New ATM Rules From April 2026: What Bank Customers Need To Know

Ever since the first ATM was installed in India (in the late 80s), banks have made sure to enhance the effectiveness and efficiency of their automated machines.

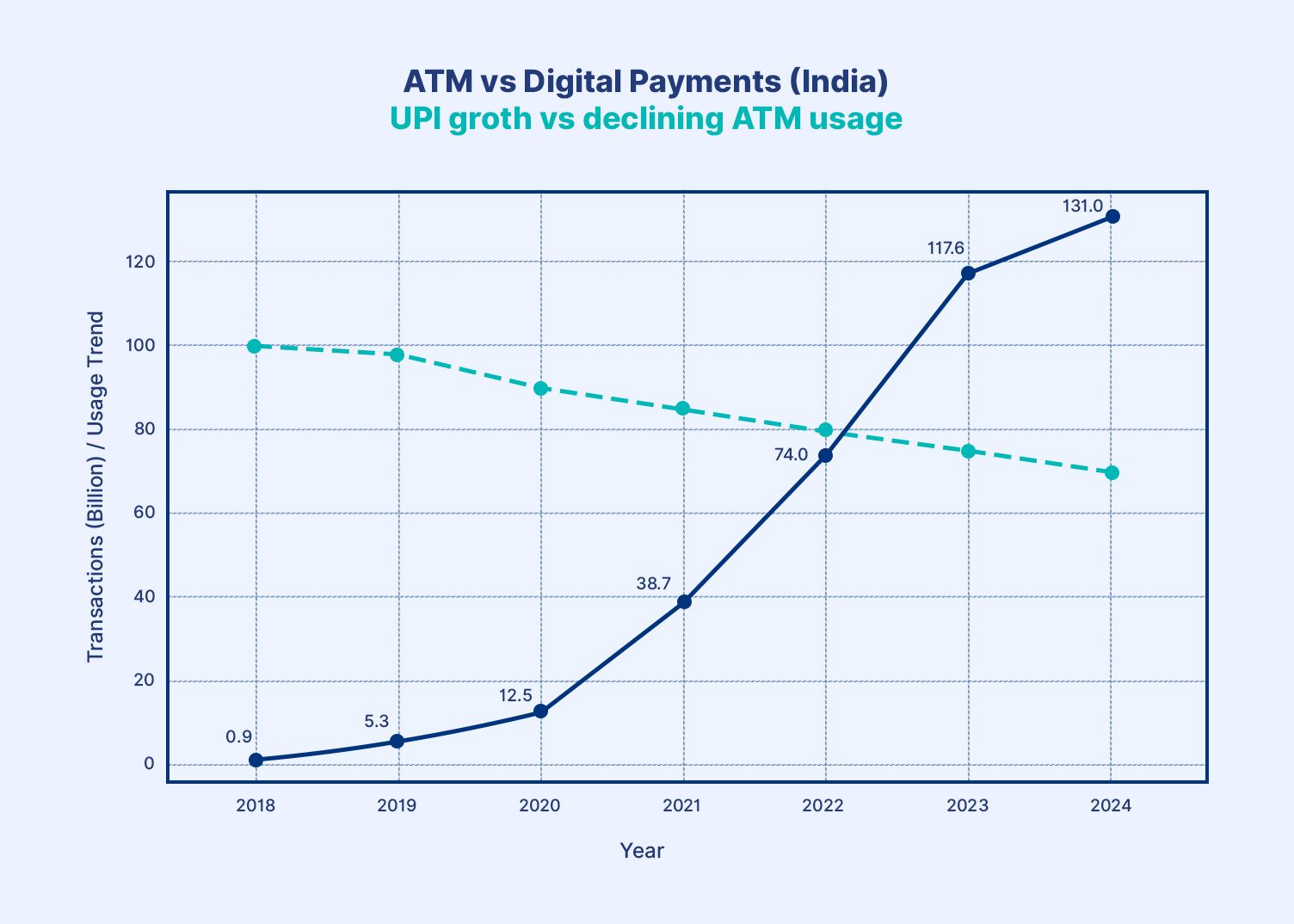

The ATMs, which were usually seen at posh metro locations with vestibules and proper set-ups, could be easily spotted in colonies, highways, and remote locations. Even though digital payments have slowed down the expansion of ATM networks in the country, there are still more than 2.5 lakh ATMs across cities and towns1.

(ATM usage is shown as a trend index based on RBI-reported declines in cash withdrawals and ATM visits, scaled to illustrate the directional shift rather than exact transaction volumes.)

As cash withdrawals remain an essential part of everyday life, especially in semi-urban and rural parts of the country, it is important to understand the impact of the new ATM rules 2026 in India, which come into effect from 01 April.

These updates impact transaction limits, charges, and even how certain withdrawals, such as UPI-based cash withdrawals, are counted.

For every bank customer, it is critical to be aware of these changes and optimize daily banking needs.

What Are The New ATM Rules ?

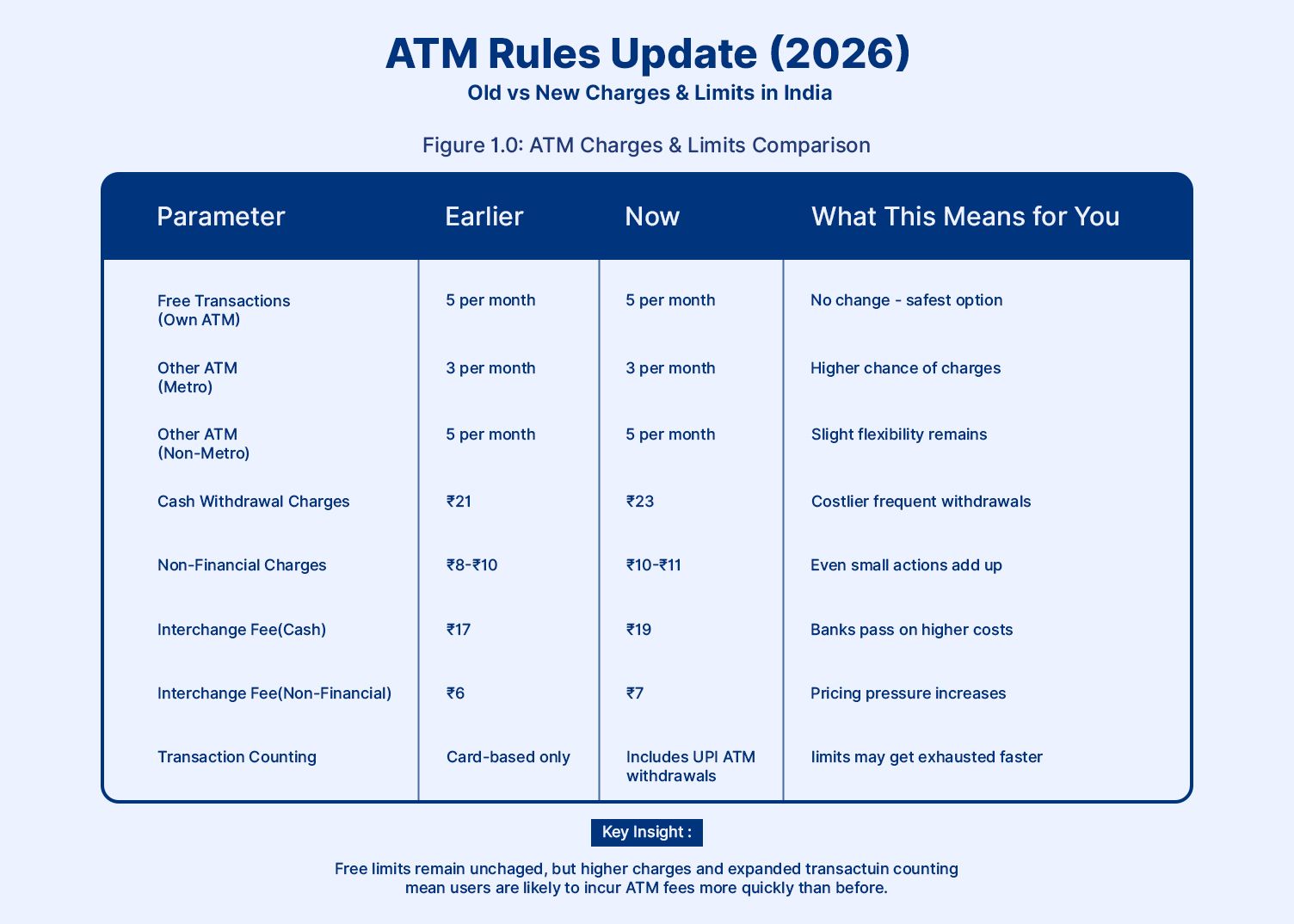

1. Changes in Free Transaction Limits

There are a few changes in the free transaction limits, but the RBI has ensured that the existing fee structure (for free transactions) is not altered too much. As per the existing limits, an ATM holder is allowed:

Own bank ATMs: 5 free transactions per month

Other bank ATMs:

- 3 free transactions in metro cities

- 5 free transactions in non-metro areas

The transaction limits include both financial (such as cash withdrawals) and non-financial (such as balance enquiry) transactions. However, the key change from April 2026 is that certain digital transactions, including UPI-based ATM withdrawals, may now be counted in the aforementioned limits.

However, the limitations depend on the bank and the account category.

2. Revised Charges After Free Limit

Once customers exceed the free transaction limit prescribed above, they will be charged INR 23 per transaction (excluding GST). Earlier, the ATM charges in India were INR 21 per transaction (excluding GST).

3. Interchange Fee Updates

An interchange fee refers to charges paid by one bank to another when customers use another bank’s ATM. The financial transaction fees were increased to INR 19 per transaction, and the non-financial fee has been increased to INR 7 per transaction2.

Impact On Bank Customers

1. Increased Withdrawal Costs

Even though the increase in withdrawal cost might look small (INR 2 per transaction), it can easily add up for customers who frequently withdraw cash. For instance, if someone makes 20 additional withdrawals (over and above the free limit), it can result in a total cost of INR 460 plus GST, which is a substantial amount.

2. Metro vs Non-Metro Differences

Customers in non-metro regions are given tighter limits, with only 3 free transactions at other banks’ ATMs, compared to 5 in metro regions.

3. Behavioural Shift

These changes are likely to push users toward:

- Fewer ATM visits

- Higher withdrawal amounts per transaction

- Increased adoption of digital payments

How To Avoid Extra ATM Charges

1. Use Digital Payment Methods

Even though digital payments have become quite popular in the past few years, a significant portion of the population still prefers cash to other forms of payment. With increased withdrawal charges, it is an excellent time to switch to digital payments such as UPI apps and wallets, which are convenient and incur no fees, regardless of the number of transactions in a period.

2. Plan Withdrawals Efficiently

You need not wait until the eleventh hour for your withdrawals, and you must acknowledge the importance of monthly budgeting. It is also important to track your ATM usage to ensure you do not surpass the prescribed limits.

3. Prefer Own Bank ATMs

You can switch banks if there are no nearby branches or ATMs from your service provider. It helps reduce the need to use other banks’ ATMs, even during emergencies.

4. Track Monthly Usage

Monitoring ATM usage through mobile banking apps or statements can prevent unexpected charges.

How Major Banks Are Changing ATM Rules From April 1, 2026

While the RBI sets the overall framework, individual banks can implement specific changes within it. Three major banks have announced notable revisions effective April 1, 2026.3

Bank-Wise ATM Rules at a Glance (April 2026)

| Bank | Own ATM (Free) | Other ATM Metro | Other ATM Non-Metro | UPI Counted? | Charge Beyond Limit |

| HDFC Bank | 5/month | 3/month | 5/month | Yes | INR 23 + GST |

| PNB | 5/month | 3/month | 5/month | Not specified | INR 23 + GST; daily cap INR 50K–75K |

| Bandhan Bank | 5/month | 3/month | 5/month | Not specified | INR 23 (fin), INR 10 (non-fin), INR 25 (failed) ? |

| SBI / Others | 5/month | 3/month | 5/month | Per bank policy | INR 23 + GST |

Source: ET4

What This Means For Personal Finance

1. Cost Optimisation

Even though there will not be a significant impact on your long-term financial planning, this can still give you a chance to become more mindful of charges, review statements, and keep track of your withdrawals and ATM usage. You can notice a slight improvement in your financial discipline.

2. Shift Toward Digital Banking

As charges for ATM withdrawal limit in India continue to rise, more people are looking for digital alternatives that are more convenient and quicker.

3. Smarter Cash Flow Management

Balancing cash usage with digital payments is now a key aspect of personal finance. Maintaining adequate liquidity while minimising transaction costs is essential.

Conclusion

The new ATM rules effective from April 2026 may not drastically change how people withdraw cash, but they do signal a subtle shift in how banking costs and convenience are evolving. With higher charges beyond free limits and UPI-based ATM withdrawals now being counted, everyday banking decisions will require a bit more planning.

For users, this is less about restriction and more about awareness. Tracking usage, optimising withdrawals, and gradually adopting digital payments can help minimise unnecessary charges while improving overall financial discipline.

More importantly, small cost leakages like ATM charges often go unnoticed but can add up over time. Building smarter money habits, even at this level, plays a key role in long-term financial health.

And while you optimise day-to-day banking, balancing your overall portfolio with stable, income-generating investments can help you stay on track, platforms like Grip Invest make it easier to explore such options alongside your regular financial planning.

FAQs On New ATM Rules

1. What are the new ATM rules in 2026?

ATM rules remain largely unchanged, but banks have aligned UPI ATM withdrawals with regular ATM transactions, meaning they may now count toward your monthly free limit.

2. How many free ATM transactions are allowed?

- Own bank ATM: 5 per month

- Other bank ATM:

- 3 (metro cities)

- 5 (non-metro cities)

3. What are ATM withdrawal charges now?

- INR 23 per transaction after free limit (plus GST)

4. Do UPI-based ATM withdrawals count in free transaction limits?

Yes, from April 2026, UPI-based ATM withdrawals may be counted within your monthly free transaction limit, depending on your bank’s policy.

5. Are ATM charges the same across all banks in India?

No, while the RBI sets the maximum charge (INR 23 per transaction after free limit), individual banks may have slight variations in policies, especially for premium accounts.

6. Are non-financial ATM transactions also chargeable after the free limit?

Yes, non-financial transactions like balance enquiries or mini statements may also be charged once you exceed the free monthly limit.

References

1. Finnovate, accessed from: https://www.finnovate.in/learn/blog/why-atm-numbers-are-falling-in-india

2. ET, accessed from: https://economictimes.indiatimes.com/industry/banking/finance/banking/atm-withdrawals-will-now-cost-more-as-rbi-raises-interchange-fees-new-changes-other-details/articleshow/119475017.cms?from=mdr

3. ET, accessed from: https://shorturl.at/aYzUw

4. ET accessed from: https://shorturl.at/OxrTX

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001