Solvency vs Liquidity: Key Differences Every Investor Should Know

The 2025 AFP Liquidity Survey states that 61% of companies now consider safety their top short-term investment objective, showcasing a strong caution about the company's financial management in the current risky economic scenario1.

In such a climate, it is more necessary than ever to distinguish a company's immediate cash flow from its overall financial strength. While liquidity focuses on fulfilling obligations in the short term, solvency is associated with a firm's long-term viability.

Getting a thorough understanding of the core differences between solvency vs liquidity is the only way to truly assess risk. This blog discusses how these two pillars interact to define a firm’s overall stability and success.

Why Solvency And Liquidity Are Often Confused

While both terms measure a company’s financial health, they are frequently confused because they both assess the ability to pay debts.

Common Financial Misconception

The most common mistake is assuming that a profitable or asset-rich company is naturally healthy in every way. Many believe that if a firm is solvent (meaning its assets exceed its total liabilities), it cannot fail. However, a company can be solvent on paper but still go broke if its wealth is tied up in illiquid assets like real estate or heavy machinery. On the other hand, having plenty of cash on hand (high liquidity) does not guarantee long-term survival if the business is buried under mountains of long-term debt that it cannot eventually repay.

Importance For Investors And Businesses

Maintaining a balance between these two metrics is vital for several reasons:

1. Day-to-Day Operations: Adequate liquidity ensures a company can cover its daily expenses, such as GST payments, vendor invoices, and employee salaries, without any interruption.

2. Risk Management: Strong solvency acts as a financial support to the company, enabling it to survive longer during economic uncertainties when revenue is likely to dip.

3. Creditworthiness: Lenders, both banks and NBFCs, consider solvency ratios to evaluate the risk of lending to a business for long-term loans or project financing.

4. Shareholder Confidence: Shareholders are concerned about the company's ability to distribute dividends; thus, liquidity plays the role of the best guarantee while solvency represents the assurance that, in the event of a total bankruptcy, the investment will not be completely wiped out.

Also Read: What Is Liquidity Risk and How To Manage it?

What Is Liquidity?

Liquidity refers to how quickly and easily an individual or business can convert assets into cash to meet immediate, short-term obligations (typically those due within one year).

For example, like Mr Sharma, who might hold INR 2 Lakhs in a Fixed Deposit (FD) and INR 50 Lakhs in a plot of land. While the land represents significant wealth, the FD is his only truly liquid asset; he can break it instantly to pay for an emergency medical bill, whereas the land could take months to sell.

Similarly, for a business like ABC Ltd., liquidity is about having enough Current Assets to cover Current Liabilities. By maintaining a healthy balance in its bank account and tracking money owed by clients, the firm ensures it can settle GST liabilities and office rent on time. This is best understood by looking at their short-term financial position:

| Current Liabilities | Amount (INR) | Liquid Assets (Current) | Amount (INR) |

| Short-term Vendor Dues | 3,00,000 | Cash & Bank Balance | 5,00,000 |

| GST & Tax Payable | 1,00,000 | Accounts Receivable (Debtors) | 4,00,000 |

| Employee Salaries | 2,00,000 | Inventory (Stock) | 2,00,000 |

| Total Current Debt | 6,00,000 | Total Current Assets | 11,00,000 |

In this example, ABC Ltd. is highly liquid because its ready assets (INR 11 Lakhs) comfortably cover its immediate bills (INR 6 Lakhs). Managing this balance is an important part of monitoring financial ratios in India to avoid operational disruptions

What Is Solvency?

Solvency is a measure of a company’s long-term financial health and its ability to meet all financial obligations, both now and in the distant future. While liquidity is about the now, solvency is about the forever. A solvent entity is one whose total assets are greater than its total liabilities, resulting in a positive net worth.

For a business, being solvent means it has a sustainable capital structure. It means that the company generates enough profit and possesses enough value to remain operational over the long term, even if it has to pay off every single debt it owes.

Solvency vs Liquidity: Core Differences Explained

Although both are essential for a company’s survival, the liquidity vs solvency difference primarily lies in the window of time each one addresses and the specific risks they present.

| Aspect | Liquidity | Solvency |

| Duration | Short-term (days to months) | Long-term (years to decades) |

| Operational impact | Affects daily greasing of the wheels (paying GST, payroll) | Affects the ability to borrow for expansion or R&D |

| Ease of correction | Often fixed via short-term credit lines or factoring | Usually requires restructuring, equity infusion, or downsizing |

| Cost of failure | High opportunity cost (late fees, missed vendor discounts) | High terminal cost (bankruptcy and liquidation) |

| Asset impact under stress | Forced sale of assets at discounts to raise cash | Assets insufficient to cover total liabilities |

Time Horizon

Liquidity is particularly a short-term measure, focusing on a company’s ability to pay bills due within days or months. Maintaining a current ratio of at over 1.00 is generally considered a healthy benchmark to manage immediate cash flow needs2.

In contrast, solvency is a long-term indicator of structural durability, assessing a firm's viability over several years or even decades.

Risk Implications

The financial consequences of failing to balance these two pillars can lead to distinct types of institutional distress:

- Operational Paralysis: Poor liquidity leads to technical default, where a company cannot fund daily functions like payroll or vendor payments, even if it owns valuable assets.

- Total Capital Erosion: Solvency risk represents a terminal threat where total liabilities outweigh assets, meaning the business is fundamentally underwater.

- Asset Fire Sales: When liquid cash is low, companies are often forced into market liquidity risk. This means selling fixed assets like machinery or real estate at a massive discount just to raise immediate cash, which permanently erodes the company's value.

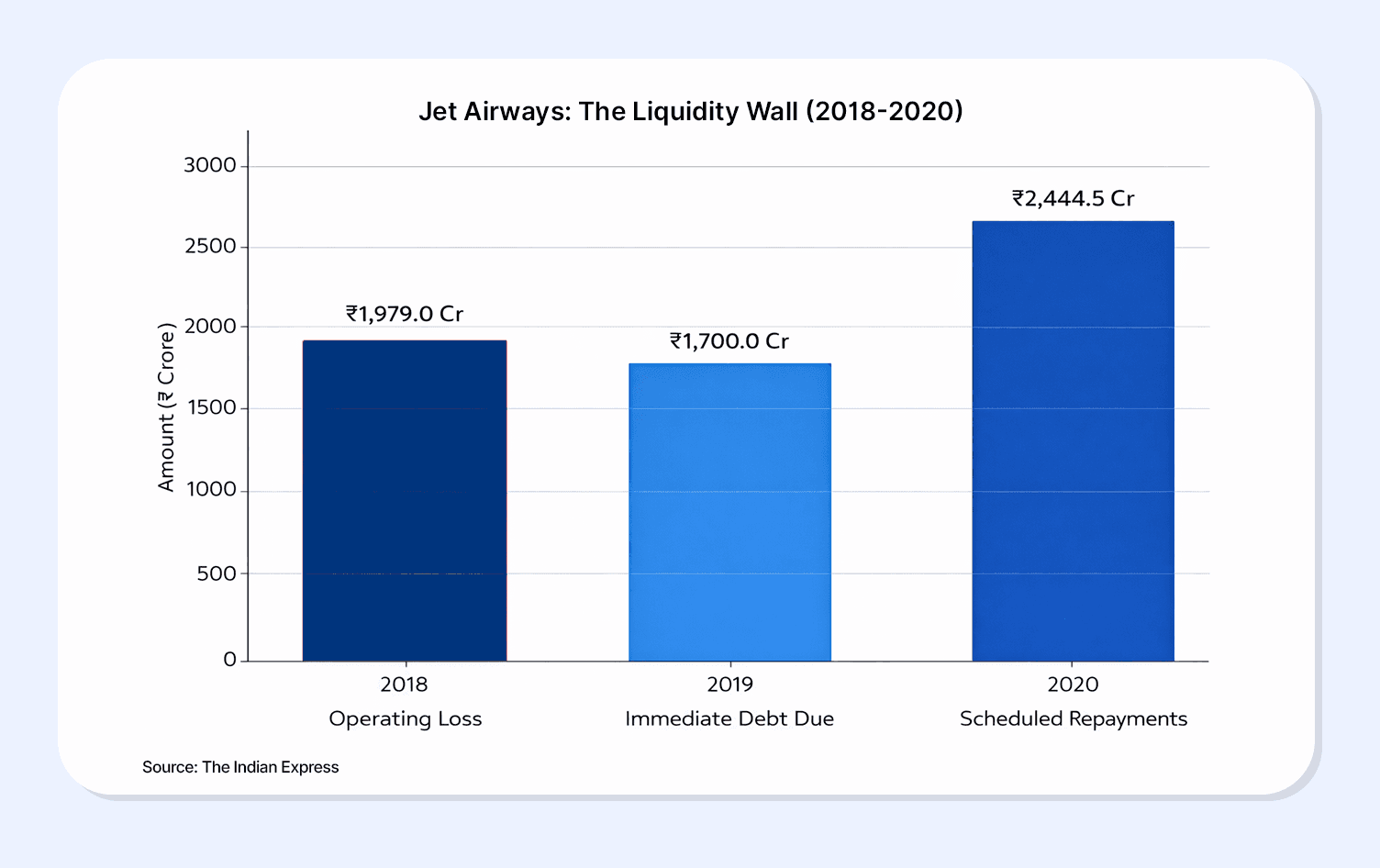

The 2019 collapse of Jet Airways is an example of this divergence3. By September 30, 2018, the company’s liquidity was severely stressed, with total gross debt reaching INR 8,411crore. The airline faced a mounting liquidity wall across three main stages: an operating loss of INR 1,879.0 crore in 2018 (H1 FY19), immediate debt repayments of INR 1,700 crore due in early 2019, and a further INR 2,444.5 crore scheduled for 2020.

Despite holding 16 owned aircraft available for possible monetisation, the inability to bridge this immediate cash void led to a total operational shutdown, proving that illiquidity can destroy even a solvent brand.

Why Solvency And Liquidity Matter In Investment Decisions

Understanding the interlink between solvency and liquidity is an imperative step in investment risk analysis, as it helps investors identify whether a company's financial distress is a temporary hurdle or a terminal failure.

Evaluating issuers

Before committing capital, investors must evaluate if an issuer is cash-strapped or structurally weak. A company may report accounting profits, but if those profits are locked in non-cash forms like ageing inventory, it lacks the flexibility to meet sudden demands. This mismatch often forces companies into expensive, emergency borrowing, which eventually degrades their long-term stability.

To assess liquidity, investors primarily use the Current Ratio to determine if a firm can meet its obligations over the next 12 months:

Current Ratio = Current Assets / Current Liabilities

Importance Of Bonds And Fixed-Income Instruments

In the debt market, these metrics serve as the ultimate safety checks. While liquidity ensures the issuer can meet its immediate coupon obligations (periodic interest payments) on time, solvency assures that the total asset base is sufficient to repay the principal amount at maturity.

To evaluate solvency, professional analysts track the Debt-to-Equity (D/E) Ratio, which reveals the company’s reliance on borrowed funds relative to its own capital. High leverage increases default risk for bondholders:

Debt-to-Equity Ratio = Total Liabilities / Shareholders Equity

Along with these ratios, choosing a regulated and transparent investment platform is equally important. Platforms like Grip curate fixed income opportunities after evaluating issuer liquidity, solvency, and leverage metrics, helping investors access debt instruments where these fundamental risk checks are clearly disclosed and easier to assess.

FAQs On Solvency vs Liquidity

1. What is the difference between solvency and liquidity?

Liquidity is the short-term ability to pay immediate bills, while solvency measures long-term viability by ensuring total assets exceed total liabilities over many years.

2. Can a company be liquid but insolvent?

Yes. A company may have enough cash for current expenses but still be insolvent if its total debt far outweighs its assets, making long-term survival impossible.

3. Why is solvency important for bond investors?

Solvency ensures that an issuer is structurally strong enough to return the full principal amount at maturity, protecting the investor's initial capital over the bond's duration.

4. How do investors assess financial stability?

Investors use the Current Ratio to check for immediate cash health and the Debt-to-Equity Ratio to verify long-term stability.

References:

1. Financial Professionals, accessed from: https://shorturl.at/mYV2L

2. Investopedia, accessed from: https://www.investopedia.com/terms/c/currentratio.asp

3. ICRA, accessed from: https://www.icra.in/Rating/GetRationalReportFilePdf?id=75657

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks and shenanigans that take place in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001