How To Save Tax For Salary Above 20 Lakhs: Smart Deductions And Investment Strategies

Individuals with a high salary of more than 20 lakh annually face many tax obligations. Their net income might be reduced by paying a large amount of income tax. Therefore, it is important for individuals with high salaries to have a plan to deal with their taxes to save some part of their salary.

Smart tax planning can provide a high-income earner in India an opportunity to save a significant amount of money. This can be done by using the right deductions and investments to reduce your tax bill.

The main opportunity available for those in the old tax system includes utilising the exemption available under Section 80C, and you can use your NPS contribution, which can lead to tax savings of over 1 lakh. If this is not utilised, then the individual is likely not to be in the best financial position because more money could be used to fund an individual's personal goals.

Understanding Tax Regime Choices

If you are considering which of the old (previous) or new tax regimes will work best for you when looking at these two systems, you will need to see the benefits of each system.

The old tax system will provide many deductions associated with a salaried employee. In fact, there will be higher brackets that require higher taxes to be paid by salaried employees. On the other hand, the new regime provides lower tax rates with fewer available deductions.

By comparing the impact of the old and new tax regimes on a salary of INR 20 lakh, we can see that if an individual is able to claim deductions that accumulate to more than INR 3 lakh per year. This will help them save more money by using the old tax regime than they would through the new tax regime.

Old vs New Tax Regime Comparison

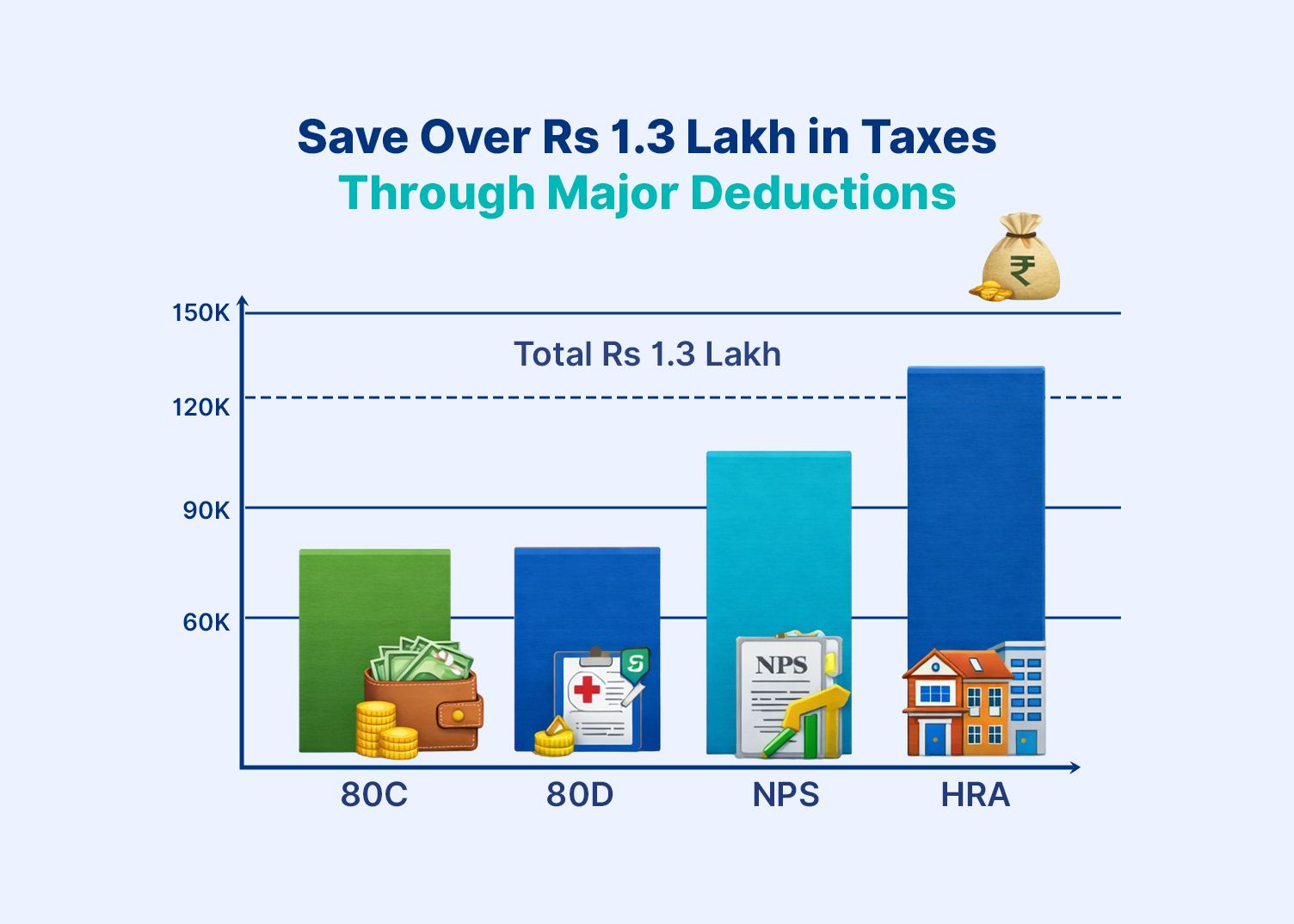

The significant difference between the two regimes lies in their respective abilities to affect taxable income. In the old regime, an individual would receive a total of up to INR 1.5 lakh worth of deductions from taxable income under Section 80C. This will also include deductions for salaried employees India, like HRA and other allowances, before calculating graduated tax rates reaching up to 30% on an individual's taxable income.

When it comes to the new tax regime, the rates are significantly lower. In fact, the maximum rate is at 30%. So, this shows how the old regime works better for those who prefer fewer deductions and simpler filing.

When Each Regime Works Better

As the previous taxation regime will be advantageous as long as cumulative deductions total between 3-4 lakh annually through investments made in a proactive manner.

Whereas an employee with very few claims below 2 lakh annually will benefit from the new taxation regime.This is one of the most important tax saving decisions for a 20 lakh salary earner.

Key Deductions High Income Earners Should Use

When an individual earns a high salary, it can greatly reduce his/her tax liability through strategic utilisation of tax deductions. This is allowed in the income tax law, such as utilising the Section 80C tax deduction for investment, along with other tax deductions that provide protection to the taxpayer from being placed in higher tax brackets. This would include health insurance and the National Pension Scheme (NPS) deductions.

- Section 80C and Retirement Investments

Salaried individuals can claim deductions of up to INR 1.5 lakh under Section 80C for various investment types, including

- Public Provident Fund (PPF),

- Equity Linked Savings Scheme (ELSS),

- And/or Employees' Provident Fund (EPF) contributions.

The tax-free growth provided by these deductions will ultimately help to accumulate a retirement corpus through the use of compound interest.

This deduction is applicable to reduce taxable income at the maximum slab rate. Therefore, yields a benefit of up to Rs 46,800 in savings for a taxpayer whose marginal tax rate is 30%, as illustrated by the professional who receives a deduction upon investing the full amount and watching his/her tax liability reduce.

- Health Insurance and NPS Benefits

Besides section 80C, there is another exemption under Section 80D, which allows a deduction of an extra INR 25,000 on payment of health insurance plots. Besides these, a taxpayer may also benefit themselves with the National Pension System (NPS) under Section 80CCD(1B). It offers an extra deduction of INR 50,000 and forms an extraordinary protection-retirement savings synergy without incurring redundancy on both the deduction or limit.

Investment-Based Tax Saving Strategies

Tax efficiency can be increased beyond just using basic deductions, and by using investment-based strategies like:

- ELSS and Retirement Planning

Equity-linked savings scheme mutual funds give investors a deduction under section 80C along with a three-year lock-up period. This allows them to be in the best position possible for investing for the long-term, as well as paying no taxes while receiving a direct return from investments.

- Tax-Efficient Fixed Income Investments

Tax-efficient fixed income investments like PPF (current approx. 7.1% tax-free interest) and legacy tax-free bonds (approx. 5-5.5% YTM, interest exempt u/s 10(15)) protect returns from tax while shielding from bracket creep. This protects the returns of fixed-income investments from bracket creep and inflation.

How To Improve Tax Efficient Returns?

To elevate overall portfolio efficiency, high earners should prioritise avenues like tax-free bonds that guarantee fixed returns without tax liability, enhancing net yields far beyond taxable alternatives and integrating effortlessly with tax planning for high income salary India. These plans reduce leakage enabling reinvestment to achieve faster growth in asset categories.

1. Tax-Free Bonds: 5-6% rate fully tax-exempted bonds outperform the taxable equivalents after taxes. In fact, a 5 lakh investment will save 15,000 each year, and best used as income in the absence of fiscal drag.

2. Arbitrage Funds: The tax stands at 7 percent on debt-like returns after one year, which is an opportunity to combine both safety and tax benefits. A 2 lakh investment yields market free returns effectively.

3. Debt Mutual Funds: Debt mutual funds held over 24 months qualify for long-term capital gains tax at 12.5% without indexation (post-2023 Finance Act changes). This makes a INR 2 lakh debt mutual fund investment more tax-efficient for long-term growth compared to short-term holdings taxed at your slab rate.

4. Home Loan Advantages: The savings are magnified under 80C of principal, and 24(b) of interest. For example, if you pay INR 2 lakh in home loan interest in a year and are in the 30% slab under the old regime, Section 24(b) alone can reduce your tax by about INR60,000 (excluding surcharge).

Action Steps To Implement Your Tax Saving Strategy

A structured tax planning approach ensures deductions are maximized and compliance deadlines are met.

1. Start Tax Planning Early (April–May): Begin investments in eligible tax-saving instruments at the start of the financial year to avoid last-minute decisions.

2. Use Monthly SIP-Based Tax Saving Investments: Systematic investing spreads contributions across the year and supports disciplined tax planning.

3. rack Deduction Proofs Regularly: Maintain documentation of insurance premiums, rent receipts, loan statements, and investment proofs to avoid filing errors.

4. File Income Tax Returns Before the Deadline: Complete ITR filing before July 31 (unless extended) to avoid penalties and maintain compliance.

5. Review Strategy Annually With a Tax Expert: A yearly consultation with a chartered accountant helps optimize deductions, select the appropriate tax regime, and align tax planning with long-term investment goals.

Conclusion

Earning above INR 20 lakhs puts you in a higher tax bracket, but it also gives you more room to plan smartly. The key is not just choosing between the old and new tax regime, but actively using deductions like Section 80C, NPS, 80D, HRA, and home loan benefits in a structured way. When your investments are aligned with your long-term goals, tax saving becomes a natural outcome, not a last-minute scramble in March.

At the same time, tax planning should not mean locking all your money into low-growth options. A balanced mix of tax-efficient investments and income-generating assets can help you grow wealth while reducing liability. Platforms like Grip Invest can support high-income earners by offering curated fixed-income opportunities that complement your broader tax and investment strategy.

In the end, the goal is simple: reduce unnecessary tax outflow, maximise post-tax returns, and make every rupee work harder for your financial future.

FAQs

1. How can I save maximum tax on a 20 lakh salary?

Under the old tax regime, claim max INR 1.5 lakh from 80C (PPF, ELSS, EPF) + extra INR 50k NPS + INR 25k+ health insurance (80D). Turn everyday expenses like EPF/insurance into big tax savings easily.

2. Which tax regime can be considered for the individuals with high-income?

High income salaried individuals should compare both regimes using a tax calculator, but as a thumb rule, if your total deductions (80C, 80D, HRA, home loan, NPS etc.) are low, the new regime often works better; if they exceed roughly INR 3–4 lakh at a INR 20 lakh income level, the old regime may save more tax.

3. What deductions are available for salaried taxpayers?

You can claim 80C, 80D, NPS, HRA, and home/education loan deductions, and enjoy savings of over INR 5 lakhs in total due to good tax planning.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001