Types of Non-Performing Assets (NPA): Meaning, Classification And Examples

For banks and non-banking financial institutions, loans are a primary source of revenue and profitability. However, assets critical to their balance sheets can become non-performing when borrowers consistently delay or default on repayments beyond prescribed regulatory thresholds.

From 2013 to 2018, the Indian banking sector suffered a major setback due to a massive accumulation of non-performing assets (NPAs). This surge in bad loans in banks, particularly in private-sector banks, intensified and peaked in 2018, necessitating a critical intervention by the Reserve Bank of India (RBI).

NPAs are not only a banking term; they also reflect the financial health of lending institutions. When bank loans no longer generate income for banks, the impact extends beyond balance sheets. The ramifications reflect credit availability, interest rates, investor/creditor confidence, and overall stability of the bond markets. Understanding the various types of non-performing assets enables investors, borrowers, and policymakers to assess their risks more accurately, particularly given the close integration of lending and capital markets.

In India, the Reserve Bank of India (RBI) sets guidelines for non-performing assets (NPAs) that establish standards for identifying, classifying, and reporting bad loans in banks. These classifications dictate everything from bank profitability to bond yields, thus making it an extremely important concept in finance.

What Is A Non-Performing Asset (NPA)?

An NPA refers to a loan or advance for which the borrower has not made any interest or principal repayments for a specified period. An NPA is classified under RBI guidelines if the overdue repayment period exceeds 90 days from the EMI due date. After that period, the lender no longer earns revenue from the NPA, so it loses value.

Let’s say you borrowed INR 5 lakh and have not been able to pay your EMI for 3 consecutive months. At this point, your loan has 'moved' from a “standard asset” to the NPA category (in the bank’s financial statements). This 'movement' has created additional provisioning requirements at the bank level, thereby negatively affecting their ability to provide new loans.

Types Of Non-Performing Assets as per the RBI

The RBI has mentioned NPA classification based on the duration of default and the likelihood of recovery. Each type reflects the level of credit risk and overall economic conditions. Let us understand the types of non-performing assets:

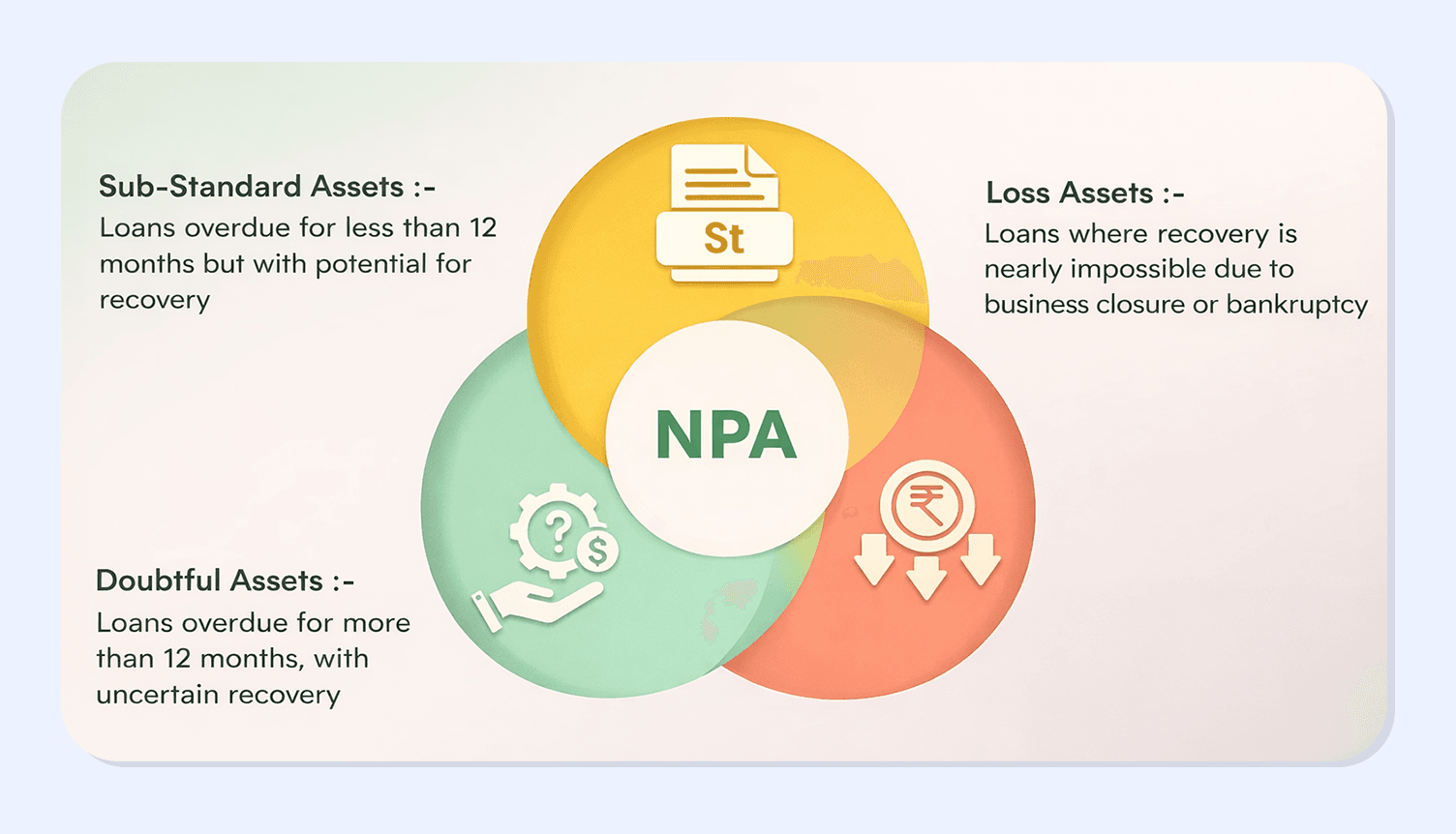

1. Substandard Assets

Loans that remain unpaid for up to 12 months are considered substandard assets. At this stage, repayment issues are evident, but the possibility of recovery still seems favourable. Such NPAs show clear credit weakness but are repayable. Banks typically provision around 10%-15% for such loans, reflecting a moderate level of risk.

Substandard assets account for most newly classified NPAs and are closely scrutinized by lenders to prevent further deterioration in asset value.

2. Doubtful Assets

A substandard asset that hasn't been paid in over a year gets classified as a doubtful asset. By that time, the likelihood of the debtor's full recovery is uncertain, and the lender is less certain of recovering their full investment.

The increase in provisioning required for doubtful assets rises rapidly, with requirements ranging from 25% to 100%, depending on the collateral's value.

Doubtful assets are signals of severe financial problems and typically receive heightened attention from bond investors and credit rating agencies.

3. Loss Assets

Loss assets are loans that a lender or auditor has identified as uncollectible or unlikely to provide any value if they were recovered.

Although there may still be potential for recovery, it will not be financially feasible to treat them as an economic asset.

Banks must provide 100% of these assets, effectively writing them off.

Loss assets rank lowest in the RBI NPA Classification System and, as such, directly erode banks' capital.

How loans Turn Into NPAs

Loans do not become Non-Performing Assets (NPAs) overnight. The transition typically occurs gradually as repayment behaviour deteriorates. At the time of disbursal, loans are classified as standard assets as long as repayments remain timely. If repayments remain overdue for more than 90 days, the loan is classified as an NPA and categorised as a substandard asset. If the default continues beyond 12 months, it is reclassified as a doubtful asset. Eventually, when recovery prospects are negligible, the loan is designated as a loss asset.

Reserve Bank of India (RBI) data shows that early intervention at the substandard stage significantly improves recovery outcomes, underscoring the importance of continuous NPA monitoring.

How Do NPAs Affect Your Bond Investment?

NPAs affect bond investors and banks, particularly for corporate bonds and debt mutual funds.

When a company or financial institution has a high NPA ratio, it indicates low-quality assets and cash-flow problems. Therefore, it is perceived as having higher default risk, a common reason for the IDR to be reduced, which in turn leads to higher bond interest rates. Higher returns generally relate to higher default risk for investors.

To evaluate the risk profile of banking NPA types, an investor should review the company's asset quality disclosures and its gross and net NPA ratios. They should also get an overview of NPA provisioning coverage and NPA trends over several quarters, as found in the company's annual report and credit rating rationale.

For Example, say a leading Finserv Company issues bonds offering attractive interest rates, but the gross NPA from unsecured loans increases significantly. The agencies may lower their bond ratings or reduce their outlook if GP for NPAs increases. Thus, upon the agency's downgrade announcement, bond prices may drop for both the original bondholder and all other bondholders in the secondary market.

Hence, understanding the nature of NPAs is critical for evaluating banks and making informed investment decisions in the bond market.

Conclusion

The number of non-performing assets (NPAs) at an institution provides insight into the institution's credit discipline, economic conditions, and risk management. In establishing RBI NPA norms, a system for categorizing loans has been created that allows stakeholders to quickly identify collection stress levels. Each categorization will also entail different consequences for lenders and investors in their relationship with banks. For those investing in debt instruments or monitoring financial performance, familiarity with the banking NPA types is quite critical.

Visit Grip Invest today!

FAQs on Types of NPAs

1. After how many days does a loan become a non-performing asset (NPA)?

As per Reserve Bank of India norms, a loan becomes an NPA if interest or principal remains overdue for more than 90 days from the due date.

2. What is the difference between substandard, doubtful, and loss assets?

Substandard assets are early-stage NPAs with some recovery potential, doubtful assets face serious uncertainty in recovery, and loss assets are considered uncollectible and are usually written off completely.

3. Do NPAs affect only banks, or do they impact investors too?

NPAs affect investors as well. High NPAs weaken a lender’s financial position, increase default risk, and can lead to bond rating downgrades and price declines in debt instruments.

4. Can a loan move back from NPA to a standard asset?

Yes. If overdue payments are fully cleared and the account performs regularly for a sustained period, banks can upgrade an NPA back to a standard asset, subject to RBI guidelines.

References:

1. RBI, accessed from: https://www.rbi.org.in/commonman/English/scripts/Notification.aspx?Id=889

2. HDFC sky, accessed from: https://hdfcsky.com/sky-learn/share-trading/non-performing-assets

3. Kotak bank, accessed from: https://www.kotak.bank.in/en/stories-in-focus/loans/personal-loan/understanding-npa-fullform-meaning-types.html

4. Groww, accessed from: https://groww.in/p/non-performing-assets

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001