Income Tax Act 2025 vs 1961: What Changes for Indian Taxpayers?

In a historic move, the new Income Tax Act 2025 is set to replace the Income Tax Act 1961 after more than six decades of India following the age-old structure. While this was announced in Union Budget 2025, the change will be effective from April 1st 2026.

So what changes does this Income Tax 2025 bring? And why is it being introduced? Let’s cover all that in detail.

Why Is The Income Tax Act 2025 Being Introduced?

If we go back to the year 1961, the Income-tax Act, 1961 was introduced to replace the earlier 1922 legislation, based on recommendations from the Law Commission (1958) and the Direct Tax Administration Enquiry Committee.

And now, six decades later, the factors that have led to the complexity of India's Income-tax Act, 1961, are as follows:

- Extensive Amendments: The Act has been amended nearly 65 times with more than 4000 amendments over six decades through annual Finance Acts and 19 separate Taxation Laws Amendment Bills. While these changes were intended to keep the law relevant, they significantly increased its length and complexity.

- Numerous Exemptions and Deductions: Over the years, the Act was repeatedly amended to include various exemptions and deductions to support socio-economic goals, such as encouraging savings, boosting exports, promoting balanced growth, and advancing social equity. These provisions included benefits for export income, investments in specific sectors or regions, and spending on rural development.

- Reduced Tax Base and Increased Litigation: The numerous exemptions and incentives significantly reduced the tax base, which in turn contributed to increased litigation, higher administrative costs, and greater compliance burdens.

- Traditional Legal Language: The Act was written in traditional legal language, characterized by long sentences, numerous provisos, and extensive explanations, making it difficult for the average taxpayer to understand.

- Fragmented Structure and Outdated Provisions: The accumulation of amendments and additions led to a fragmented structure. This complexity was further compounded by the presence of outdated provisions that were no longer in use.

When Did The Reform Process Begin?

It was in July 2024 when India’s Finance Minister Nirmala Sitharaman had announced the government’s intent to overhaul the Income-tax Act, 1961.

To lead this effort, an internal Departmental Committee was constituted by the CBDT (Central Board of Direct Taxes) for comprehensive review of the existing Act of 1961. The Committee actively engaged with stakeholders such as industry bodies, professional associations, and field officers of the tax department, through consultations and brainstorming sessions. The Committee also drew insights from international best practices, including tax reforms in Australia and the UK.

Then came the reframing of the Income Tax law framework. Here are the core objectives of the Income Tax Act 2051:

Four core objectives of Income Tax Act 2025

- Simplification: Aim to replace archaic language and redundant provisions with clear, concise, and modern legal text.

- Taxpayer-Centric Approach: Aim to improve ease of filing, reduce litigation, and enhance transparency.

- Digital Integration: Aim to enable faceless assessments and digital compliance to reduce human interface and corruption.

- Global Alignment: Aim to Reflect contemporary economic realities, including taxation of digital assets and global income

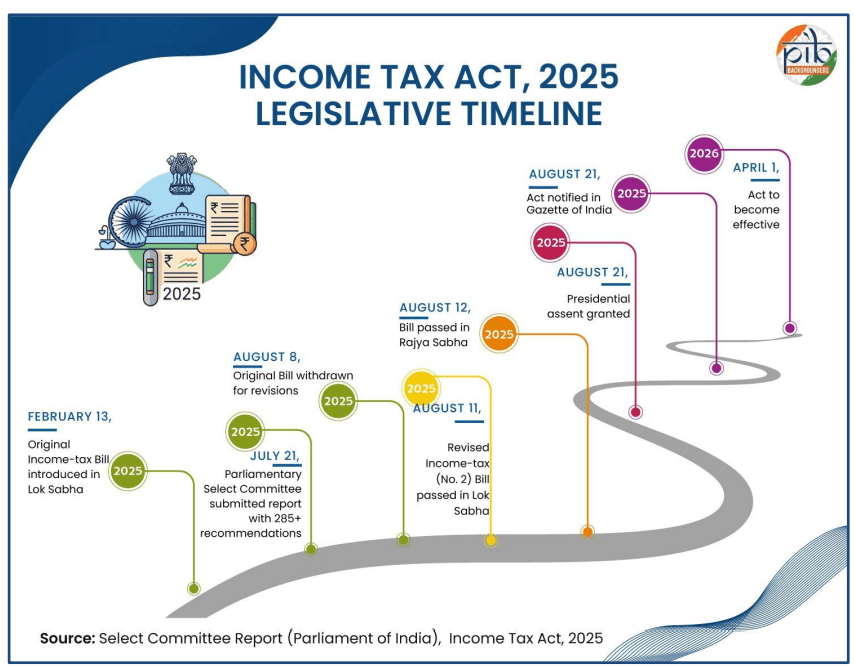

Here’s a brief view of how the Act’s timeline moved:

Key Changes Introduced In Income Tax 2025

When compared to the outgoing Income Tax Act 1961, the Income Tax 2025 has reduced the total number of sections from 819 to 536, and the number of chapters from 47 to just 23. Also, the total words in the new Income Tax Bill 2025 are around 2.6 lakhs, as against 5.12 lakh words in the Income Tax Act, 1961.

Here are the key changes introduced in the new Act1.

1. Introduction of ‘Tax Year’: The Income Tax Act 2025 has simplified tax terminology by replacing the previously used and often confusing terms ‘Assessment Year’ and ‘Previous Year’ with a single, unified concept called the ‘Tax Year’. This has been defined as the financial year for which the income is liable to be taxed, computing a twelve-month period of that financial year commencing on the 1st April and ending on March 31st. This change is expected to result in improving clarity and making it easier for taxpayers to understand which financial period their income and tax filings relate to, hence reducing ambiguity in compliance and interpretation.

2. Govt gets power to frame schemes: The Income Tax Act 2025 also authorizes the Central Government to design new schemes to improve efficiency, transparency, and accountability in tax administration. This can be done by eliminating the interface with the assessee or any other person to the extent technologically feasible, and optimising utilisation of the resources through economies of scale and functional specialisation.

3. Simplified compliance: The Income Tax Act 2025 has brought in multiple provisions together for more clarity. For example, the provisions related to TDS (Tax Deducted at Source), which were earlier distributed across multiple sections, have now been streamlined and grouped under a single section - Section 393. Such a consolidation simplifies the legal framework, thus making it easier for taxpayers, professionals, and authorities to locate and interpret TDS related rules without navigating through numerous clauses scattered across the previous Act.

4. Digital first enforcement: The Income Tax Act 2025 has defined ‘Virtual Digital Space’ as an environment, area, or realm constructed and experienced through computer technology. This includes email servers, social media accounts, cloud servers, online investment and trading accounts, as well as websites for storing details of asset ownership. Also, the Act has broadened the scope of Virtual Digital Assets in order to cover any asset that holds value in digital form and operates using cryptographic ledger systems, such as cryptocurrencies. The Act has clearly mentioned that it is mandatory to furnish information in respect of a transaction of crypto-asset in a statement.

5. Higher HRA Benefit Proposed for Additional Cities: The draft rules as per the Income Tax Act 2025 have proposed extending the 50% HRA exemption to taxpayers residing in rented accommodations in Bengaluru, Hyderabad, Pune, and Ahmedabad2. At present, the 50% salary exemption for HRA purposes has been available only to taxpayers residing in Chennai, Mumbai, New Delhi, and Kolkata. But note that this benefit is only available in the old tax regime.

6. Dispute Resolution: Last but not the least, the Income Tax Act, 2025 has introduced a more robust and taxpayer-friendly framework for resolving disputes through the simplification of tax laws. This is expected to reduce litigation burdens significantly.

Conclusion

The Income Tax Act 2025 marks one of the biggest structural tax reforms in India in over six decades. By reducing sections, simplifying language, introducing the concept of a Tax Year, and strengthening digital enforcement, the government aims to make taxation clearer, faster, and more transparent.

What this really means is fewer confusing provisions, reduced litigation, and a system better aligned with today’s digital and global economy.

As tax rules evolve, investors and taxpayers must stay informed and plan smarter. Platforms like Grip Invest can help individuals explore fixed-income opportunities and build tax-efficient investment strategies alongside the changing regulatory framework, ensuring stability while navigating new tax laws confidently.

FAQs

1. When will the Income Tax Act 2025 come into effect?

The new Income Tax Act 2025 will replace the Income Tax Act 1961 from 1 April 2026, as announced in Union Budget 2025.

2. What is the ‘Tax Year’ under the new Act?

The term “Tax Year” replaces both “Assessment Year” and “Previous Year.” It refers to the financial year (1 April to 31 March) for which income is taxed, simplifying compliance and understanding.

3. Has the new Act changed HRA exemption rules?

Yes. The draft rules propose extending the 50% HRA exemption to Bengaluru, Hyderabad, Pune, and Ahmedabad under the old tax regime, in addition to the existing metro cities.

References:

1. Income tax, accessed from: https://incometaxindia.gov.in/Documents/Act/Income-tax-Act-2025.pdf

2. Tax Guru, accessed from: https://taxguru.in/income-tax/draft-income-tax-rules-2026-old-regime-re-emerges.html

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001