Best SWP For Monthly Income: Top Funds And Withdrawal Strategies

SWPs (Systematic Withdrawal Plans) have become quite popular among investors for attaining a consistent monthly income. Besides the investors looking for retirement planning, SWPs are an excellent source of supplementing regular income. However, choosing the appropriate fund is critical to ensure that your objectives are successfully met.

Selecting and finalising the best SWP for monthly income requires understanding how SWPs work, the type of funds suitable for withdrawals, and the factors that can influence the sustainability of cash flows over time. Let us help you in providing information about such funds so that you can make an informed decision.

What Is An SWP And How Does It Work?

An SWP is a facility offered by mutual funds that allows investors to redeem a predetermined amount from their investments at regular intervals, such as monthly, quarterly, or annually. The concept has become quite popular in the past few years as more and more investors use SWP for monthly income to enhance their income and meet recurring expenses without liquidating their investments.

Under the SWP arrangement, the fund automatically sells a given number of units to generate the withdrawal amount. The remaining units remain invested in the fund and participate in the market movements.

The concept is often compared with SIPs (Systematic Investment Plans) where a fixed and predetermined amount is invested each month; here, the difference is that a predetermined amount is withdrawn and the initial investment, generally, is a large lumpsum amount.

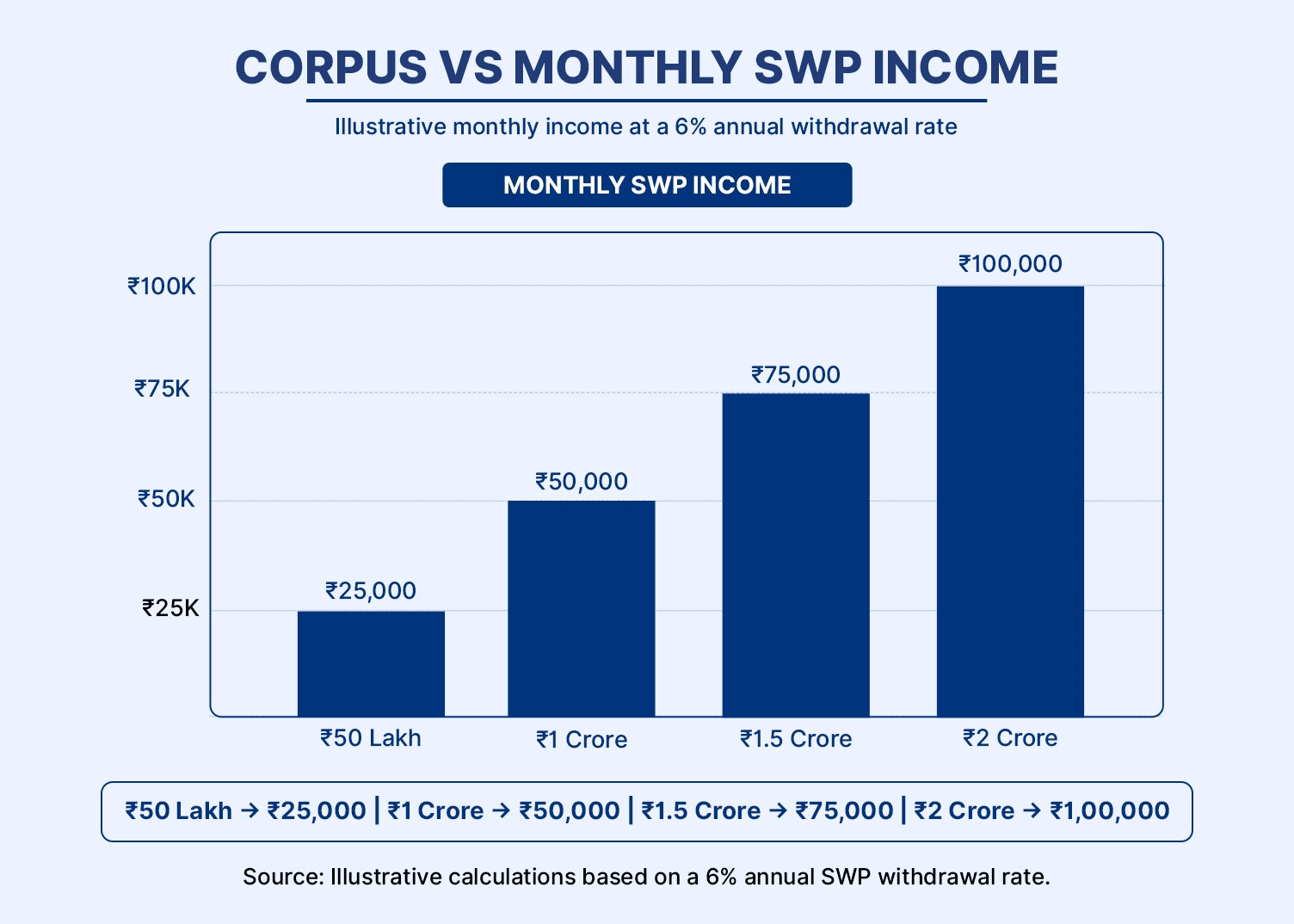

How Much Monthly Income Can You Generate?

The amount you can withdraw depends on the size of your investment corpus, expected returns, and withdrawal rate. In addition, you should also understand that the longevity of your investment will depend on the quality of the underlying assets and prevailing market conditions.

Example Calculation

Suppose an investor has a corpus of INR 50 lakh and withdraws INR 25,000 per month through an SWP. If the fund generates returns that partially offset the withdrawals, the corpus may continue to support income for many years.

You can also use an SWP calculator to evaluate the expected duration of your corpus based on the withdrawal amounts and the market rate of return.

Corpus Required For Different Income Goals

Here is a table that indicates the corpus required for different income goals. Please note that it is an indicative table based on a 6% rate of return on investments.

Best Types Of Funds For SWP

Selecting the right fund is critical for ensuring sustainable withdrawals. There are a wide range of investment alternatives, each having their own pros and cons. Let us assess each option:

1. Conservative Hybrid Funds

Conservative hybrid funds invest primarily in debt instruments with a small allocation to equities. These work extremely well for investors looking for long-term planning such as retirement or meeting recurring expenses. These funds are quite diversified, providing the best of both worlds to the investors.

2. Debt Funds

Debt funds invest in bonds, treasury bills, and other fixed-income securities. For risk averse investors who do not want any exposure to market volatility, can choose debt funds. These are often considered the best mutual fund for SWP, when the objective is to preserve capital and ensure consistent income.

3. Balanced Advantage Funds

Balanced advantage funds dynamically adjust equity and debt allocations based on market conditions. The concept is quite similar to hybrid funds, the difference being the dynamic nature of investing. The investors who can manage to take a bit of risk and wish to achieve a higher return often choose balanced advantage funds.

4. Large-Cap Funds

For investors with a longer investment horizon, large-cap funds can be considered. Although they are more volatile than debt-oriented options, they offer greater growth potential that may help offset withdrawals over time.

Factors To Consider Before Choosing An SWP

SWPs can be an excellent part of your personal financial management but you cannot simply choose any fund for this purpose. For instance, if you go for a pure equity fund, the returns can be quite high during favourable market conditions. This means that your corpus will last for a considerable period and you can attain your monthly goals without any hassles. However, when the market conditions are bearish, this can have an extremely negative impact on the longevity of your corpus.

Here are some factors that you must consider before choosing an SWP:

1. Withdrawal Rate

A withdrawal rate that is too high may deplete the corpus quickly. Investors should aim for sustainable withdrawal levels aligned with expected fund returns.

2. Fund Volatility

Market fluctuations can impact the value of investments. Higher volatility may reduce the effectiveness of an SWP during prolonged market downturns.

3. Taxation

Tax treatment depends on the type of mutual fund and the holding period. Investors should understand applicable capital gains taxes before starting an SWP.

4. Investment Horizon

The investment horizon should align with income requirements. For example, if you are looking for a retirement income SWP, you should choose an option that provides consistent returns (such as debt funds or a hybrid fund rather than a pure equity fund) as it will help in generating consistent returns for decades.

SWP vs FD For Monthly Income

Many investors compare swp vs fd when evaluating regular income options. Here is a comparative table that can help you take an informed decision:

Parameter | SWP | Fixed Deposit |

Tax Efficiency | Capital gains taxation may be more efficient in certain situations | Interest is taxed according to the investor's tax slab |

Flexibility | Withdrawal amount and frequency can be customised | Limited flexibility |

Return Potential | Market-linked and potentially higher | Fixed and predictable |

Risk | Subject to market risk | Lower risk |

Whereas FDs are quite popular because of their reliability and the ability to offer consistent returns, investors can go for SWPs if they are willing to take an extra bit of risk for a higher ROI. In addition, investors looking for a sustainable retirement cash flow, may find SWPs extremely attractive as in the long-term, these options tend to provide a higher return than fixed deposits.

Conclusion

SWPs can be an excellent strategy and an integral part of your personal finance journey. With SWPs, you can remain invested in a fund scheme while deriving consistent income. This works extremely well for retirement planning. However, there are various factors such as the category of fund chosen, the investment strategy, and horizon along with tax implications, which you must consider before starting your SWP journey.

FAQs On SWP

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001