How To Invest In SWP: A Step By Step Guide To Systematic Withdrawal Plans

There are a lot of people out there who have a vision of being able to get a steady stream of income from their investments without having to cash in on all of them at once. One of the smartest and easiest ways to accomplish this is by using a systematic withdrawal plan (SWP).

It has become very popular with retirees as well as those looking for a way to generate a steady cash flow.

By allowing your money to grow at the same time that you withdraw a predetermined amount on a set schedule, SWPs offer a good balance to your retirement needs. They can provide you with a reliable source of income while also giving you peace of mind throughout your retirement years.

We'll break it down step by step as to how you can start a SWP mutual fund with clarity and show you how you can make an informed decision about whether or not it meets your needs.

Why Is SWP Popular For Retirement And Passive Income?

Reliable sources of income are generally necessary after retirement or during a semi-retirement lifestyle. While fixed deposits offer safety, they may not be able to keep up with inflation over time. SWPs combine the advantages of market growth and periodic cash flow through regular withdrawals.

1. Provides regular cash flow after retirement

SWPs can offer a steady source of income, which can help cover daily living expenses during retirement or semi-retirement.

2. Balances growth with withdrawals

Unlike fixed deposits, SWPs allow the remaining invested amount to stay in the market and potentially grow over time.

3. May help manage inflation better

Since investments remain market-linked, SWPs can offer better long-term growth potential compared to traditional fixed-income options that may struggle to beat inflation.

4. Supports financial flexibility

Investors can withdraw money periodically while keeping the rest of their corpus invested.

5. Useful for multiple life goals

SWPs can help manage routine household expenses, medical costs, or even education-related expenses without liquidating the full investment.

6. Can create passive income

This mix of periodic withdrawals and continued investment growth makes SWPs a commonly considered option for retirement and passive income planning.

What Is SWP And How Does It Work?

Systematic withdrawal plans allow you to take a fixed amount of money from your mutual fund on a set schedule. Withdrawals can be made monthly, quarterly, or annually. When a withdrawal occurs, the fund will redeem a number of units to provide you with that amount of money while the balance remains in the fund.

A systematic withdrawal plan steps are the reverse of a systematic investment plan (SIP). With an SIP, you invest regularly, whereas with an SWP, you pull money out at regular intervals. By continuing to invest after taking withdrawals, you can extend the length of time that you will have money in the account, and potentially even grow your account value, despite making regular withdrawals from it.

For Example

Priya has developed a corpus of INR 50 lakh in a mutual fund. She puts in an SWP of INR 20,000 each month. Each month, the fund sells units worth INR 20,000 based on its current NAV in order to provide Priya with her monthly withdrawal.

The remaining amount will continue to be invested in the fund, and Priya will benefit from growth on her remaining investment due to recouping her no longer needed portion of the original investment.

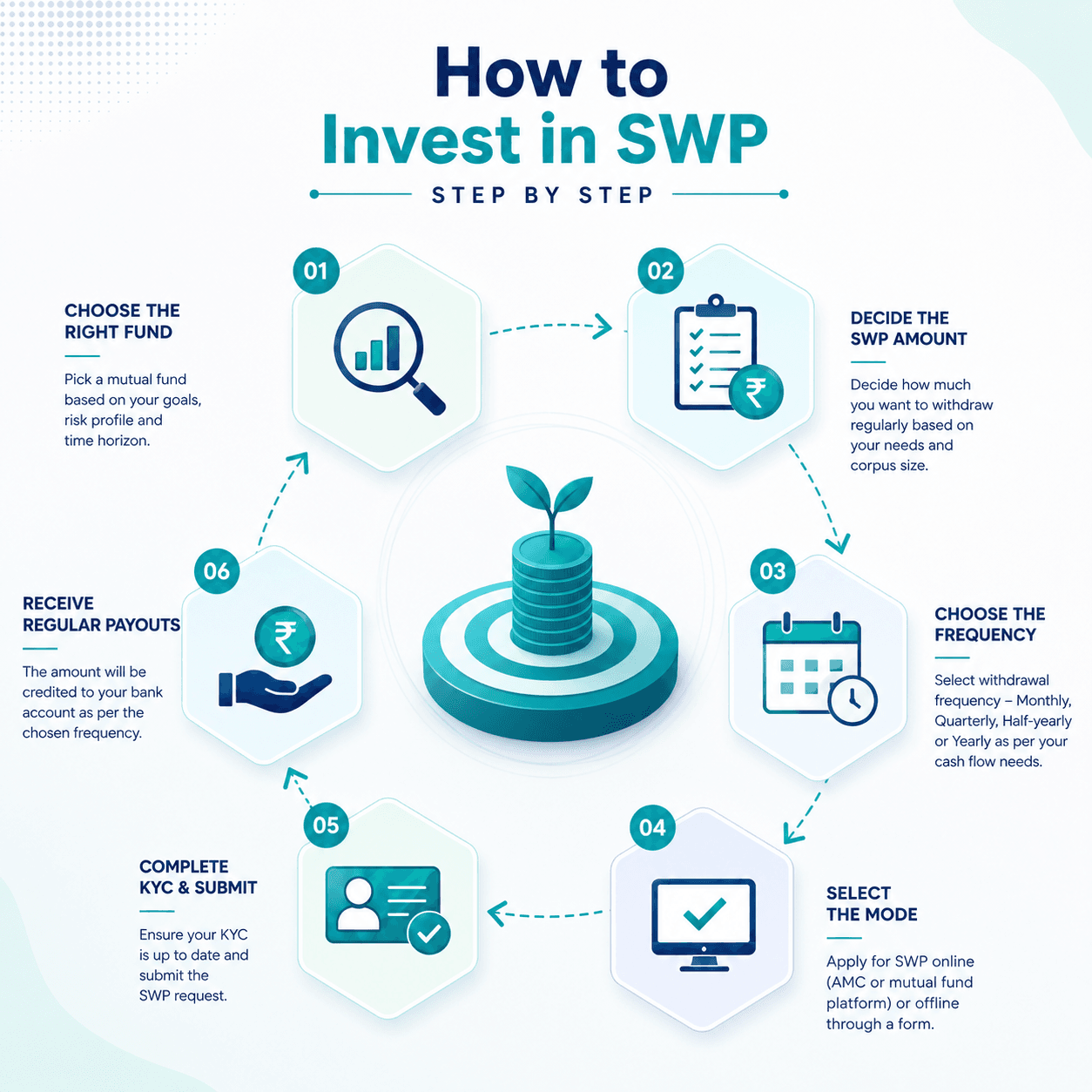

Step By Step: How To Invest In SWP

Setting up a systematic withdrawal plan (SWP) is a simple process if you understand the process.

To ensure you have a good experience with your SWP, please follow these steps carefully.

1. Choose the Right Fund:

To find the right mutual fund for your SWP, you must first determine your risk tolerance and income needs. There are three types of mutual funds you can choose from:

- Equity Mutual Funds: Generally have the potential for high growth but have high volatility.

- Balanced (or Hybrid) Mutual Funds: These types of funds provide a balance between risk and reward; they are usually composed of both stocks and bonds.

- Debt Funds: These types of funds are usually used to provide a conservative investment with less risk and moderate growth.

2. Set Withdrawal Amount and Frequency

You will also need to determine how much you will withdraw and when. Most mutual fund companies allow you to withdraw either monthly (12 withdrawals), quarterly (4 withdrawals) or annually (1 withdrawal). You may find that a good rule of thumb is to withdraw 4% to 6% of your total investment account balance as an SWP annually.

3. Online versus Offline Process

Most people are now accustomed to using the internet for all of their transactions. You can do so by simply going to your mutual fund company's website or by logging into your investment application and selecting SWP from the list of options on your account page.

At this time, you will need to identify the amount of money you want to withdraw, the frequency at which you would like to withdraw it, and the date you would like to begin withdrawing your SWP.

The traditional approach (offline) involves filling out a paper-based application form and handing it in to an advisor or branch. The online method (online) has faster processing times and offers better options for subsequent modifications.

Thus, investing through an SWP will be relatively easy via digital platforms, as most people can complete their entire investment in under five minutes from the comfort of their own home.

Best Fund Categories For SWP

The best types of SWP funds will depend on the investor's needs:

| Fund category | Best suited for | Risk level | Return potential | Why it may work for SWP |

| Equity Funds | Risk-tolerant investors with a long investment horizon | High | High | Offers strong long-term growth potential, but short-term fluctuations can affect SWP stability. |

| Hybrid Funds | Investors seeking a balance between growth and stability | Moderate | Moderate to high | Combines equity and debt, making it useful for investors who want a middle ground for SWP. |

| Debt Funds | Conservative investors who want predictable income and capital stability | Low | Low to moderate | Provides lower volatility and more stable payouts, which can support regular SWP withdrawals. |

| Balanced Advantage Funds | Middle-aged and senior investors looking for a more flexible SWP option | Moderate | Moderate | Dynamically shifts between equity and debt, offering a balance of growth and downside protection. |

When selecting an SWP fund to use, one should consider their age, level of risk tolerance, and financial goals. Many middle-aged and senior-aged investors who are looking for the best fund for SWP will likely find that either a well-managed hybrid fund or a balanced advantage fund provides them with the best opportunity to achieve their investment goals.

Also read on How SWP works In Mutual Fund

Common Mistakes To Avoid

When creating a Systematic Withdrawal Plan (SWP), there will likely be some beginner errors you will encounter while setting up your SWP.

- Withdrawing too early is a fast way to diminish your investments.

- If you do not consider the current market, your investments at that time may have a bearing on how your investments will perform over time.

- Not reviewing your plan annually will cause you to not have enough money to meet your income needs.

- Investing in very aggressive funds when you need money markets for income will add undue stress to your life.

- If you do not take the time to consider the tax implications of your withdrawals, you will lose part of your invested amount to taxes.

Doing a periodic review and making any adjustments based on your current circumstances will ensure your SWP is on track.

SWP Tax Treatment

There are different taxation rules for an SWP withdrawal based on your fund type, such as the amount of time you held the fund. You will only be taxed on the capital gains portion of the withdrawal. You will withdraw your original investment amount without being taxed.

For a long-term capital gain on a long-held equity fund, the applicable long-term capital gains tax would apply, but there would be an exemption limit on the amount over which you would pay tax.

For a debt fund, you would be taxed at your respective tax bracket depending upon the holding period; therefore, if you hold your investments in SWP, you may find that they can be a more tax-efficient source of income than fixed-deposit accounts. Make sure you speak with your tax professional to understand your specific situation and keep good records.

Should You Invest?

The SWP Investment Guide will help you establish indefinite income sources; nevertheless, it also has the inherent market risk associated with it and should only be implemented after you assess your whole financial position.

If you want predictable income sources that provide you with lower volatility, bonds can provide a better alternative than SWP and will add stability to your retirement portfolio.

Once you have achieved a sufficient corpus and built an emergency fund, you may want to create a systematic withdrawal plan through a mutual fund. When you set the SWP, you will obtain greater results than if you did not prepare ahead of time.

To effectively create a successful SWP requires a great deal of patience and an understanding of your cash flow needs. An appropriate SWP investment guide can assist you in living your lifestyle comfortably.

Also read on Is SWP Return better than FD Interest?

Conclusion

A Systematic Withdrawal Plan (SWP) offers retirees and long-term investors a flexible and disciplined way to generate regular income while keeping their investments working for future growth. The ability to start, stop, or modify withdrawals anytime makes SWPs highly adaptable to changing financial needs and lifestyle goals. Investors can also align their withdrawals with inflation and combine SWPs with other income sources such as pensions, rental income, or fixed-income investments to create a more stable retirement strategy.

With digital investment platforms making SWP tracking and management easier than ever, more Indian families are now including SWPs as an essential part of long-term financial planning. However, building a sustainable withdrawal strategy requires careful planning, proper asset allocation, and an understanding of market risks.

To strengthen your retirement planning further, explore diversified fixed-income opportunities, bonds, and alternative investment options with Grip Invest and build a smarter, more predictable passive income portfolio for the future.

FAQs On How To Invest In SWP

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001