Capital Expenditure Vs Revenue Expenditure: Key Differences And Examples

Introduction To Capital Expenditure Vs Revenue Expenditure

When analysing a company’s financial statements, one question smart investors always ask is simple: Where is the money going? Every business spends money but at the same time we cannot say that all spending serves the same purpose. Some expenses are made to build the future, while others are necessary to run the present. Understanding the difference that helps investors, founders, and finance professionals decode a company’s true priorities, performance, and growth direction.

These differences help to measure the profitability of how cash flows are managed, how taxes are planned, and how a company is valued in the market. It’s not just an accounting concept—it is a strategic process for reading financial statements more intelligently.

In this blog, we break down how business spending works, why it matters, and how it influences long-term success—before clearly explaining capital expenditure and revenue expenditure in the next sections of this blog.

What Is Capital Expenditure (CapEx)?

Now that we understand why it is necessary to understand the spending patterns matter, let’s begin with capital expenditure. Capital Expenditure, also known as CapEx, refers to the money a company invests in acquiring, upgrading, or improving long-term assets that will benefit the business for several years.It is a strategic investment aimed at expanding capacity, improving efficiency, or supporting future growth. Instead of being fully recorded as an expense in the same year, it is shown as an asset on the balance sheet and depreciated over time.

It can be said that,

Capital expenditure = Investment in assets for long-term business growth.

For example, purchasing machinery, constructing a building, buying land, or investing in software systems are common examples of capital expenditure because they provide long-term value to the business.

List of Capital Expenditure (CapEx)

- Purchase of land

- Construction of buildings or factories

- Purchase of machinery and equipment

- Buying vehicles for business use

- Installation of plant and production units

- Investment in software systems and IT infrastructure

- Major upgrades or improvements to existing assets

- Purchase of furniture and fixtures for long-term use

- Acquisition of patents or licenses

- Expansion of office or production facilities

What Is Revenue Expenditure?

Revenue expenditure refers to the regular, day-to-day expenses a company incurs to run its normal operations. These costs are short-term in nature and are used up within the same accounting period. Examples include salaries, rent, electricity bills, repairs, maintenance, and advertising expenses. Unlike capital expenditure, revenue expenditure does not create long-term assets or provide benefits beyond the current year. It is fully recorded as an expense in the income statement when incurred.

For example, if a company pays monthly office rent or spends money on a marketing campaign, it is treated as revenue expenditure because the benefit is limited to the current period.

It can be said that,

Revenue expenditure = Daily operational spending to run the business

List of Revenue Expenditure

- Salaries and wages

- Rent payments

- Electricity and utility bills

- Repairs and routine maintenance

- Office supplies and stationery

- Advertising and marketing expenses

- Insurance premiums

- Telephone and internet charges

- Transportation and fuel expenses

- Printing and administrative expenses

Key Differences

Understanding the distinction between capital expenditure and revenue expenditure becomes much clearer when the two are compared side by side.

Below is a structured comparison to highlight the key differences:

| Basis of Comparison | Capital Expenditure (CapEx) | Revenue Expenditure |

| Purpose | To acquire or upgrade long-term assets | To maintain day-to-day business operations |

| Time Benefit | Provides benefits for multiple years | Benefits are consumed within one accounting period |

| Accounting Treatment | Capitalised and shown on the balance sheet | Fully expensed in the income statement |

| Impact on Profit | Depreciated over time, reducing profit gradually | Reduces profit immediately in the same year |

| Nature | Investment-oriented | Operational-oriented |

| Frequency | Usually non-recurring or irregular | Recurring and frequent |

This table comparison clearly shows that while both expenditures are essential, they serve different strategic and financial purposes within an organisation.

Impact On Financial Statements

Building on the discussion of capital and revenue expenditure, their real difference becomes more evident when analysing how they appear in financial statements. Their impact can be clearly understood as follows:

Impact of Revenue Expenditure

Revenue expenditure, on the other hand, is fully recorded as an expense in the income statement during the same accounting period.

This means:

- It immediately reduces net profit.

- It does not create a long-term asset on the balance sheet.

- In the cash flow statement, it appears under operating activities.

Impact of Capital Expenditure (CapEx)

When a company incurs capital expenditure, the amount is not immediately recorded as a full expense. Instead, it is capitalised and shown as an asset on the balance sheet. Over time, the asset’s cost is allocated through depreciation (for tangible assets) or amortisation (for intangible assets).

This means:

- The balance sheet shows an increase in assets.

- The income statement reflects a gradual depreciation expense each year.

- Profit reduces slowly over the asset’s useful life rather than all at once.

- In the cash flow statement, it appears under investing activities.

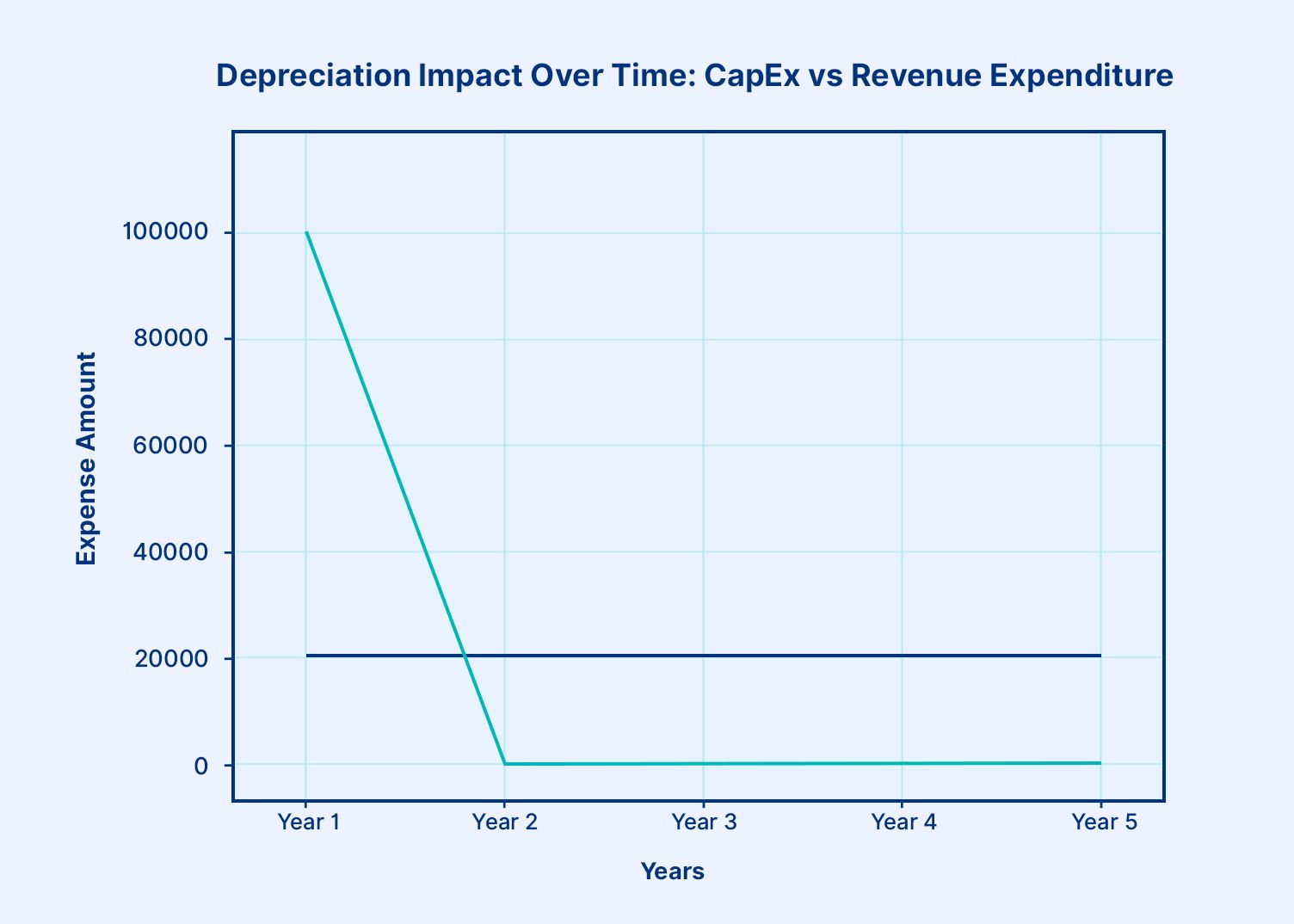

Lets understand this in a graph format.

You can see the graph illustrating the depreciation impact over time-

- CapEx is spread evenly across 5 years through depreciation.

- Revenue expenditure is recorded fully in Year 1, creating a sharp spike, with no impact in later years.

Conclusion

As we conclude, the difference between capital expenditure and revenue expenditure goes beyond accounting terminology—it reveals how a company plans, grows, and sustains itself. Capital expenditure reflects long-term vision and expansion, while revenue expenditure highlights operational efficiency and stability. Understanding their financial impact helps investors analyse profitability, cash flow, and overall business health more effectively. Developing a strong grip on investment concepts like CapEx and revenue expenditure enhances financial awareness and strategic thinking. Grip Invest on investment knowledge empowers investors to make smarter decisions, interpret financial statements confidently, and better evaluate a company’s true long-term potential.

FAQs

1. What is capital expenditure with example?

Capital expenditure (CapEx) is money spent on long-term assets that support future growth. Example: purchasing machinery, land, or setting up a factory. It is recorded as an asset in the financial statement and depreciated over time.

2. Is salary capital or revenue expenditure?

Salary is a revenue expenditure because it is paid for daily operations. However, if paid for asset construction work, it is treated as capital expenditure.

3. How does CapEx affect profit?

CapEx does not reduce profit immediately. It impacts profit gradually through depreciation, unlike revenue expenditure which directly reduces profit in the same year.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001