FD Income Tax Exemption: Rules, Limits And Ways To Save Tax

Fixed deposits remain a popular choice amongst many Indians who want secure and safe investment vehicles that provide predictable returns. However, many investors are often surprised by their tax implications when it comes to earning interest on their fixed deposits.

Understanding the rules around tax exemptions can help you retain more of the money that you earn.

Is FD Interest Tax-Free In India?

Many investors believe that fixed deposit (FD) interest is completely tax-free because the principal amount invested remains safe. However, while the principal amount you deposit is not taxed again, the interest earned on your FD is taxable as per your applicable income tax slab.

FD interest is added to your total income for the financial year and taxed accordingly. The tax treatment depends on your overall income, deductions, and the applicable tax slab.

Banks also report interest payments to tax authorities and may deduct Tax Deducted at Source (TDS) when the interest earned crosses the prescribed limit. Therefore, investors should declare FD interest income while filing their income tax returns, even if TDS has already been deducted.

How FD Income Is Taxed?

The tax you pay on fixed deposit interest depends on your total income during the financial year. FD interest is added to your overall income and taxed according to your applicable income tax slab.

For example, if you fall under the 20% tax slab, your FD interest income (after considering applicable exemptions and deductions) will be taxed at 20%.

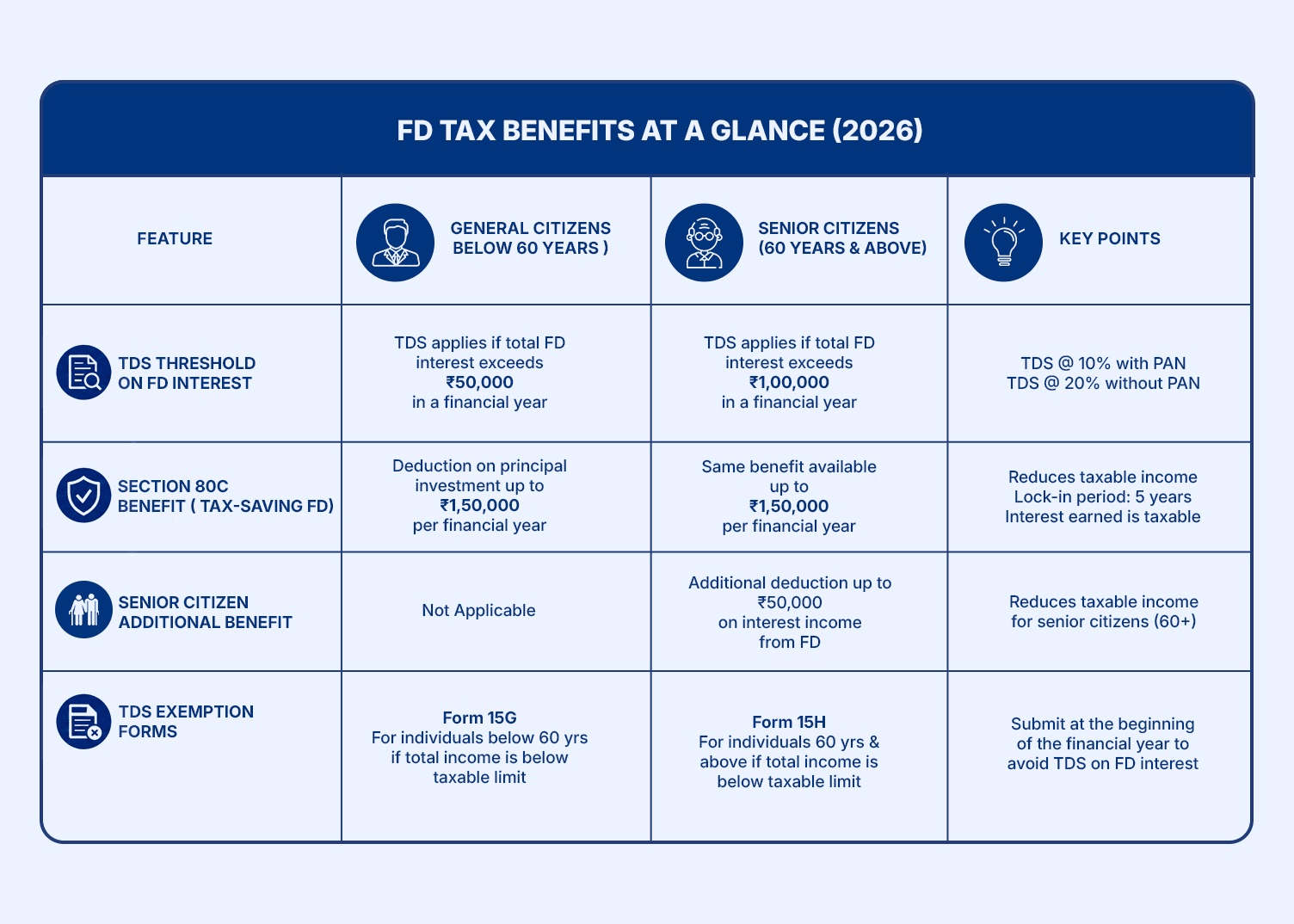

Banks deduct Tax Deducted at Source (TDS) on FD interest when the interest earned exceeds the prescribed threshold limit in a financial year. The TDS rate is generally 10% if your PAN details are submitted to the bank. If PAN is not provided, TDS may be deducted at a higher rate.

Senior citizens have a higher TDS threshold compared to other individuals, making fixed deposits relatively more tax-efficient for retirees.

While filing your income tax return, you can claim credit for the TDS already deducted by the bank. The final tax liability is calculated based on your total taxable income, and you may need to pay additional tax or receive a refund depending on the difference.

FD interest is taxable in the year it is earned or credited, even if you choose not to withdraw the interest amount.

For Example:

Priya has received INR 60,000 in interest from fixed deposits during a financial year. Her bank deducted TDS amounting to INR 6,000 (at a rate of 10%). Priya is within the 20% slab, therefore, her actual tax liability is INR 12,000. Priya has an additional payment of INR 6,000 for tax owed at the time of filing her return.

FD Income Tax Exemptions And Deductions Available

1. Tax Burden Reduction

Many Tax-saving provisions allow people to reduce their tax burden and can help them save taxes by allowing tax deductions from their taxable income. Each taxpayer of the financial year can reduce their total tax liability due to an income member.

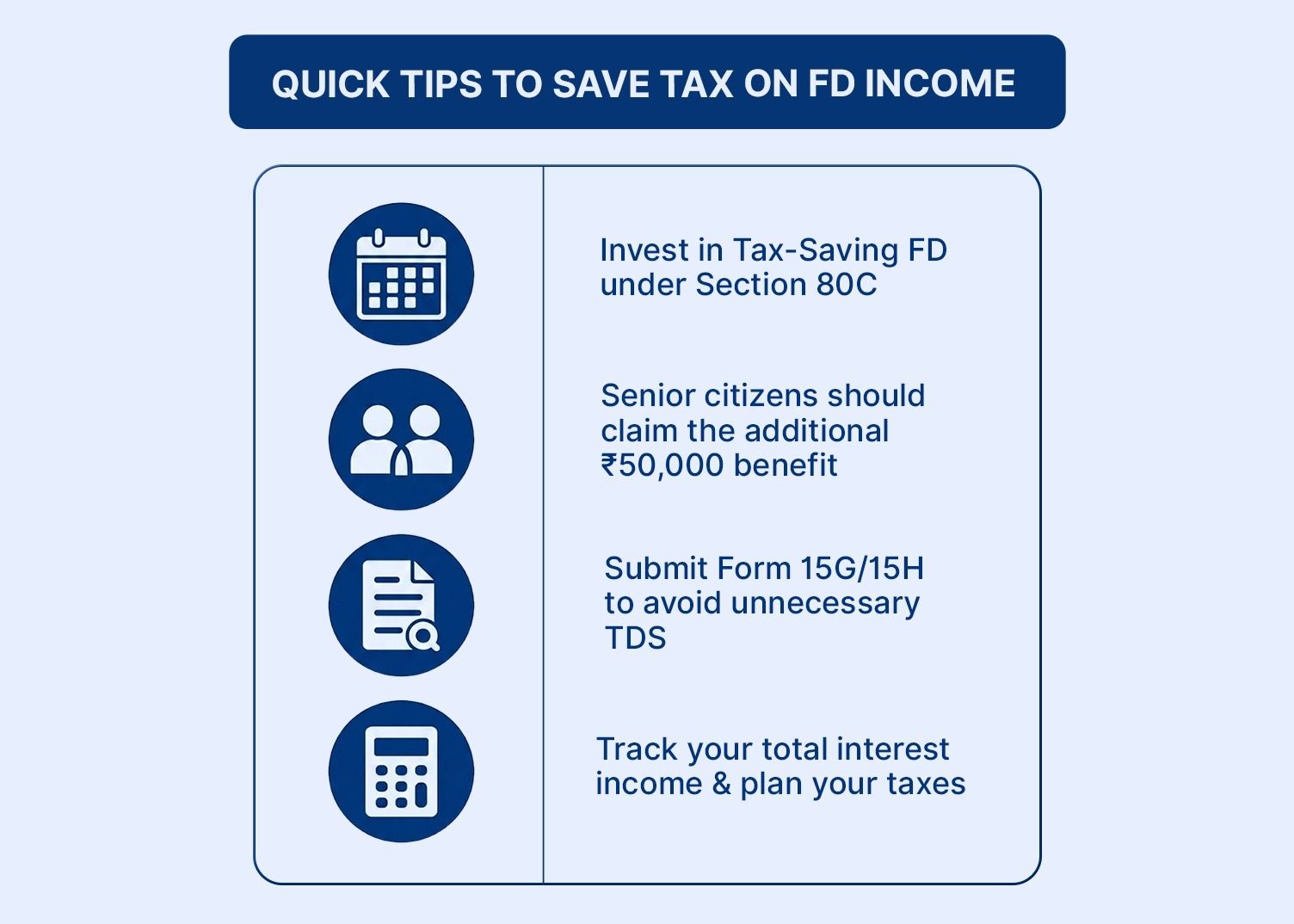

Tax-saving fixed deposits fall under Section 80C. They allow you to deduct the principal amount invested in a tax-saving FD up to INR 1,50,000 per financial year. Therefore, the amount of tax you pay will be directly affected by the FDs you invest in. However, the interest earned on tax-saving fixed deposits will be subject to income tax.

2. Senior Citizen Tax Benefit

Senior citizens (60 plus) receive more favourable tax treatment than others do. As a result, senior citizens can offset up to INR 50,000 against their interest income from fixed deposits. This benefit from fixed deposits will be of significant assistance to seniors who depend on fixed deposit interest.

3. TDS Exemption

Form 15G on FD is required for taxpayers under the age of 60 to be able to avoid TDS on fixed deposits when their projected total annual income falls below the threshold for taxability. Similarly, Form 15H is for individuals over age 60. Both of these must be submitted to your FD bank at the beginning of the financial year. By using fixed deposits with the appropriate tax deduction methods based on projected income and submitting the required forms, you can receive higher returns than you would without these benefits.

Also read on Claim Tax Deductions Using Form 12BB

Who Pays Tax On FD Interest?

Tax is usually paid on interest to almost everyone who earns it over the basic exemption limits.

- All salaried earners have FD Interest added to their salary income, and good planning allows them not to move into the higher tax brackets.

- For Senior Citizens, they benefit by having the higher TDS limits and Section 80TTB deduction, thus making FD tax exemption India more accessible.

- For NRIs, they face separate sets of rules regarding TDS, and usually, TDS is deducted at a higher rate, and they cannot file Form 15G or 15H.

- For joint FD accounts, the tax liability depends on the ownership structure and contribution towards the deposit. Maintaining proper records can help avoid confusion while reporting interest income.

Ways To Reduce Tax On FD Income Legally

With smart planning, it is possible to increase your total net returns from safer investments that provide tax savings.

- You can consider tax-saving FDs to claim deductions under Section 80C of the Income Tax Act. These FDs come with a 5-year lock-in period, and the eligible investment amount qualifies for deduction up to the prescribed limit. However, the interest earned remains taxable.

- Investors can also plan their FD investments across different banks based on their financial goals, liquidity needs, and applicable tax rules. This can help manage concentration risk while ensuring efficient allocation of funds.

- Planning the timing of FD maturity and choosing between cumulative and non-cumulative FDs can also impact your cash flow and tax planning. Cumulative FDs reinvest the interest until maturity, while non-cumulative FDs provide regular interest payouts.

- For families, investments can be structured carefully based on individual income levels and applicable tax regulations. However, investors should consider clubbing provisions under tax laws before transferring investments to family members.

- Apart from FDs, diversifying across other fixed income options such as PPF, bonds, or other tax-efficient instruments may help create a balanced investment portfolio and manage overall tax impact.

Reviewing your FD investments and tax strategy every year can help you make better financial decisions.

Also read on How FD Interest Is Taxed Under Different FD Types?

Common FD Tax Mistakes To Avoid

Many investors assume that fixed deposits are completely tax-free, which can lead to surprises while filing income tax returns. While the principal amount invested in an FD remains unaffected, the interest earned is taxable as per your applicable income tax slab.

Banks may deduct Tax Deducted at Source (TDS) on FD interest when it crosses the prescribed limit. However, TDS is only a deduction made by the bank and does not represent your final tax liability. The actual tax payable is calculated when you file your income tax return.

If you are eligible to avoid TDS, submitting Form 15G or Form 15H (for senior citizens) on time is important. Incorrect details or delayed submission may result in unnecessary TDS deductions.

Many investors also miss out on tax-saving FD benefits under Section 80C of the Income Tax Act. Tax-saving FDs have a lock-in period of 5 years, and while the invested amount may qualify for deduction up to the prescribed limit, the interest earned remains taxable.

Understanding these rules can help investors plan their fixed deposit investments better and avoid unexpected tax liabilities.

Additional Considerations

If an investor withdraws an FD before maturity, the bank may apply a premature withdrawal penalty and revise the interest rate applicable to the deposit. The final interest payout depends on the bank’s terms and the period for which the FD was held.

Premature withdrawal does not remove the tax liability on interest already earned. FD interest remains taxable as per the applicable income tax rules, whether it is withdrawn or accumulated.

Tax regulations may change from time to time, so investors should stay updated on the latest rules and understand how they apply to their financial situation. Those with multiple income sources, significant investments, or complex tax requirements may consider consulting a tax professional for better planning.

Conclusion

Investors who know the tax exemption process and the investment strategies that allow them to maximize their returns can continue to build wealth consistently and can remain compliant with the relevant tax legislation. You should review your financial position before any major investment decision and should seek advice from a tax expert.

Grip offers corporate bonds and other fixed-income investment options with yields up to 12.5% and institutional-grade security features. Visit Grip Today!

FAQs On FD Income Tax Exemption

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001