Small Finance Bank FD Rates: Compare Interest Rates In 2026

Do you seek good returns with no exposure to market risks at all? The interest rates on fixed deposits provided by small finance bank FDs have been very attractive in 2026 due to the increased competition between banks to acquire deposits. Investors can take advantage of an opportunity to earn some good fixed returns without taking any risks.

The Small Finance Banks (SFBs) belong to the class of banks that fall under the regulatory domain of the Reserve Bank of India (RBI). The banks of this type serve the needs of unserved people, small businesses, farmers, and micro-enterprises.

One of the reasons behind high FD rates in small finance banks is that they need to draw deposits from customers to be able to lend. Therefore, many SFBs keep offering one of the highest FD rates available in the market; consequently, they become favourites of conservative investors.

Interest rates have been favourable in 2026, even though many banks have revised their FD offers considering liquidity and monetary policies. So now is the best time to find out about small finance bank FD rates and compare them.

This article will help you compare the latest small finance bank FD rates, find out why they are so high, and choose the best fixed deposit according to your needs.

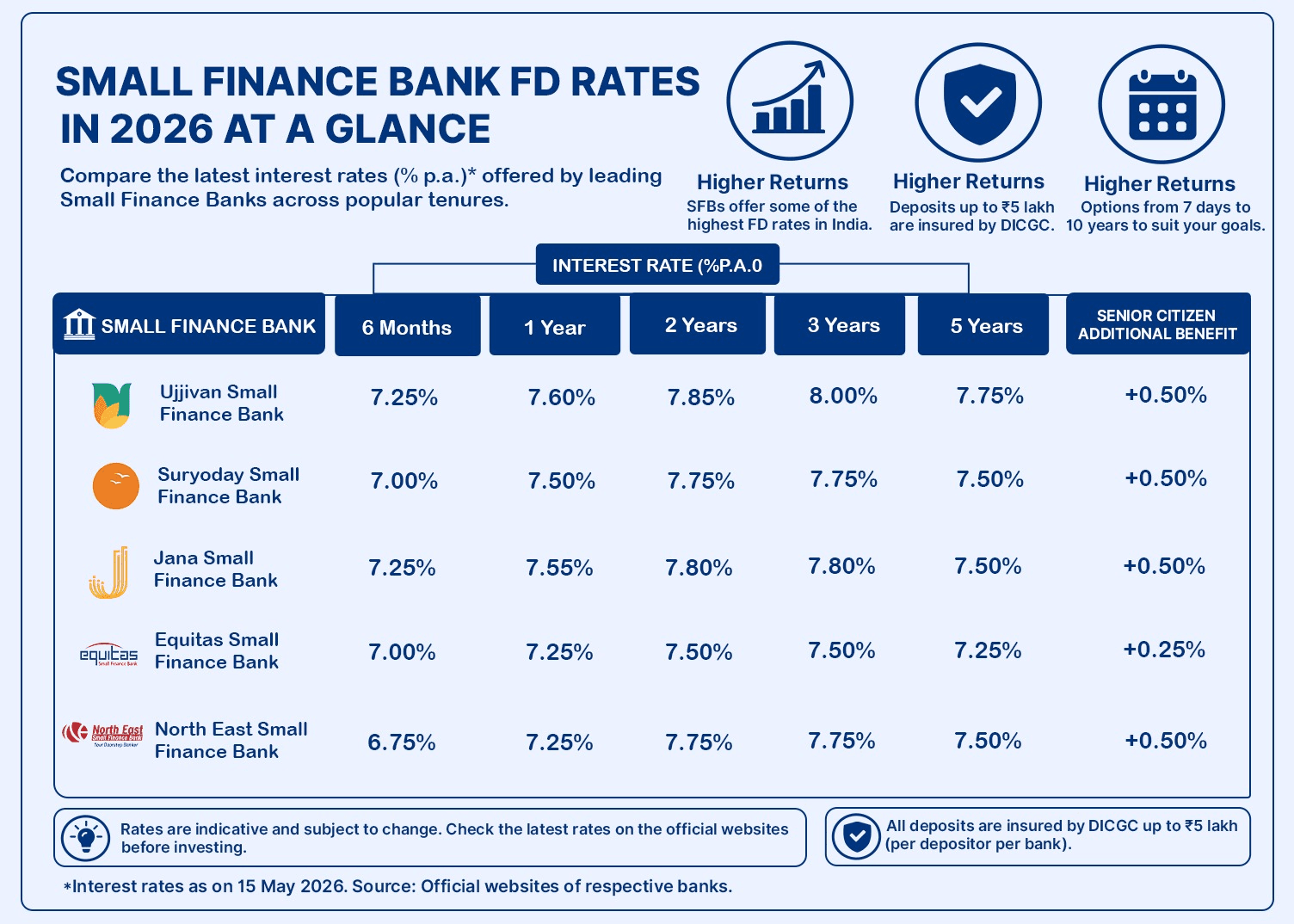

Latest FD Rates Across Leading Small Finance Banks

When considering the FD interest rates of small finance banks, you must not just look at the maximum advertised interest rate. Maximum interest rates are usually available only for certain tenure periods, like 18 months and 888 days. The comparison of FD rates on different tenures will provide more clarity about the best bank according to your investment period.

Below is the table that shows the top regular FD interest rates offered by the leading Small Finance Banks up to July 2026.

Small Finance Bank | Highest Regular FD Rate | Tenure Offering Highest Rate |

Suryoday Small Finance Bank | 8.10% | 18 Months |

Utkarsh Small Finance Bank | 8.10% | 666 Days |

Jana Small Finance Bank | 8.00% | 2–3 Years |

Equitas Small Finance Bank | 8.00% | Special FD (Maxima) |

Shivalik Small Finance Bank | 7.80% | 21–22 Months |

Unity Small Finance Bank | 7.75% | 12 Months |

Why Does One Bank Offer A Higher FD Rate Than Another?

The highest advertised FD rate does not necessarily mean one bank is better than another. Small Finance Banks often revise interest rates based on liquidity needs, deposit mobilisation targets and prevailing market conditions. A difference of 0.25% to 0.50% in interest rates should therefore be evaluated alongside factors such as the bank's financial position, tenure, premature withdrawal rules and deposit insurance coverage.

Why Do Small Finance Banks Offer Higher FD Rates?

FD rates of small finance banks could be because such banks use more money from customer deposits for their business activities. Because such banks receive fewer deposits compared to commercial banks, they give competitive interest rates on fixed deposits to attract more people to their business.

SFBs also lend to disadvantaged categories such as small-scale businesses and agricultural activities, and therefore, the money that comes in makes more profit, and they can maintain competitive SFB FD rates.

The return on your investments may be a good consideration, but it is not enough. Check the bank's finances and your deposit insurance cover before you go for the highest FD rates in India.

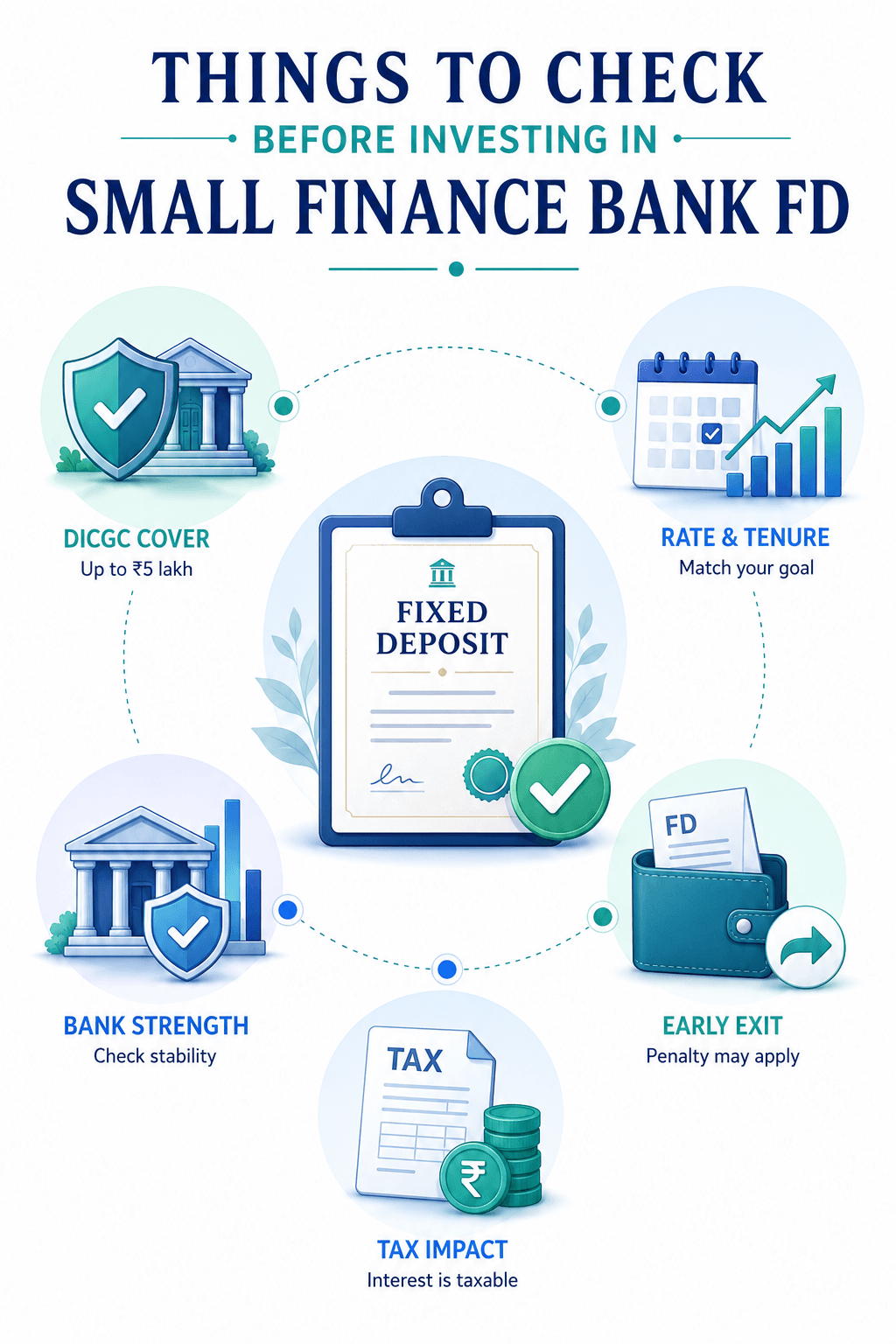

Things To Consider Before Investing

FD Rates of attractive small finance banks can help you get good returns on your investment, but they must not be the sole criteria for making investments. Below are some things to look at before investing to make sure the fixed deposit suits your financial objectives.

1. Coverage Under Deposit Insurance Scheme: Small Finance Bank deposits come under insurance from DICGC up to INR 5 lakh per depositor per bank along with interest. If you want to make a higher investment, you might have to diversify it among multiple banks.

2. Interest Rate & Tenure: Highest rates of small finance bank FDs may be applicable only for some tenures and not others. So, instead of going for the highest rate, you need to compare rates and tenure according to your investment period.

3. Early Withdrawal Provisions: It is quite usual for most banks to provide provisions for early withdrawals. They might, however, have some penalties or offer reduced rates of interest. Make sure to go through these conditions if there is any possibility that you may require access to your funds before maturity.

4. Strength of the Bank: Though all Small Finance Banks come under the regulation of the RBI, you still might want to evaluate their past financial performance and reputation. It will only add to your confidence in the bank and the investment you have made.

5. Taxation: Interest on Fixed Deposits is taxable depending on your income tax slab.

Common Mistakes Investors Make

- Investing only because of the highest interest rate

- Ignoring DICGC limits

- Selecting the wrong tenure

- Forgetting taxation

- Ignoring premature withdrawal penalties

How To Compare Small Finance Bank FD Rates?

Instead of simply comparing percentages, investors should evaluate:

- Effective annual return

- Investment tenure

- Interest payout frequency

- Premature withdrawal rules

- Deposit insurance coverage

- Post-tax returns

Small Finance Bank FD vs Other Fixed Income Options

Though the FD interest rates offered by small finance banks can be quite lucrative in the fixed-income universe, they are just one of the many choices available to you. You can use return, risk, and liquidity as criteria for selecting the best choice for you.

Investment Option | Expected Returns* | Risk Level | Liquidity | Best Suited For |

Small Finance Bank FD | 7.50%–8.10% | Low | Moderate (premature withdrawal allowed with penalty) | Investors seeking higher fixed returns |

Large Bank FD | 6.00%–7.00% | Very Low | High | Conservative investors prioritising safety |

6.90%–7.50% | Very Low | Moderate | Investors seeking government-backed savings | |

8.00%–11.00%** | Low to Moderate | Moderate to High (depending on bond type and market availability) | Investors looking for potentially higher yields with manageable risk |

Should You Invest In Small Finance Bank FDs?

FD rates of small finance banks can be one of the best choices available if you are aiming for stability and assured returns without exposure to market volatility. Nevertheless, their suitability will depend upon several aspects such as your financial objectives, liquidity requirements, and risk profile.

Who should consider them?

Small Finance Banks FDs should be considered if you prefer predictability and don't mind keeping your money locked in for a fixed period of time. Another scenario when these FDs can be chosen is when you require higher FD rates than large banks, but don't exceed the DICGC insurance limit.

Who should avoid them?

If you have liquidity requirements or don't mind taking risks to earn higher returns, then FDs from Small Finance Banks might not be right for you.

How Much Of Your Portfolio Should Be In Fixed Deposits?

The right allocation depends on financial goals, liquidity needs and risk appetite. Investors who prioritise capital preservation may allocate a larger share to fixed deposits, whereas investors seeking higher long-term returns may complement deposits with other regulated fixed-income investments. Diversification across institutions can also help reduce concentration risk.

Where Do Small Finance Bank FDs Fit In A Diversified Portfolio?

Even though FD rates offered by small finance banks are good enough for generating a handsome fixed income, they will never be the ideal way of managing fixed deposits alone. By diversifying your fixed deposit portfolio, you can not only manage your risk but also maximise your chances of earning decent money from the deposits.

A simple way through which this can be done would be by including corporate bonds to your existing fixed deposit portfolio. It allows you to generate handsome returns along with having the option of choosing the best bonds according to your goals and risk-taking capacity.

You can look out for the best opportunities in corporate bonds through platforms such as Grip Invest. By combining small finance banks' FDs with other forms of fixed deposits, you can have a diversified portfolio of investments instead of generating returns from one source alone.

Conclusion

FD Interest Rates for Small Finance Banks in 2026 remain an attractive choice for those investors seeking stability and predictability. Nevertheless, one must look beyond the maximum interest rate alone and consider factors such as tenures, DICGC insurance, and matching the product with one's financial objectives.

On the other hand, creating a strong investment portfolio sometimes requires more than a single investment product. One can create a diversified investment strategy by adding investments in fixed income apart from investing in Small Finance Bank FD.

Would you like to diversify your fixed income portfolio? Take advantage of corporate bonds with our curated choices from Grip Invest.

FAQs On Small Finance Bank FD Rates

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001