How To Invest In Government Bonds In India: A Step-By-Step Guide For 2026

When we talk about risk-free investments that are not only secure but also provide a consistent return, government bonds often come to the forefront. These bonds are an excellent addition to your portfolio, especially if you are looking to add a bit of diversification without taking too many risks.

However, as an investor, you might ask the logical question: how to invest in government bonds and whether it is worth investing in them when there are so many other alternatives available.

You might also wonder if investing in government bonds is possible through digital platforms or if the investment is still carried out through conventional modes. Before diving into the specifics about the government securities, let us find out how these have performed against some other ‘safer’ investment options, such as Fixed Deposits and Corporate Bonds.

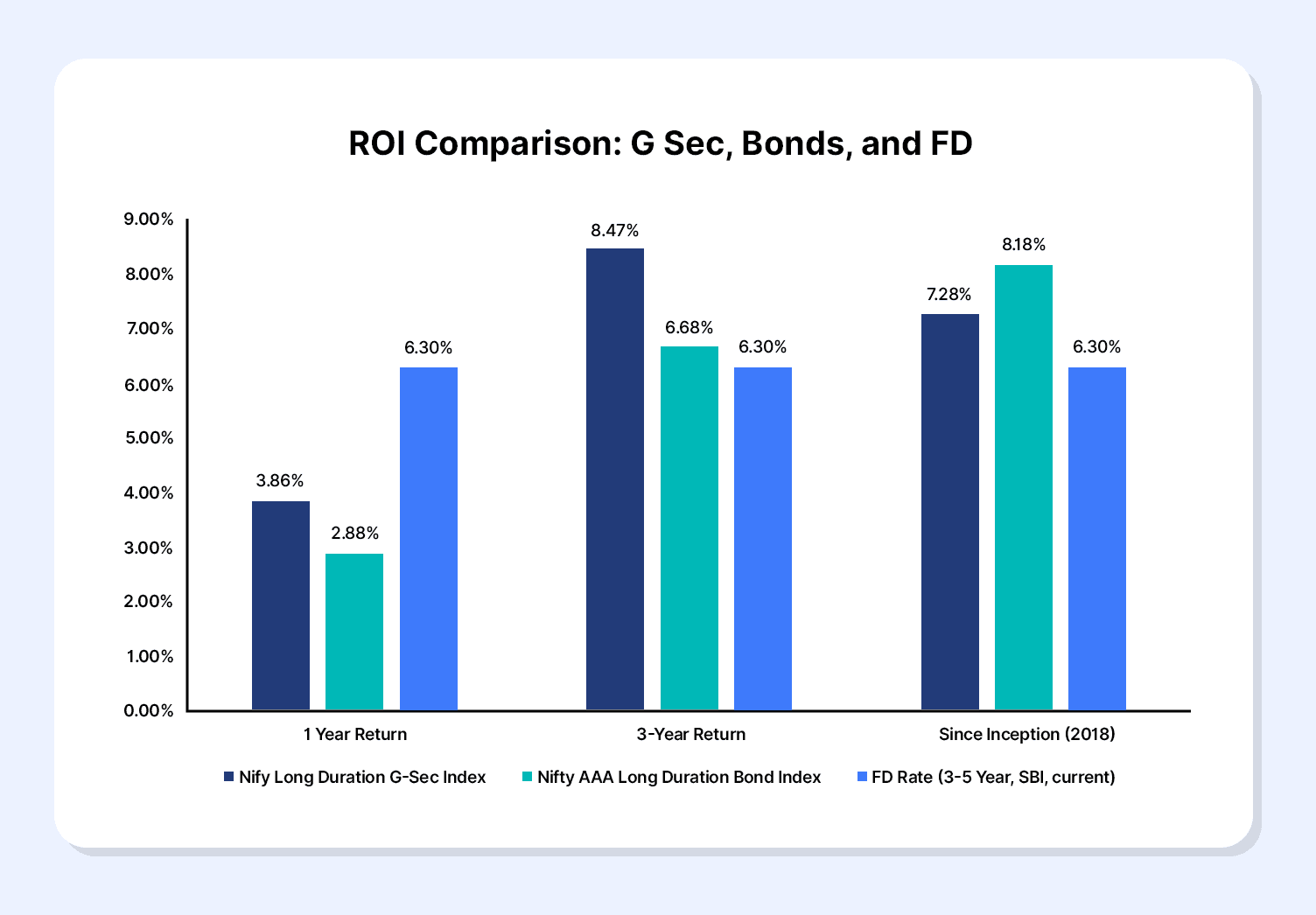

Figure 1.0: Performance comparison: G-Secs vs FD vs corporate bonds

G Secs or government bond yield India information is derived from the NIFTY All Duration G-Sec Index. Corporate bonds information is derived from the NIFTY Corporate Bond Index, and Bank Fixed Deposit interest rate is derived from SBI FD Rate (3-5 years, current)

What Are Government Bonds?

Simply put, these are fixed-income debt securities issued by the central or state governments to raise money for public expenditure. As these securities have a sovereign backing, they are considered among the most reliable avenues for long-term capital preservation and predictable income.

Investors receive periodic interest payments and the principal amount at maturity, making these securities suitable for conservative or risk-balanced portfolios. Government bonds are preferred by investors looking for diversification in the portfolio, having a low to moderate risk appetite.

The overall retail participation in government bonds India has increased significantly as they can be traded transparently through digital platforms.

Types of Government Bonds in India

You can find the following types of government bonds in India:

1. G-Secs: The Central Government of India issues these bonds. They have terms of 5 to 40 years. Investors get interest payments every six months and get their money back when the bond matures. These are considered one of the safest government bond investment options.

2. Treasury Bills: These are issued for 91 to 364 days. They do not pay interest. Instead, they are sold at a price and redeemed at face value when they mature. This makes them good for short-term investments.

3. State Development Loans: SDLs are issued by the State governments to raise money for projects. They often pay higher interest than G-Secs as they carry more risk.

4. Sovereign Gold Bonds: SGBs are connected to the price of gold. Investors earn a fixed interest rate every year. They can also benefit if the price of gold goes up. This way, people do not need to buy or store gold. New SGBs are not being issued now, but existing ones can still be traded.

5. Inflation-Indexed Bonds: IIBs help protect investors from inflation. The interest or principal is adjusted based on inflation changes. Although no new IIBs are being issued, they are a type of government security.

6. RBI Floating Rate Bonds: These RBI bonds have an interest rate that can change over time. The rate is based on the National Savings Certificate rate. They are meant for investors who want a stable government-backed income for a long time.

Key Terms To Understand Before Investing In Government Bonds

The following table lists the key terms you should understand before investing in government bonds:

Term | What It Means |

| Face Value | Also known as par value or principal. It is the exact amount the bond is worth when issued and the amount repaid at maturity. |

| Coupon Rate | The annual interest rate the government promises to pay you is usually distributed semi-annually or annually. |

| Maturity Date | The specific future date when the government repays the original face value to you. |

| Yield to Maturity or YTM | This is what you can expect to get if you buy the bond at market price and keep it until it matures. |

| Discount | This means buying the bond for less than its face value. |

| Premium | A premium means paying more than its face value. |

| Interest Rate Risk | The risk that bond prices in the secondary market will fall if broader market interest rates rise. |

| Sovereign Guarantee | The promise by the issuing national government to repay the debt. |

How To Invest In Government Bonds In India

With the rise of digital investment platforms, investing in bonds—including government securities—has become far more accessible for everyday investors. Platforms like Grip simplify not just the investment process but also the ongoing management and tracking of your bond portfolio.

This shift toward digital investing has significantly boosted retail participation in government securities, as investors now prefer options that offer predictable returns, lower volatility, and complete transparency. For anyone exploring how to invest in G-Secs in India, these platforms remove paperwork, reduce friction, and make fixed income investing smoother than ever.

Investing In Government Bonds Via Grip

In one way or another, Grip is a kind of revolution as it has democratized investment in bonds. The process, when done via conventional channels, was time-consuming, and there was an inherent factor of lower accessibility.

Here is how the process works:

| Sign up and complete KYC | Create an account and verify your identity through a quick online KYC process. |

| Explore available government securities | Browse the government bonds listings, with coupon rates details, maturities, credit standing, and expected yield. |

| Select the bond and start investing | Choose the amount you want to invest. Most listings offer a low minimum investment thresholds. This enables easy entry for new investors. |

| Track holdings and returns | Investors can track the interest to be received and overall performance directly on the platform. |

In addition to Grip, you can still invest in government bonds through the conventional modes.

Other Ways To Invest In Government Bonds

Here are some conventional ways of investing in bonds, besides the Grip platform:

- RBI Retail Direct: This allows investors to open an account directly with the RBI. Through which you can buy and sell government securities in both the primary and the secondary market.

- NSE and BSE Platforms: Selected government bonds are listed on both platforms. Investors can buy or sell these bonds through a registered stockbroker, like trading shares.

- Banks: Many banks offer government bonds during their primary issuance. Investors can apply through their bank when new bond issues are available.

- Debt Mutual Funds and ETFs: Debt mutual funds and ETFs invest in government securities and other debt instruments. This makes them suitable for those who prefer to invest in government bonds.

Benefits And Risks Of Government Bonds

There are numerous benefits that government bonds offer the investors, starting with stability, transparency, and predictability. As digital access improves and information becomes more widely available, government securities investment is increasingly seen as a disciplined way to balance risk, preserve capital, and attain long-term financial goals. Here are the most important benefits, followed by a few risks of government bond investment:

Benefits:

- Sovereign Safety: Backed by the Government of India, they carry minimal default risk.

- Predictable Income: Regular coupon payments help investors plan cash flows with certainty.

- Portfolio Stability: They reduce volatility and provide balance when equity markets fluctuate.

- Diversification: Low correlation with equity makes them ideal for risk mitigation.

- Tax Efficiency (SGBs): Sovereign Gold Bonds provide tax-free capital gains on maturity.

- Market Liquidity: Many G-Secs trade actively, enabling investors to buy and sell when needed.

- Even though there are fewer, there are still a few risks associated with government bonds. We have discussed them briefly.

Risks:

- Interest Rate Risk: Government bond prices move inversely to interest rates. When rates rise, the market value of existing bonds falls, which can impact returns if sold before maturity.

- Lower Yields: G-Secs generally offer lower returns than high-quality corporate bonds or other fixed income options, making them less attractive for investors seeking higher income.

- Liquidity Gaps: While G-Secs are considered safe, certain maturities—especially longer-tenor bonds and some State Development Loans (SDLs)—may witness low trading volumes, making it harder to exit quickly.

- Long Tenors: Many G-Secs have long maturities (10 to 40 years). Unless actively traded, these can lock in capital for extended periods, which may not suit investors with medium-term goals.

Who Should Invest In Government Bonds?

The following groups of investors benefit the most from government bonds:

- Risk-averse individuals: Government bonds are good for people who want to keep their money safe and do not want to deal with the ups and downs of the stock market. They give you returns, and the chance of losing money is very low.

- Retirees and pensioners: If you need an income, government bonds can be a good choice. You get interest payments at intervals, which can help you pay for your daily expenses and give you an income.

- Long-term financial planners: Government bonds are a good option for people saving for long-term goals. They let you lock in your returns for years with low risk of default.

- Portfolio diversifiers: Investors with a large allocation to equities can use government bonds to reduce overall portfolio risk. Adding government bonds can improve stability and balance during periods of market volatility.

Government Bonds Vs Corporate Bonds: Which Should You Pick?

Government bonds and corporate bonds both fall under fixed-income investments, but they differ significantly in terms of safety, return potential, and who they are best suited for. Government bonds are generally seen as more stable because they are backed by the sovereign, whereas corporate bonds offer higher yields in exchange for taking on company-specific credit risk.

A quick side-by-side view makes it easier for investors to match the right bond type to their risk appetite and financial goals.

| Parameter | Government Bonds | Corporate Bonds |

| Issuer | Central or state government | Private or public companies |

| Backing / Security | Sovereign backing (implied government guarantee) | Backed by issuer’s business strength and balance sheet |

| Default risk | Very low | Varies by rating; higher for lower-rated issuers |

| Typical returns (yields) | Moderate, generally lower than corporate bonds | Usually higher than government bonds |

| Credit rating range | Often high-quality (sovereign) | Ranges from AAA (high quality) to below investment grade |

| Interest (coupon) stability | High; coupons are usually predictable and timely | Depends on issuer’s performance and financial health |

| Market risk (price swings) | Present but usually lower than many corporate bonds | Can be higher, especially for lower-rated or longer-tenure issues |

| Liquidity | Often good in G-Sec markets; retail access improving | Varies; top-rated issues may be liquid, others less so |

| Ideal investor profile | Conservative investors prioritising capital safety | Investors seeking higher income and willing to accept more risk |

Conclusion

Government bonds are one of those investments that bring balance to a portfolio. They offer stability, predictable income, and peace of mind—especially when markets feel uncertain. Now that platforms like Grip make access simple and beginner-friendly, investing in government securities isn’t complicated or reserved for experts. If you're looking to add steady income and reduce risk in your portfolio, government bonds are worth considering.

Ready to get started? Visit Grip Invest today and explore government bond options with ease.

FAQs On How To Invest In Government Bonds In India

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001