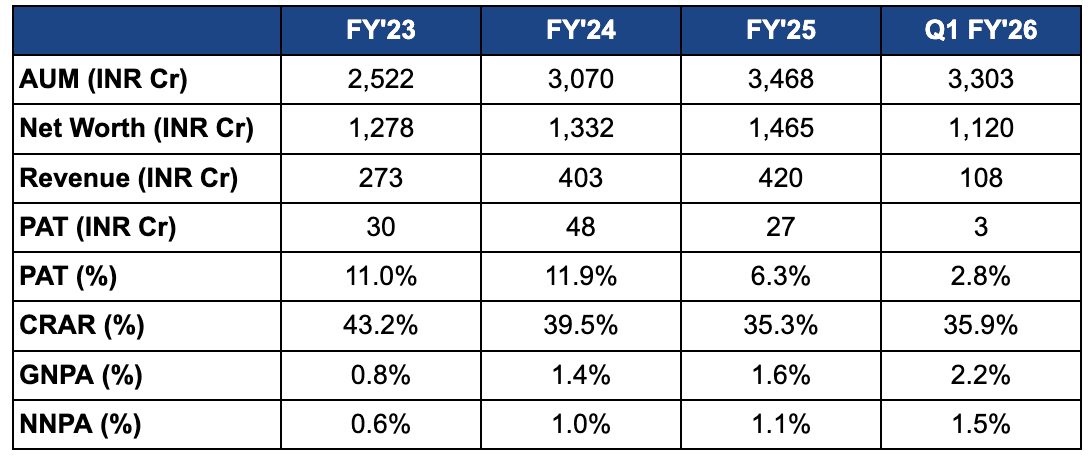

As of June 2025, Profectus Capital has built an Asset Under Management (AUM) of INR 3,303 crore and operates through 29 branches across 15 states. The company maintains a Capital Adequacy Ratio (CAR) of 35.9%, reflecting its strong financial health and conservative risk management practices.

Now set to be acquired by UGRO Capital, this strategic move is expected to add approximately INR 150 crore in annualized profit and further strengthen UGRO’s presence in secured and machinery finance. With its disciplined governance, diverse portfolio, and expanding footprint, Profectus Capital continues to play a vital role in bridging the credit gap for India’s growing MSME sector.

Board Of Directors Of Profectus Capital Pvt. Ltd.

Here is the list of Board of Directors of Profectus Capital Pvt. Ltd. along with their designations:

- Mr. KV Srinivasan — Executive Director & Chief Executive Officer

- Mr. Asanka Rodrigo — Non-Executive Director

- Mr. Pratik Jain — Non-Executive Director

- Mr. Hossameldin Aboumoussa — Non-Executive Director

- Mr. Sudarshan Sampathkumar — Independent Director

Source: Profectus Capital Pvt. Ltd.1

Products Offered By Profectus Capital Pvt. Ltd.

1. Secured Term Loans / Enterprise Mortgage Loans

PCPL provides term loans secured by property (enterprise mortgage) to MSMEs that need funds for expansion, infrastructure upgrades, new site acquisition or working capital support. The property collateral (industrial / commercial) is used as security, and the underwriting uses a mix of cash-flow assessment and asset value. According to their website the product covers: business expansion, purchase of new property, infrastructure upgrades, plot + construction loan, zero-day LAP (loan against property where borrowing can go beyond agreement value).

Key features: flexible repayment, industry-specific underwriting, collateral options including industrial/commercial plots, eligibility typically for businesses with at least three years of vintage.

This product enables entrepreneurs to leverage their real estate or business assets to get growth capital rather than rely purely on unsecured credit.

2. Machinery & Equipment Finance

PCPL offers financing for purchase of machinery, equipment and tools across both manufacturing and service sectors. Examples listed include CNC machines, VMC machines, injection moulding, blow moulding, offset printing machines, medical diagnostic and surgical equipment.

Features include: high LTV (loan to value) for new machinery, in some cases older/used equipment (for certain sectors like printing & healthcare) allowed, no secondary collateral in some cases, flexible tenure (up to about 4 years mentioned) and cash-flow based underwriting.

This product is aimed at MSMEs that want to upgrade operational capacity, modernize technology, remain competitive or expand production.

3. Working Capital / Supply Chain Finance

PCPL provides working capital term loans and supply chain finance (SCF) products to improve cash-flow, free up capital tied in receivables/inventory, and help manage supplier or distributor relationships. Their SCF product includes distributor financing, vendor finance/bill discounting, merchant cash advance.

Key benefits listed: Faster payments to suppliers, improved liquidity, better procurement/inventory management, flexible financing options such as revolving credit, bill discounting or merchant advances.

This product is especially useful for MSMEs with high turnover, receivables or supply-chain obligations who want to optimize working capital rather than invest purely in fixed assets.

4. School / Education Infrastructure Financing

PCPL offers loans tailored to the K-12 school segment for infrastructure expansion, technology upgrades, new facilities (lab/classrooms), and sometimes sustainable upgrades (like solar installations) for school properties.

Features include: loan amounts from roughly INR 25 lakh up to INR 5 crore, repayment tenures between 2 to 7 years, flexible collateral options (school property or individual residential/commercial property), approvals within 3-7 working days in some cases, and supporting schools in both metros and non-metros.

This product addresses the financing gap for private schools which need to expand or modernize but may lack large traditional bank financing options.

5. Rooftop Solar / Green Energy Finance

PCPL also offers financing for solar panel installations and renewable energy setups, especially for MSMEs, schools, hospitals and commercial entities. The idea is to reduce energy costs and drive sustainability while backing the asset with financing.

Highlights include financing up to about INR 3 crore for solar energy needs, collaterals waived for certain amounts (up to INR 1 crore), flexible repayment up to 4 years, large capacity from 15 kW to 100 MW.

This product shows PCPL’s focus beyond pure manufacturing/service lending into modern, future-oriented infrastructure finance.

6. NBFC/Onward Lending / Structured Finance

PCPL lends to other NBFCs (non-banking financial companies) to help them expand their portfolios, engage in pool purchases or structured finance arrangements.

This product is aimed at the financial-institution side rather than direct MSME customers: providing term loans or structured offerings to NBFCs for onward lending, improving liquidity or balance sheet strength.

Source: Profectus Capital Pvt. Ltd.2

Profectus Capital Pvt. Ltd. Customer Care

For any queries or support, Profectus Capital’s customer care team is here to help. You can reach them at 022-4919-4400 or email : customercare@profectuscapital.com.

Customized And Secured MSME Financing Solutions By Profectus Capital

Profectus Capital Pvt. Ltd. stands out in India’s lending landscape for its specialized approach to MSME financing. The company focuses on providing customized and secured loans that cater to the specific needs of micro, small, and medium enterprises across diverse sectors. Unlike traditional lenders, Profectus Capital designs its loan solutions based on each business’s cash flow, operational model, and growth potential, ensuring flexibility and affordability for borrowers.

Its products cover a wide range of MSME requirements — from enterprise mortgage loans and equipment financing to school infrastructure loans and supply chain finance. Each product is backed by sound underwriting practices and collateral-based security, giving both the borrower and the lender confidence in sustainable growth.

With a strong presence across multiple Indian states and deep understanding of regional industries, Profectus Capital helps small businesses access funds quickly and transparently. This personalized, secured, and growth-oriented approach makes it a trusted financial partner for MSMEs looking to expand operations, modernize facilities, or improve cash flow management.

Key Strengths Of Profectus Capital Pvt. Ltd.

Following are the key strengths of Profectus Capital Pvt. Ltd.

1. Strategic Acquisition by UGRO Capital

Profectus Capital is being acquired by UGRO Capital for INR 1,400 crore. After this deal, it will become a wholly owned subsidiary of UGRO. This acquisition is expected to strengthen UGRO’s position in secured and machinery finance while giving Profectus Capital access to a wider customer base, better technology, and more funding support for future growth.

2. Diversified MSME-Focused Portfolio

The company has a well-balanced loan portfolio that focuses on different segments of the MSME sector. Its lending book includes enterprise mortgage (38%), school funding (25%), equipment finance (18%), and supply chain finance (10%). This diversification helps reduce risk by ensuring that no single sector dominates its business. As a result, Profectus Capital maintains steady performance even if one industry faces challenges.

3. Robust Capital Position

Profectus Capital maintains a Capital Adequacy Ratio (CAR) of 35.9% and a low leverage ratio of 1.84x. These numbers show that the company has a strong financial foundation and enough capital to manage risks and fund its expansion. Such a healthy capital position gives it flexibility to grow while maintaining stability.

4. Healthy Asset Quality

The company has kept its loan book strong and secure, with Gross Non-Performing Assets (GNPA) at 1.6% and Net Non-Performing Assets (NNPA) at 1.1%. These low levels highlight its disciplined lending practices and focus on secured loans, which help protect both the company and its investors from credit losses.

Financial Snapshot Profectus Capital Pvt. Ltd.

Source: Source: audited financials, credit rating reports

To arrange the capital, Profectus Capital Pvt. Ltd. also offers corporate bonds. These opportunities from the company are secured and are rated by credit rating agencies. On Grip Invest, investors invested in CARE ‘A’ rated bonds of the company that offered fixed returns of up to 10%. To invest in similar, rated, regulated and secured fixed-income opportunities sign-up for Grip Invest today and start earning fixed returns:

References:

1. Profectus Capital Pvt. Ltd., accessed from: https://tinyurl.com/9s454duf

2. Profectus Capital Pvt. Ltd., accessed from: https://www.profectuscapital.com/

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks, including delay and/ or default in payment. Read all the offer-related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for the consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001