SWP in Mutual Funds: Create Regular Income While Growing Your Wealth

Most investors know how SIPs (Systematic Investment Plans) help in disciplined wealth creation by investing small amounts regularly in mutual funds. But wealth creation is only one part of the journey—what about when you need to use that money? That’s where a Systematic Withdrawal Plan (SWP) in India comes in. An SWP allows you to withdraw a fixed amount from your mutual fund investments at regular intervals, creating a steady income stream while keeping the rest of your money invested.

In this article, we’ll explain what an SWP is, how it works, its benefits, tax implications, and how you can use it to plan your post-retirement cash flow or other financial goals.

Introduction To SWP In Mutual Fund

Definition: Systematic Withdrawal Plan

A SWP in mutual fund is a facility offered by mutual funds that allows investors to withdraw a fixed amount from their investments at predetermined intervals. It works as the opposite of a Systematic Investment Plan. While SIP helps you invest regularly, SWP helps you withdraw systematically.

How SWP Helps Investors Generate Regular Income

SWP transforms your lump sum investment into a regular income stream while keeping the remaining corpus invested in the market. This approach is particularly beneficial for retirees, individuals with irregular income patterns, or those looking to supplement their regular income. It is a mutual fund withdrawal strategy that provides financial discipline and helps manage cash flow needs effectively.

How SWP Works

Step-by-Step Example: Withdrawing Monthly from a Mutual Fund

When you initiate an SWP, you instruct the fund house to redeem a fixed number of units or a specific amount at regular intervals from your mutual fund investment.

For example, imagine you have invested INR 10 lakhs in a balanced mutual fund and need INR 20,000 monthly to cover your expenses. Here’s how the SWP would work:

- You set up an SWP for INR 20,000 per month from your mutual fund

- On the predetermined date each month, the fund house calculates the number of units equivalent to INR 20,000 based on that day’s Net Asset Value (NAV)

- These units are redeemed, and the proceeds are transferred to your registered bank account

- The remaining units continue to stay invested and participate in market movements

Difference Between SWP And Dividends

The key difference between SWP vs dividends is consistency and control. With dividends (now known as Income Distribution cum Capital Withdrawal or IDCW), payouts depend on the fund’s performance and the fund manager’s discretion. However, with SWP, you decide the amount and frequency, ensuring predictable cash flow regardless of market conditions.

Additionally, SWP tax implications are more efficient than dividend options, as only the capital gain component is taxable, not the entire withdrawal amount, as in the case of dividends.

Benefits And Risks Of SWP

A Systematic Withdrawal Plan offers the dual advantage of steady income and continued market participation. However, like any investment strategy, it comes with risks such as market volatility and potential capital erosion. Let us understand what are those

Benefits of SWP

1. Regular Cash Flow: SWP provides a steady stream of income at predetermined intervals, helping you manage your finances better.

2. Tax Efficiency: SWPs can be more tax-efficient than dividend options. In equity funds, long-term capital gains up to INR 1.25 lakhs per year are tax-free (as of FY 2025-26).

3. Flexibility: You can customise the withdrawal amount, frequency (monthly, quarterly, or annually), and duration based on your needs.

4. Potential for Capital Appreciation: The remaining investment continues to grow as per market conditions, potentially offsetting some of the withdrawal impact.

5. Liquidity: You can modify or terminate the SWP facility at any time without penalties, except applicable exit loads.

Read: Personal Finance Management in India: A 2026 Guide to Smarter Money Habits

Risks: Capital Erosion If Market Underperforms

1. Capital Erosion Risk: If market returns are lower than your withdrawal rate, your capital may deplete faster than expected. For instance, if your fund generates an 8% annual return but you are withdrawing at a rate of 10%, your corpus will gradually diminish.

2. Market Volatility Impact: During market downturns, more units need to be redeemed to maintain the same withdrawal amount, potentially accelerating corpus depletion.

3. Exit Load and Tax Implications: Frequent withdrawals may trigger exit loads (if applicable) and result in tax liabilities, reducing your effective returns.

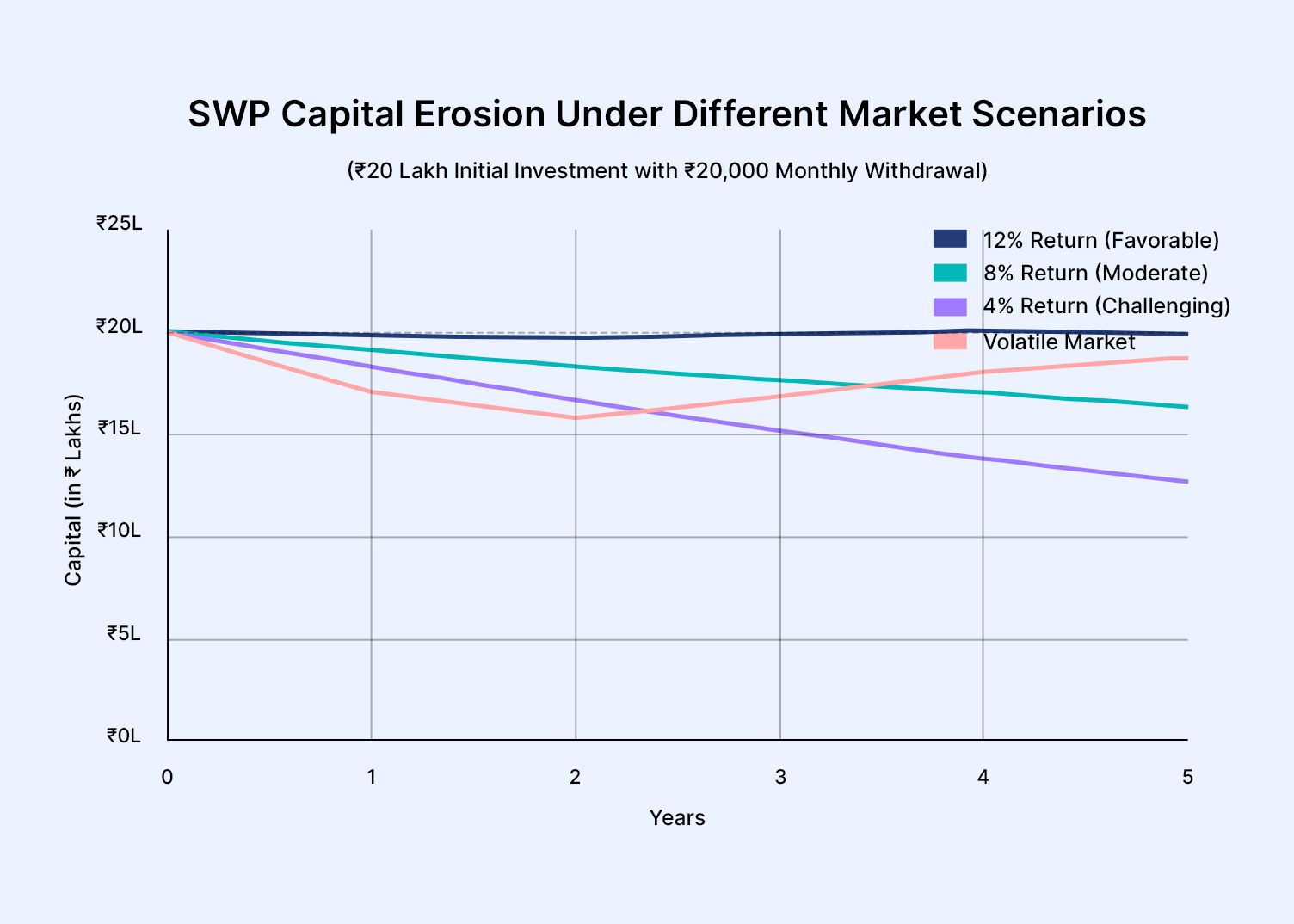

This chart shows how your INR 20 lakh investment performs over 5 years with INR 20,000 monthly SWP in mutual funds under different market conditions.

The green line (12% returns) shows your capital remains stable despite withdrawals, while the blue (8%) and orange (4%) lines reveal increasing capital erosion as returns fall below withdrawal rates. The purple line illustrates how market volatility creates a U-shaped capital curve, with initial erosion followed by recovery as returns improve.

Each scenario highlights why aligning withdrawal rates with realistic market expectations is crucial for sustainable income.

Read: Corporate Bonds in India: Meaning, Types, Benefits & SEBI Guidelines (2026 Guide)

Planning Your SWP With Bond Portfolios

An effective SWP strategy should balance growth potential with income stability. While mutual funds provide the growth component, incorporating fixed-income instruments can enhance predictability during market volatility. Consider allocating 15-20% of your portfolio to bonds based on your goals and risk appetite to bonds for regular income.

Corporate bonds available on Grip offer fixed returns with defined maturity dates. They can act as a stable income cushion when equity markets underperform, reducing pressure on your mutual fund corpus and lowering sequence-of-returns risk.

For example, you could set up an SWP from an equity mutual fund for long-term income needs while investing in bonds available on Grip with 2–3 year maturities for more immediate, predictable returns. This balanced approach creates a steadier and more reliable income strategy.

Conclusion

A Systematic Withdrawal Plan (SWP) is a powerful tool for turning your mutual fund investments into a steady income stream, especially during retirement or for long-term financial goals. By withdrawing fixed amounts at regular intervals, you can enjoy consistent cash flow while the remaining corpus continues to grow in the market.

This approach helps balance your need for liquidity with the potential for wealth creation. For investors looking to further stabilize their income, combining an SWP with fixed-income options like bonds available on Grip Invest can provide added predictability and peace of mind.

FAQs On SWP In Mutual Funds

1. How is SWP different from SIP?

A Systematic Investment Plan involves investing a fixed amount regularly into mutual funds to build wealth over time. In contrast, a Systematic Withdrawal Plan allows you to withdraw a predetermined amount at regular intervals from your existing mutual fund investment.

2. Is SWP taxable in India?

Yes, withdrawals through SWP are subject to capital gains tax in India. For equity mutual funds, long-term capital gains (investments held for more than 1 year) exceeding INR 1.25 lakhs per annum are taxed at 10% without indexation benefits. a

3. Which mutual funds are best suited for SWP?

The ideal mutual funds for SWP depend on your income needs, risk tolerance, and investment horizon. Conservative investors can consider debt funds and hybrid funds for stability, while moderate risk-takers can opt for balanced advantage funds that adjust allocations dynamically. For long-term income needs, equity funds with consistent track records offer growth potential alongside withdrawals. Regardless of choice, ensure your withdrawal rate remains below the fund's expected returns to prevent premature capital erosion.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001