Securitised Debt Instruments (SDIs): Common Terminologies That Can Affect Your Portfolio

With interest rates rising and economic uncertainties looming ahead, many investors are looking to restructure their portfolios to protect against potential losses. One way to do this is through securitised debt instruments (SDIs) like mortgage-backed securities and asset-backed securities. However, the terminology around these securities needs to be clarified for the average investor. In this article, we will break down some of the most common jargon and phrasal verbs around securitised debt so that you are well-versed with the concept of SDIs and can make informed decisions about what to hold onto or offload from your portfolio.

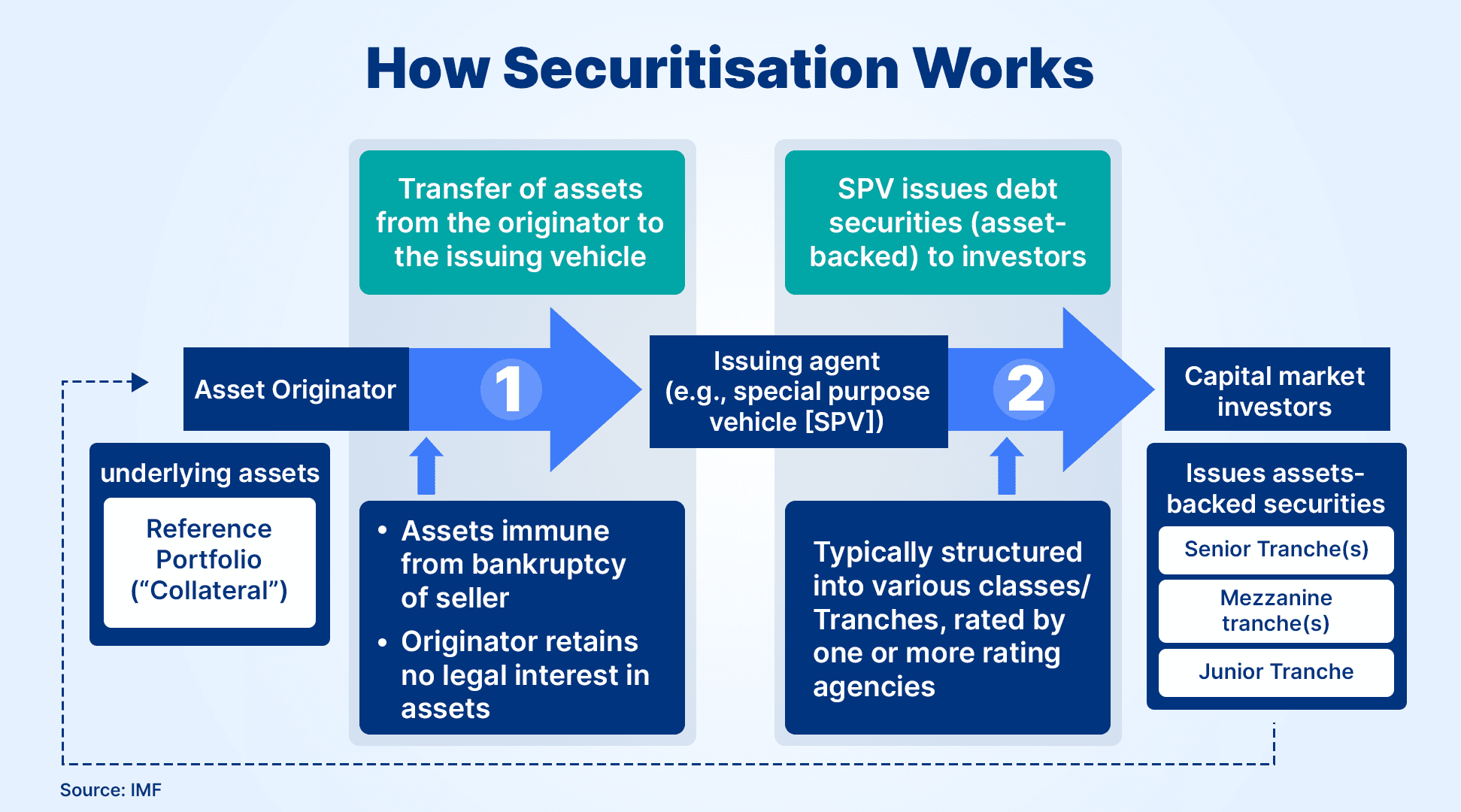

The ABC Of Securitisation

- Arranger: The financial institution that structures and arranges the securitisation deal. The arranger puts together the various parties and assets and oversees the creation of the special purpose vehicle (SPV).

- Securitisation Trust/Special Purpose Vehicles (SPV): A securitisation trust or special purpose vehicle (SPV) is a legal entity created by a company to carry out a specific financial transaction or activity. The SPV is separate from the parent company and insulates it from the risks of the parent company's activities. Typical uses of an SPV include securitising assets like mortgage loans or bonds, isolating financial risk, and undertaking speculative investments.

- Borrower IRR: The internal rate of return (IRR) calculates the percentage return you would earn from investing. To calculate IRR, you look at the expected cash inflows and outflows over the life of the investment. IRR is the discount rate that makes the net present value of those cash flows equal to zero. In other words, the return results in a breakeven investment. IRR helps you compare investment options.

- Collateral: Assets provided as security for the repayment of the bonds issued by the SPV. This collateral can be drawn if the borrower cannot pay the interest and the principal. It provides extra comfort to SDI investors.

- Pass-through Certificate (PTC): These securities, issued by the SPV, give investors ownership in the trust and allow them to gain exposure to the cash flows from the pooled assets. PTC holders receive principal and interest payments from the underlying loans.

- Listed, Rated, and Compliant: PTCs issued by the SPV are rated by a credit rating agency, listed on a stock exchange, and compliant with SEBI and RBI regulations to assure investors. The arranger ensures the deal meets these requirements.

- Non-performing Assets (NPA): Non-performing assets (NPAs) are loans where the borrower has missed payments and defaulted. As per RBI guidelines, a loan is classified as non-performing if the principal's interest and/or instalment remains overdue for over 90 days. High levels of NPAs reduce the credit quality of the loan pool and must be weeded out by the arranger. After 90 days of non-payment, the loan is categorised as an NPA.

- Originator: The bank or financial institution that originates and owns the assets to be pooled and securitised. The originator transfers the assets to the SPV to get them off its balance sheet.

- Servicer: The entity that manages the loans in the securitised pool. This involves collecting payments, managing non-payments, and following up with borrowers. The servicer provides reports on the loan pool to the SPV and investors.

- Trustee: An independent third party that oversees the SPV to ensure all parties live up to their duties and obligations. The trustee acts in the best interest of the investors who purchase the PTCs. These trustees are registered with SEBI and provide additional security to the investor’s portfolio.

- Mortgage Pool Or Pool Of Assets: A mortgage pool or pool of assets refers to a group of mortgage loans bundled together and sold as an investment. The mortgages within the pool are backed by residential or commercial real estate. Investors can purchase shares or securities in the mortgage pool and receive some interest payments on the underlying mortgages.

- Securitisation: Securitisation is taking an illiquid asset, or group of assets, and transforming them into a security or negotiable financial instrument through financial engineering. Typically, the cash flows from the underlying assets are redirected to a special purpose vehicle (SPV) that issues securities sold to investors. The SPV services the securities by collecting the cash flows from the original assets and distributing them to the security holders. Securitisation aims to make the assets more liquid, allow risk to be transferred and diversified, and reduce funding costs.

Case Study: InvoiceX - First SDI Product From Grip Invest

InvoiceX, an SDI product of Grip Invest, is the first-ever credit-rated, diversified version of Invoice Discounting. InvoiceX brings a fresh concept to the Indian investment landscape- it allows individual investors to diversify into pools of short-term corporate debt by purchasing trade receivable-backed securities. This innovative instrument ticks many boxes for attractive features for investors, earning risk-adjusted returns.

By opening up short-term corporate credit to individual investors, InvoiceX significantly expands the range of products available to gain fixed-income exposure. Investors can now look forward to regular interest payouts at pre-determined intervals while having their principal amount paid back closer to maturity. The diversified nature of InvoiceX helps spread out risk across various underlying corporate loans backed by invoices rather than concentrating exposure to a single borrower.

Importantly, InvoiceX carries the seal of approval and confidence inspired by RBI compliance and credit ratings from renowned agencies. The instrument adheres to RBI's framework for securitisation, affirming its regulatory standing. Furthermore, strong credit ratings by agencies like India Ratings validate the product's creditworthiness, providing reassurance to investors on the product's soundness.

Oversight on InvoiceX comes from a SEBI-registered trustee, who monitors it for timely payments and flags potential delays or shortfalls. This prudent supervision layer acts as an ongoing safeguard of investors' interests. Additionally, with a security cover buffer of up to 20% of investment value, InvoiceX provides a cushion against possible defaults.

InvoiceX offers diversification in two ways- diversification from other assets in an investor's portfolio and diversification within InvoiceX. Overall, as India's first diversified, rated short-duration instrument, InvoiceX brings something novel to the table for investors looking to broaden their investment horizons.

InvoiceX is just one of the many securitised investment opportunities available on Grip Invest. With options like LoanX and LeaseX, investors can diversify their fixed-income portfolios with regulated, rated, and secured instruments.

Conclusion

Securitised debt instruments (SDIs) like asset-backed securities and mortgage-backed securities make up an essential part of many investment portfolios. Investors must understand the terminology and risks associated with these securities to make informed decisions. Investors who take the time to research and educate themselves about these instruments are better equipped to analyze their exposures and manage their portfolios accordingly.

When assessing securitised products, be sure to delve into the details of the offerings, including the underlying assets and cash flows. Try not to get bogged down in complex structuring, but pay attention to factors that could impact performance over time. Evaluate the risks diligently and determine if they align with your investment objectives.

If you decide to add securitised investments, start small to test the waters. Ease into positions slowly over time as you become more comfortable. Monitor your holdings closely to catch any signs of trouble before they become bigger issues. Be ready to pare back or unload positions that appear riskier than initially thought.

Want to keep your finger on the pulse of the financial world? Explore Grip Invest today to learn about securitised debt instruments and their benefits.

FAQs

1. What does “securitisation” mean in simple terms?

It’s when banks/NBFCs pool loans and sell them as securities to investors, converting illiquid loans into tradable assets.

2. Why do banks/NBFCs use SPVs (special purpose vehicles) to issue SDIs?

SPVs act as separate legal entities that isolate risk from the bank/NBFC, protecting investors if the bank/NBFC defaults.

3. What is an “asset-backed security” versus a “mortgage-backed security”?

Asset-backed securities are backed by loans like auto or credit cards, while mortgage-backed securities rely on home loans.

4. How do credit enhancements like “first-loss facilities” help investors?

They ensure the originator absorbs initial losses, giving investors added safety and confidence.

5. Why are SDIs split into different tranches (like senior vs junior)?

Tranches distribute risk—senior investors get priority payments, while junior tranches take higher risk for better returns.

6. What is “over-collateralisation,” and why is it used?

It means adding extra loans beyond the required amount, offering investors a cushion against defaults.

7. What’s an “early amortisation event” and why does it matter?

It’s when loan repayments start sooner than expected, often triggered by defaults—impacting investor cash flows.

8. How does an SPV pay investors from loan repayments?

The SPV collects borrower EMIs and distributes them to investors as interest and principal payments.

Want to stay at the top of your finances?

Join the community of 2.5 lakh+ investors and learn more about Grip, the latest financial knick-knacks and shenanigans that take place in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities are subject to risks. Read all the offer-related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading. This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for the consequences of any actions taken based on the information provided. For more details, please visit https://www.gripinvest.in/.

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001.