Monthly Interest On INR 10 Lakh Fixed Deposit: Returns Across Different Interest Rates

Fixed Deposits (FDs) are age-old avenues of earning fixed returns on your money that is kept safe with a bank or financial institution. With advancements in the financial literacy of Indians, the demand for FDs in the rural sector of India has been surging. This surge of 14% year on year in the FD holdings of the rural sector outpaces the urban sector’s 10% for the second quarter of FY261.

FDs are instruments that balance risk and provide steady returns in the investment portfolio. Investors often consider INR 10 Lakh as a starting investment corpus. They may aim to generate passive income on this amount without risking losses. FD returns are not linked to market movements. Because of this reliability, many investors view it as a dependable way to earn regular income. Therefore, their INR 10 Lakh savings are often invested in FDs that are considered safe and steady.

Monthly Interest On INR 10 Lakh FD

The income from a fixed deposit depends mainly on the interest rate offered by the institution. In India, most large banks currently offer average FD rates around 5.5% to 7% for regular customers, depending on tenure2. Corporate fixed deposits and certain alternative fixed-income instruments may offer slightly higher rates to attract investors.

Many banks also offer a monthly interest payout option, allowing investors to receive a monthly income from an INR 10 lakh FD, which can be useful for retirees or individuals looking for a steady cash flow. For example, Aman wants to invest INR 10 Lakh in a safe and steady asset.

Therefore, he considers investing in an FD. However, he is willing to invest through either banks (regular FD) or through companies (corporate FD). The table below highlights the comparison of bank FD rates and corporate FD rates offered by Grip Invest.

| Investment Type | Interest Rate | Monthly Income | Annual Interest |

| Regular FD | 6% | INR 5,000 | INR 60,000 |

| Corporate FD | 8% | INR 6,666 | INR 80,000 |

Both investment types help create a steady return base. However, corporate FDs have an edge in returns due to the additional risk they entail. Thus, investors seeking higher income with greater risk can consider corporate FDs.

Real Returns After Inflation

Inflation is the persistent rise in prices of goods and services in a country over time. As inflation increases, citizens' purchasing power decreases. With rising prices, people can consume less of what they were able to in the same amount. Therefore, the value of the money that you presently hold also goes down. This also erodes the value of money held in bank accounts, such as FDs. Thus, investors must look at the real returns of any investment.

Real Return = Nominal Return - Inflation Rate

To generate a real return on your FDs, aiming for an FD rate above inflation is ideal. For instance, if Aman finally decides to invest INR 10 Lakh in a bank FD that pays 6% interest for 5 years. His investment becomes INR 13.38 Lakh in 5 years3. On paper, this looks like healthy growth. The story changes as he accounts for the inflation of 6%.

If prices rise at 6% annually, the inflation factor over 5 years becomes (1.06)^5 = 1.338.

This means that something costing INR 10 Lakh today would cost roughly INR 13.38 Lakh after 5 years. This is the same amount of your corpus when invested in an FD. Therefore, effectively, your FD is not generating real returns. The FD will only manage to keep pace with inflation.

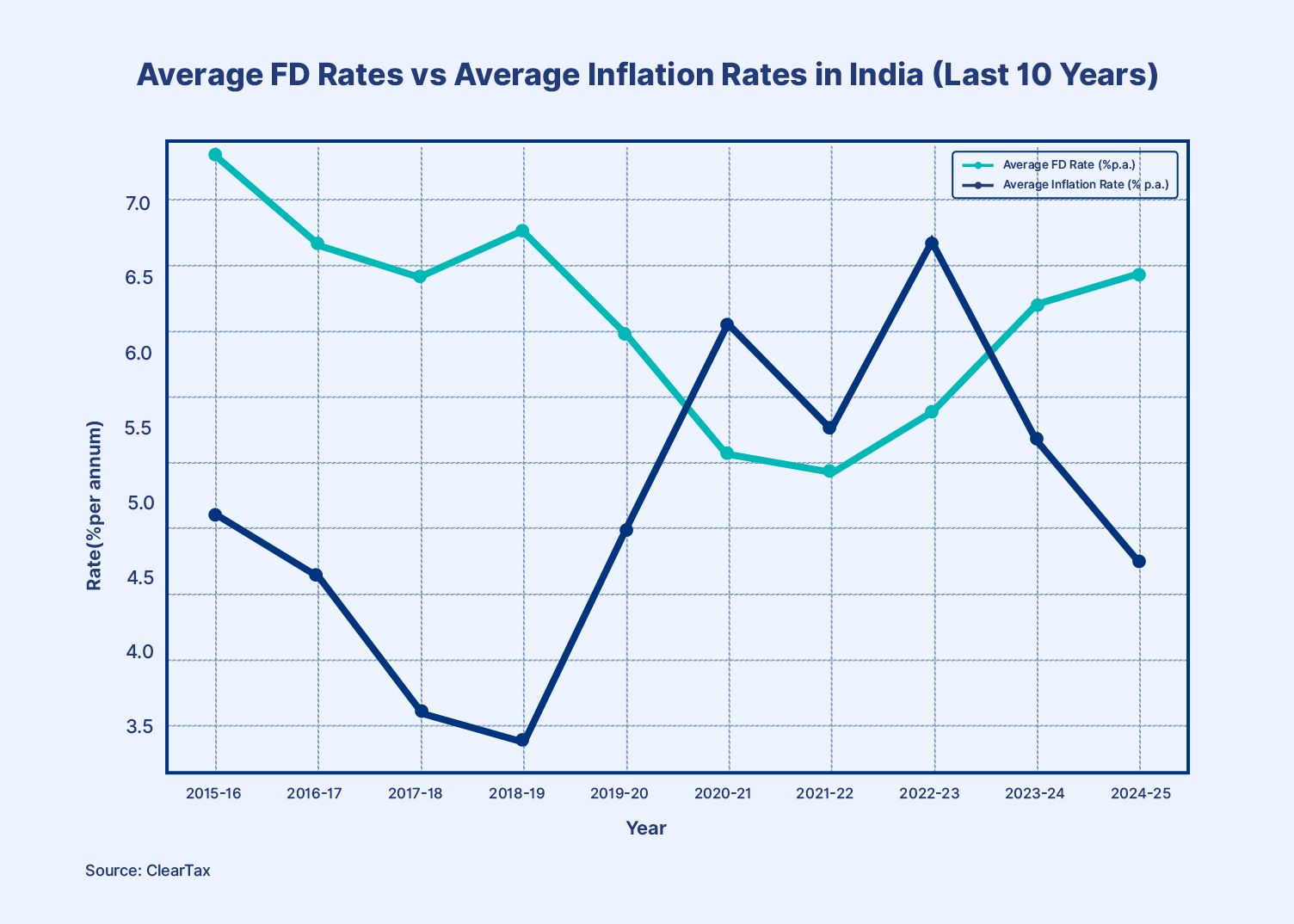

For an FD to be able to generate real returns, it must have an interest rate more than the expected inflation rate. The table and chart below highlight the comparison between the average FD rate and the inflation rate in India over the past 10 years.

| Year | Avg FD Rate (% p.a.) | Avg Inflation Rate (% p.a.) |

| 2024-25 | 6.5 (midpoint) | 4.6 |

| 2023-24 | 6.3 | 5.4 |

| 2022-23 | 5.6 | 6.7 |

| 2021-22 | 5.2 | 5.5 |

| 2020-21 | 5.3 | 6.2 |

| 2019-20 | 6.1 | 4.8 |

| 2018-19 | 6.8 | 3.4 |

| 2017-18 | 6.5 | 3.6 |

| 2016-17 | 6.7 | 4.5 |

| 2015-16 | 7.3 | 4.9 |

Source: BajajFinserv4, ClearTax5

*Figures are averaged

The comparison of historical FD rates and inflation rates shows unclear patterns. Neither has been able to outpace the other consistently. Therefore, before choosing the right FD for you, evaluate it with the current inflation rate.

Income Diversification Strategy

Fixed Deposits deliver fixed, stable, and modest returns. These alone are not enough for an investor looking to get higher returns from their overall portfolio. FDs are suitable for a low-risk investor. However, investors seeking high returns while taking additional risks may consider investing in other asset classes. Yet, allocating a certain percentage of their portfolio in secured FDs can help balance the overall risk.

For instance, an investor may keep a portion of their savings in fixed deposits for predictable income. At the same time, another portion may be invested in diversified fixed-income instruments such as bonds, debt funds, or corporate debt platforms that offer higher yields. Platforms such as Grip Invest offer bonds and debt mutual funds that can help investors create a diversified portfolio.

Conclusion

Fixed Deposits are a stable and secure form of investment that can help create a balance of risk and reward in your portfolio. Many banks offer an additional interest benefit to senior citizens, which increases the INR 10 lakh FD interest for senior citizens compared to standard FD returns. For example, as on March 12, 2026, the regular HDFC Bank’s INR 10 lakh FD interest per month for 5 years comes to 0.51%. For a senior citizen, it is 0.55%. For someone with an INR 10 Lakh corpus, an FD can provide a steady income stream, particularly if the monthly payout option is selected.

FAQs

1. How much interest will INR 10 lakh generate monthly?

On average, Indian banks provide an FD rate of 6% per annum in 2026. Thus, an investment of INR 10 Lakh will generate INR 60,000 each year. The monthly payout comes to INR 5,000.

2. Is a monthly interest FD better than a cumulative FD?

A monthly interest FD generates a steady stream of income that is paid out to the investor each month. This is ideal for investors such as retirees who may seek a monthly income. On the other hand, a cumulative FD accumulates the interest earned on the total amount over the duration of the FD. The total interest is paid as a lump sum at the end of the FD term.

3. Is FD interest taxable?

Yes, the interest earned from fixed deposits is taxable according to the investor’s income tax slab. Banks also deduct tax at source (TDS) if the interest exceeds the prescribed threshold during a financial year.

References:

1. TOI, accessed from: https://timesofindia.indiatimes.com/business/financial-literacy/investing/rural-deposit-boom-fixed-deposits-surge-14-in-villages-metros-lose-momentum-as-savers-shift-to-market-products/articleshow/125910883.cms

2. BankBazaar, accessed from: https://www.bankbazaar.com/fixed-deposit-rate.html

3. FD calculator, accessed from: https://calculators.gripinvest.in/fd-calculator

4. BajajFinserv, accessed from: https://www.bajajfinservmarkets.in/fixed-deposit/what-is-the-history-of-fixed-deposits-through-time

5. ClearTax, accessed from: https://cleartax.in/s/inflation-calculator

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001