Unified Pension Scheme: A Deep Dive Into UPS For Central Government Employees

Understanding The Unified Pension Scheme (UPS)

The pension scheme for the Central Government Employees has been a debatable topic for long. The reason behind this is the demand of the government employees to restore the Old Pension Scheme (OPS) which they find secure and guaranteed. To solve this issue the government brought a new pension scheme called Unified Pensions Scheme (UPS). The cabinet approved this pension plan for government employees in August 2024 and it was rolled out effective April 1, 2025.

The Unified Pension Scheme is regulated by Pension Fund Regulatory and Development Authority (PFRDA) and it operates as an optional pension scheme under the existing National Pension System (NPS) architecture. UPS is a blend of Old Pension Scheme (OPS) and National Pension System (NPS). The objective of the UPS is to provide secured retirement benefits to the central government employees. Although the UPS is guaranteeing the retirement benefits, still the adoption to UPS is slow.

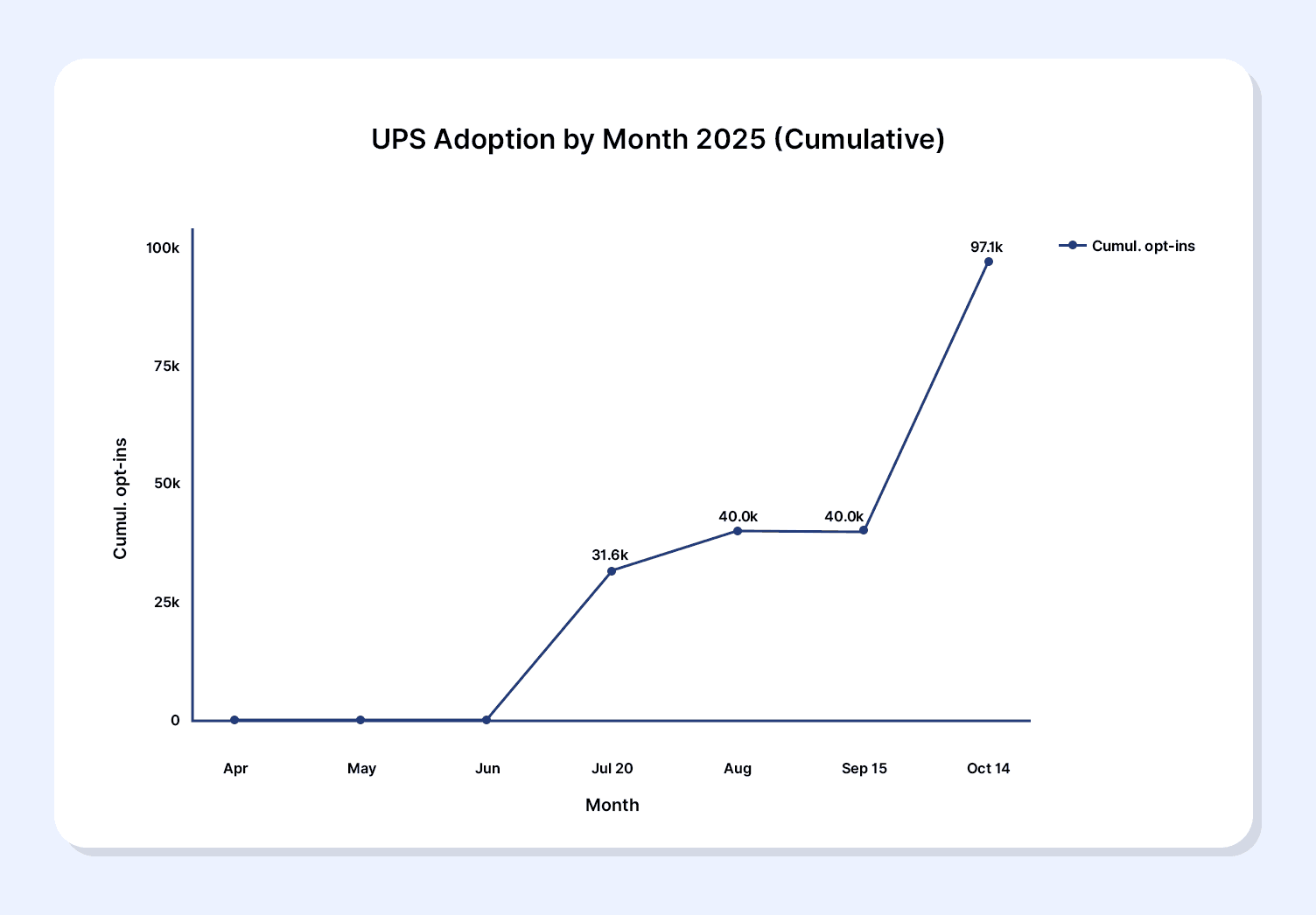

As of September 30, 2025, only about 4.5% (1.11 lakh) of the 23.93 lakh NPS employees had opted to switch to UPS1. This slow adoption of the UPS highlights the need for employees to understand the intricacies of the new system. In this article, we will discuss the benefits and drawbacks of the UPS and where else the government employees can invest their money to secure a peaceful retirement life.

What Is The Unified Pension Scheme (Ups)?

The Unified Pension Scheme (UPS) is an option that has been given to the Central Government employees. This option comes under the National Pension System (NPS) architecture only. This is a move taken by the government to combine the features of the Old Pension Scheme (OPS) and NPS. It was recommended by the T.V. Somanathan committee in 2023.

Government employees have several concerns with the NPS including no guarantee of the pension, inflation and more. The UPS has been brought to address these concerns of assured, inflation - indexed, and adequate retirement benefits. The government has made some major amendments in the contribution structure of the pension plan to assure the guaranteed retirement corpus.

Contribution Structure Of UPS

1. Employee Contribution: Employees contribute 10% of Basic Pay + Dearness Allowance (DA).

2. Government Contribution: The Central Government provides a matching 10% contribution to the employee’s individual corpus.

3. Additional Government Contribution: An estimated 8.5% of Basic Pay + DA is provided as an additional contribution to a separate Pool Corpus, which is used solely for supporting the assured payouts2.

This results in a total employer contribution of 18.5% of basic salary plus DA.

Key Benefits: Why UPS Offers Financial Security

1. Assured Fixed Pension Payout: The biggest benefit of UPS is assured payout after the retirement. In order to become eligible for assured payout, an employee must complete at least 25 years of qualifying service. This assured payout is the 50% of the average basic pay of the employee drawn in the last 12 months prior to superannuation. With this assured payout the employees get the same benefit of assured payout of the Old Pension Scheme.

- If the employee’s qualifying service period comes between 10 and 25 years, he/she is still eligible for proportionate payout.

- For instance, an employee retiring with INR 80,000 basic pay after 25 years will receive INR 40,000 monthly under UPS, providing predictability compared to variable NPS returns.

2. Guaranteed Minimum Pension: If a government employee retires after completing at least 10 years of the qualifying service, he/she becomes eligible for a minimum guaranteed payout of INR 10,000 per month. However, this guarantee comes with a condition that the employee has contributed regularly and no withdrawals are done.

3. Inflation Protections (Dearness Relief): Another benefit of the Unified Pension Scheme (UPS) is the addition of Dearness Relief (DR). This makes UPS different from NPS as it is available on both the assured payout and the family payout. It’s important to mention here that DR will be payable only when the pension payout starts.

4. Assured Family Pension and Support: UPS also provides spousal benefits. In case of the demise of the pensioner, the spouse is eligible for a payout of 60% of the pension. Additionally a death gratuity is also payable to the family/nominee regardless of the tenure of the service if the government employee dies during the service3.

5. Lump Sum Payment and Gratuity: The employee gets the benefit of lump sum payment as well as gratuity both under the UPS. The lump sum payout is calculated as one-tenth (1/10th) of the employee’s monthly emoluments (Basic Pay + DA) for every six months of completed qualifying service. Retirement Gratuity is also added after 5 years of service.

6. Enhanced Employer Contribution: The total employer contribution from the government is 18.5% of the Basic Pay + DA. This is higher than the employer’s contribution in the NPS.

Drawbacks And Implementation Challenges Of UPS

1. The adoption of the Unified Pension Scheme (UPS) has been slow. As of 30th Sep 2025, only 1.11 lakh employees out of total 23.93 lakh Central Government employees under the NPS opted for it and switched from NPS to UPS4.

Source: Economic Times5 and Upstox6

2. Another drawback of UPS is the financial trade-off. Many employees believe that NPS being the market linked is still the better option. They believe that NPS is market linked and it can offer better payout than the assured payout of UPS on retirement.

3. Another limitation of UPS is the matching contribution of the employer. In NPS the matching contribution to the retirement corpus is 14% from the government, however in UPS it comes down to 10%. Although with additional 8.5% contribution to Pool Corpus for assured payout the total employer contribution under UPS becomes 18.5%.

4. Another concern is the unavailability of the option to switch back to the NPS. Once an employee switches to UPS from NPS, it’s final and cannot be reversed.

5. Next limitation of the UPS is delay in VRS payout. If an employee takes a voluntary retirement his assured UPS payout only commences from the date the employee would have superannuated (e.g., age 60).

Operational Details Of UPS

1. Unified Pension Scheme (UPS) is regulated by the Pension Fund Regulatory and Development Authority (PFRDA) and is operated within the existing structure of the NPS.

The deadline to opt-in for UPS was extended to 30th November 2025, considering the slow adoption of the new pension system.

2. The existing employees who are willing to switch from NPS to UPS can use form A2 and new employees who wish to opt for UPS can use form A1.

3. The Individual Corpus (IC) and the Benchmark Corpus (BC) values of the employees are shared with them on a regular basis.

4. Employees can make partial withdrawals as well for up to 3 times during the service (up to 25% of the contributions) subject to a three-year lock-in period.

Alternatives To UPS and NPS

The objective of UPS is to add assurance of fixed income to the NPS. If employees are not convinced with the new system that the government has brought, there are other alternatives available that can help them build a good retirement corpus with fixed income. Employees can invest in Corporate Bonds and Corporate Fixed Deposits to generate fixed income. Corporate bonds with ‘AAA’ rating are considered low risk fixed income investments and they offer 9 - 12.5% fixed returns to the investors. Additionally, Corporate FDs are also there offering better returns than Bank FDs. Another option for the personal retirement corpus can be the securitised debt instruments (SDIs). These debt instruments offer fixed returns and their monthly returns along with the monthly principal payout can be automatically invested into a debt mutual fund via Infinite on Grip Invest. This way, the government employees can build their own personal retirement corpus independent of government arrangements.

Conclusion

The Unified Pension Scheme (UPS) was brought by the government to address the concerns of uncertainty with the National Pension System (NPS). With UPS the government added the assurance of guaranteed retirement benefits for the Central Government employees. This new system works under the same system of NPS and gives an option to the employees to switch from NPS to UPS. The government increased the total contribution to the employee’s retirement fund from 14% in NPS to 18.5% in UPS. Out of this 18.5%, 8.5% is added to a separate pool which will ensure the guaranteed pension for the employees.

However, despite adding assurance, the adoption of UPS has been slow. The government employees can look for other alternatives like Corporate Bonds and SDIs along with the UPS to ensure a good retirement corpus. To learn more about the retirement planning and fixed income investing login to Grip Invest today.

Frequently Asked Questions On UPS

1. Which one is better, NPS or UPS?

Both the schemes have their own benefits and limitations. UPS is better for those employees who are risk averse and want an assured pension fund. With UPS they get an assured pension of 50% of the average basic pay and a minimum payout of INR 10,000 monthly. On the other hand NPS is market linked and hence carries market risk. But it comes with better returns potential as well. Hence, NPS is better for those who are ready to take risk for higher pension amounts.

2. What is the difference between a Unified Pension Scheme and NPS salary?

The key difference between UPS and NPS is in their payout mechanism. NPS does not guarantee the minimum pension amount but UPS comes with an assured pension amount. This amount is equivalent to 50% of the average basic salary. Employees must complete their 25 years of service to become eligible for this. If the service period is between 10 - 25 years a proportionate amount is given.

3. Why are people not opting for UPS?

The main reason behind the slow adoption of UPS is that NPS is market linked and it has a potential to offer higher pension amounts in the long run. Another concern is a lower matching contribution than the NPS. In NPS it is 14% however in UPS it is 10%.

4. What is the lock period of UPS?

To become eligible for an assured pension amount an employee must complete a minimum of 10 years of qualifying service and for full benefits 25 years of service is required. For partial withdrawals, which are permitted up to three times, a three-year lock-in period is required.

References:

1. India express, accessed from: https://indianexpress.com/article/india/few-takers-ups-employees-jantar-mantar-protest-press-old-pension-scheme-10317565/

2. Financial services, accessed from: https://financialservices.gov.in/beta/sites/default/files/2025-02/FAQs-UPS.pdf

3. Clear tax, accessed from: https://cleartax.in/s/unified-pension-scheme-ups

4. Business today, accessed from: https://www.businesstoday.in/personal-finance/story/unified-pension-scheme-just-4-of-central-government-shift-to-new-system-500238-2025-10-30

5. Economic times, accessed from: https://economictimes.indiatimes.com/news/economy/policy/over-31500-govt-employees-opt-for-ups-till-july-20-finance-minister-nirmala-sitharaman/articleshow/122950267.cms

6. Upstox, accessed from: https://upstox.com/news/personal-finance/latest-updates/ups-nps-switch-november-30-deadline-96-of-central-govt-staff-continue-under-national-pension-system/article-183850/

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001