Government Bond Index Explained: Types, Benefits And Risks

A government bond index tracks the performance of a defined basket of sovereign securities. It acts as a bond index benchmark for funds and investors comparing returns against a rules-based market measure.

The term government bond index emerging markets may sound technical, but it now has direct relevance as eligible Indian government securities entered J.P. Morgan’s GBI-EM series in June 2024, Bloomberg’s emerging-market local-currency index from January 2025 and FTSE Russell’s EM government bond index from September 2025.1 India’s sovereign debt market is now more closely linked with global fund flows.

However, entry into these indices does not depend on economic growth alone. Index providers also assess different criteria. FTSE Russell, for example, requires countries to meet a defined market-accessibility level before inclusion. India moved from Level 0 to Level 1 before joining the index.2

These requirements matter because inclusion can influence actual investment flows. Foreign investors purchased a record USD 3 billion of Indian FAR government bonds in June 2026.3

India is one part of a much wider emerging-market universe. Major bond indices also cover economies across different regions:

Region | Countries to highlight |

Asia | India, China, Indonesia, Malaysia, the Philippines, Thailand |

Latin America | Brazil, Mexico, Colombia, Chile, Peru |

Europe | Poland, Hungary, Romania, Czechia |

Middle East and Africa | Saudi Arabia, South Africa, Egypt, Türkiye |

The exact country mix differs across providers. To understand why one market receives a higher weight than another, it is necessary to look at how these indices select, rank and rebalance bonds.

How Does An Emerging Market Government Bond Index Work?

An EM bond index follows a set of rules to decide which countries and securities qualify. These rules also determine how much weight each market receives and when the composition changes.

The main factors include:

- Eligibility criteria: Index providers assess the issuer type, coupon structure, minimum amount outstanding, remaining maturity, pricing availability and foreign-investor access. The FTSE EMGBI, for instance, tracks 17 local-currency, fixed-rate government bond markets and rebalances monthly.4

- Weight allocation: Most indices begin with market value. Countries with a larger pool of eligible debt may therefore receive a higher allocation. Diversified versions usually apply caps to reduce concentration. For example, the J.P. Morgan GBI-EM Global Diversified has a maximum country weight of 10%.5

- Phased inclusion: New markets are often added gradually to limit sudden portfolio shifts. For example,Bloomberg included Indian FAR bonds at 10% of their full market value in January 2025. It then raised the inclusion factor by 10 percentage points each month until October. Bloomberg estimated that 34 Indian securities would account for 7.26% of the uncapped index and reach 10% in the capped version.6

- Rebalancing: The index is reviewed periodically to account for new issuance, bond maturities and changes in eligibility. This process can alter country weights, yields and index duration, even when the benchmark name remains unchanged.

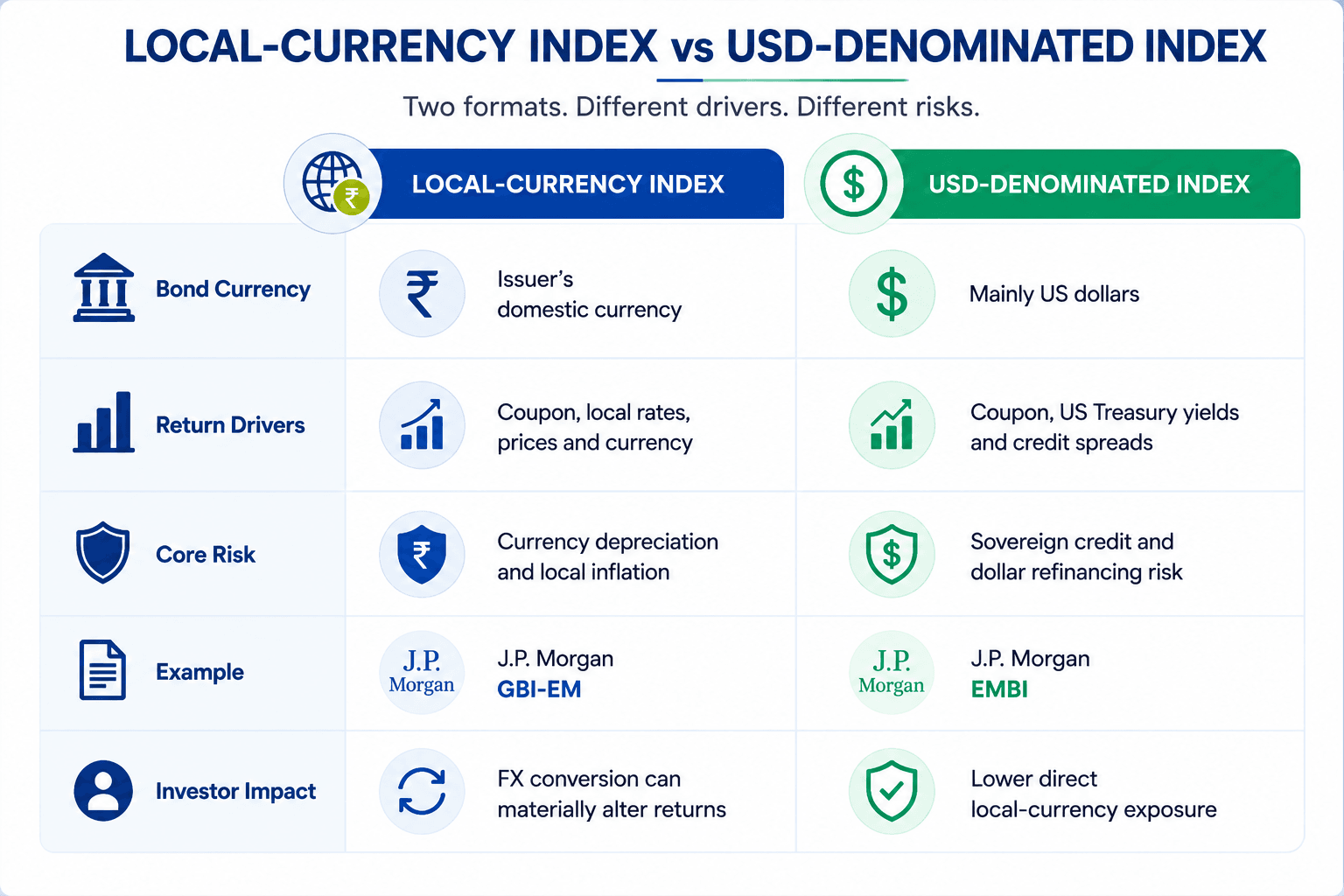

Currency denomination is another important distinction. Some indices track bonds issued in domestic currencies, while others focus on US dollar-denominated debt. The following table shows how these two formats differ.

Metric | Local-currency index | USD-denominated index |

Bond currency | Issuer’s domestic currency | Mainly US dollars |

Return drivers | Coupon, local rates, prices and currency | Coupon, US Treasury yields and credit spreads |

Core risk | Currency depreciation and local inflation | Sovereign credit and dollar refinancing risk |

Example | J.P. Morgan GBI-EM | J.P. Morgan EMBI |

Investor impact | FX conversion can materially alter returns | Lower direct local-currency exposure |

These differences shape both return potential and risk. The next section examines the main benefits and limitations of investing through emerging-market bond indices.

Benefits And Risks Of Investing Through Emerging Market Bond Indices

The structure offers diversification, but investors need to view the advantages beside the risks.

Emerging market government bonds provide exposure to different inflation cycles, policy rates and economic conditions. Emerging East Asia’s local-currency bond market reached USD 31.5 trillion in Q1 2026, increasing 2.4% from the previous quarter.7 Government issuance drove much of the expansion.

A rules-based index also reduces dependence on selecting individual sovereign securities. As a benchmark for debt funds, it helps investors compare returns, duration and country exposure.

However, headline yield is not total return. The IMF found that currency performance had often weakened returns from emerging-market local-currency debt. It placed government debt across emerging and developing economies near USD 30 trillion in 2024, or nearly USD 12 trillion excluding China, with median debt close to 60% of GDP.8

The main trade-offs include:

- Income potential: Sovereign bond yields may exceed developed-market levels, but inflation can reduce real returns.

- Diversification: Country exposure can spread rate risk, although several markets may sit near the index cap.

- Currency risk: A 7% local return can turn negative if the currency falls by more than the income earned.

- Rate sensitivity: Longer index duration usually causes larger price movements when yields change.

- Liquidity risk: Emerging East Asia’s average government-bond bid–ask spread widened from 5.9 basis points in February 2026 to 6.8 basis points in March.9 This illustrates how trading costs can rise during uncertain market conditions.

India’s January 2026 experience shows this sensitivity. When Bloomberg deferred Indian bond inclusion in its Global Aggregate Index, the 10-year government yield rose by as much as six basis points to 6.64%.10

What Should Investors Evaluate Before Using These Indices?

The index label alone is not enough. Investors should examine the underlying risks and their fit with personal goals.

Credit quality indicates a government’s ability to service debt, but ratings can vary widely within one index. Inflation matters because rising prices may prompt rate increases and lower bond prices. Currency movements can add to returns or erase coupon income.

Country concentration also needs attention. A diversified label does not guarantee equal weights. The investment horizon should also match the index duration, especially when longer-dated bonds face larger price swings.

7 Questions To Ask Before Investing In Emerging Market Bonds

- Is the index investment grade, high yield or a mix?

- Does it hold local-currency debt, hard-currency debt or both?

- What are the weights of its five largest countries?

- Are inflation and policy rates rising or easing?

- How have currency movements affected past returns?

- What is the index duration and sensitivity to yield changes?

- Does the fund track the index closely after fees, taxes and hedging costs?

Building A Diversified Fixed Income Portfolio

The final question is where global bond indices fit within a broader fixed-income allocation.

International sovereign exposure can add geographical and currency diversification. However, it should not replace emergency savings, domestic government securities or carefully selected corporate debt. Indian investors can spread maturities and issuer exposure across short-term instruments, G-Secs and corporate bonds rather than relying on one overseas index.

Corporate bonds can offer defined coupons and maturity dates, but they carry issuer credit and liquidity risk. Investors should compare the rating, yield to maturity, security cover, repayment structure and tenure.

Grip Invest provides access to curated fixed-income opportunities, including corporate bonds, that can complement sovereign exposure. A balanced fixed-income sleeve should combine suitable credit quality, manageable duration and staggered maturities, while keeping global bond indices as one allocation rather than the entire portfolio.

FAQs On Government Bond Index

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001