Household Debt in India: Key Trends, Risks, and Smart Management Tips

The Indian economy is one of the fastest-growing major economies in the world. Given the massive size of the population and the GDP surpassing the $4 trillion mark recently, it is rather astonishing that the growth rate for Q1 FY26 (first quarter of 2025-26) was 7.8%1. However, along with the increased household expenditure, another critical factor that should be considered is the level of household debt.

Household debt refers to the total amount of money that individuals and families owe to lenders, including banks, housing finance companies, and credit card issuers. It impacts the net worth of households as people take loans to cover large expenses such as housing, education, vehicles, personal expenses, and outstanding credit balances.

With digitalisation and improved banking and financial processes, availing loans has become easier. Loans help families attain their aspirations and lifestyle changes; however, huge debt can also drastically affect personal financial planning.

Let us explore the trends, risks, and how household debt impacts your finances and long-term financial planning.

Current Trends In Household Debt

With the changing lifestyles, increase in urbal population, and ease of availability (of credit), the country is witnessing a constant rise in the household borrowing trends. Even though the levels of debt have been rising consistently in the past couple of years, there has been a massive rise in personal and other loans undertaken by individuals in the past two years. As per a report, the average household debt in India has increased by 23% in the past two years2.

Still, major financial institutions suggest that the numbers are not worrisome right now. The average household debt in India is close to 42% which is significantly lower than the average debt in other emerging economies3.

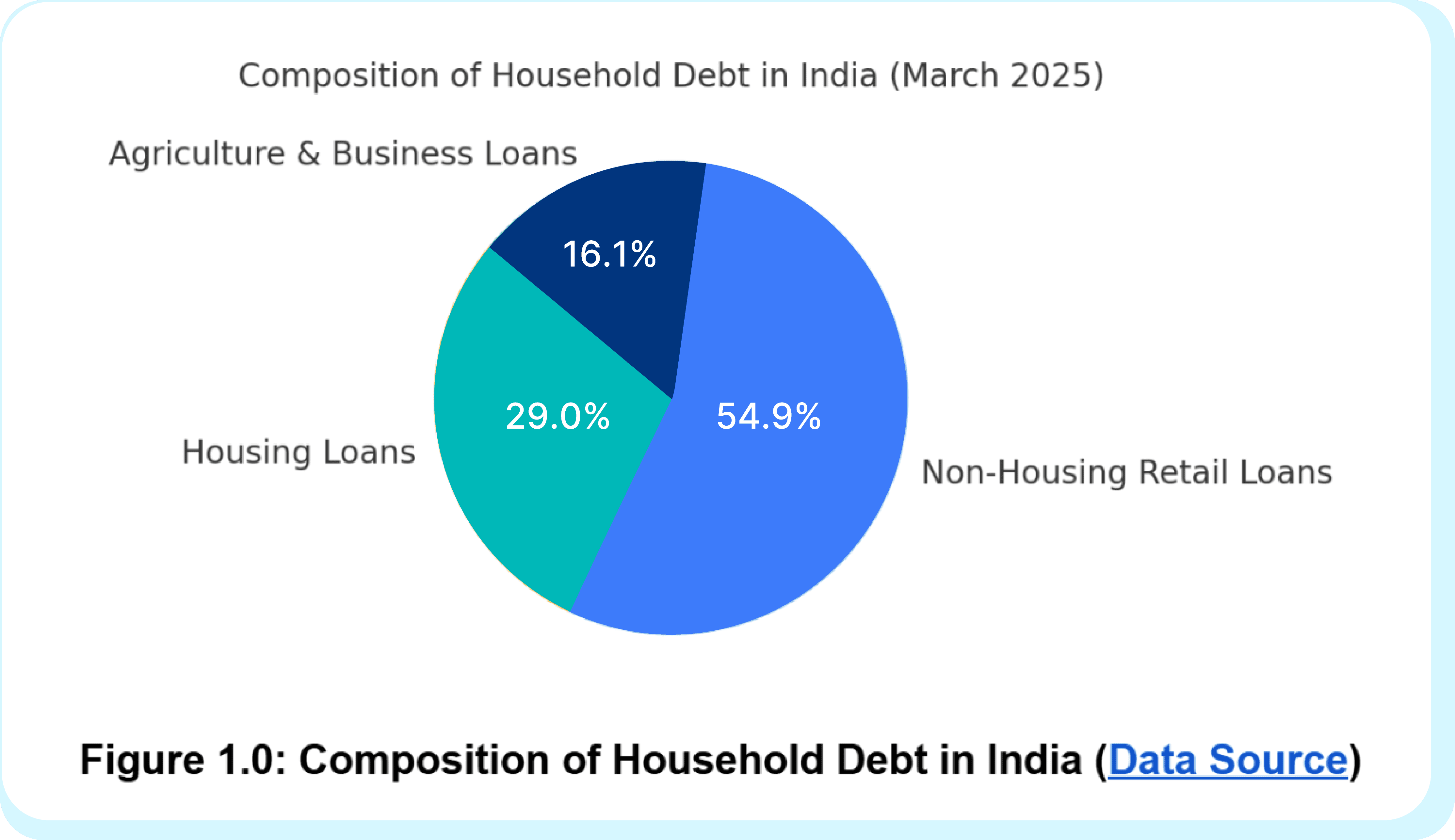

Let us understand the areas where Indian households are using loaned money the most:

A major share of household debt India is linked to housing loans, as owning a home remains a key financial goal. Education loans, though smaller in proportion, have been gaining traction with the rising demand for higher education and overseas studies. Personal loans and credit card debt India are also witnessing rapid growth, especially among younger consumers who are more comfortable with short-term credit.

Impact Of Household Debt On The Indian Economy

Debt or loans can be perceived from different perspectives and lenses. There are both positive and negative aspects of increasing debt on the markets, economic systems, and people’s lifestyle. Even though the debt to income ratio in India is low, it can rise due to change in the consumption patterns. First, let us consider the negative impact.

Debt is the only thing that can make you bankrupt. If you do not have to pay periodic interest and principal repayments, there is a chance that you might not be able to live your life comfortably, but you will always be solvent.

Loans give you an illusion of having wealth and income, and if used wrong, it could be disastrous for your personal financial planning.

Rising interest rates increase the Indian households loan burden, particularly for families with limited disposable income.

Unsecured loans, such as rising personal loans India and credit card dues, are especially vulnerable to defaults when economic conditions weaken. High debt-to-income ratios can strain household budgets, leading to reduced savings and, in turn, limiting long-term wealth creation. However, consumption and demand in a market is often stimulated by short and long-term loans. Housing loans, for example, stimulate the real estate sector and allied industries such as cement, steel, and consumer durables.

Similarly, education loans contribute to the development of human capital, while personal loans and credit cards help sustain consumer demand, especially in urban centres. This rise in borrowing has supported financial inclusion and expanded the reach of India’s formal credit system.

Also Read: How To Save Money From Salary

Managing Household Debt Smartly

It is important that you make the best use of available loans and avoid taking any borrowings that are high-interest. It is critical to not overspend and ensure a healthy balance between income, expenses, and liabilities. Taking huge loans for short-term factors such as holidays, expensive gadgets, and other lifestyle related expenses from high-interest sources (such as credit cards or personal loans) can be quite disastrous for your personal finances. Hence, it is important to keep household debt risk in India to lower levels.

Borrowing should ideally be aligned with long-term goals such as buying a home or funding education. Always have a monthly budget and in no conditions should your repayments exceed 30-40% of your projected monthly incomes.

Another important practice is to prioritize low-interest, secured loans (like home loans) over high-interest, unsecured borrowing.

Also, never miss out on investing and allocate a fixed sum out of your income into investments. Always have a planned approach towards investment and use portfolio diversification to ensure consistent returns over periods. Instruments such as bonds, fixed-income securities, or even fractional investment platforms offer steady returns and help balance the risks of borrowing.

Conclusion

Household debt can be both a powerful enabler and a financial risk, depending on how it is managed. While credit allows families to achieve goals like home ownership, education, and lifestyle upgrades, excessive borrowing can lead to repayment stress. The key lies in financial discipline, keeping EMIs within affordable limits, maintaining an emergency fund, and balancing debt with regular saving and investment. By adopting thoughtful financial planning, households can transform debt into a tool for long-term wealth creation rather than a liability.

Looking beyond traditional borrowing and lending? Login to Grip Invest and get access to alternative fixed-income opportunities that can help families diversify their portfolios and build financial security with confidence.

FAQs on Household Debt In India

1. What is household debt in India?

Household debt in India refers to the total money owed by individuals and families to banks, NBFCs, or other lenders. It includes home loans, personal loans, education loans, vehicle loans, and outstanding credit card balances.

2. How much household debt is considered safe?

A general rule is to keep total EMIs within 30–40% of monthly income. This ensures that borrowing remains manageable while leaving enough room for savings and essential expenses.

3. How can I manage household debt effectively?

Prioritize low-interest loans like housing, avoid piling up high-cost credit card debt, and build an emergency fund. Diversifying income through investments such as bonds or fixed-income products can also reduce over-reliance on loans.

References:

1. The Times Of India, accessed from: https://timesofindia.indiatimes.com/business/india-business/india-gdp-growth-q1-fy26-live-updates-first-quarter-indian-economy-growth-gross-domestic-product-data-donald-trump-tariffs/liveblog/123580996.cms

2. The Economic Times, accessed from: https://economictimes.indiatimes.com/news/new-updates/indias-average-household-debt-rises-23-in-2-years-says-financial-expert/articleshow/122345585.cms?from=mdr

3. The Hindu, accessed from: https://www.thehindu.com/business/Economy/indias-rising-household-debts-are-not-worrisome-sbi-report/article69678649.ece

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks, including delay and/ or default in payment. Read all the offer-related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for the consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001