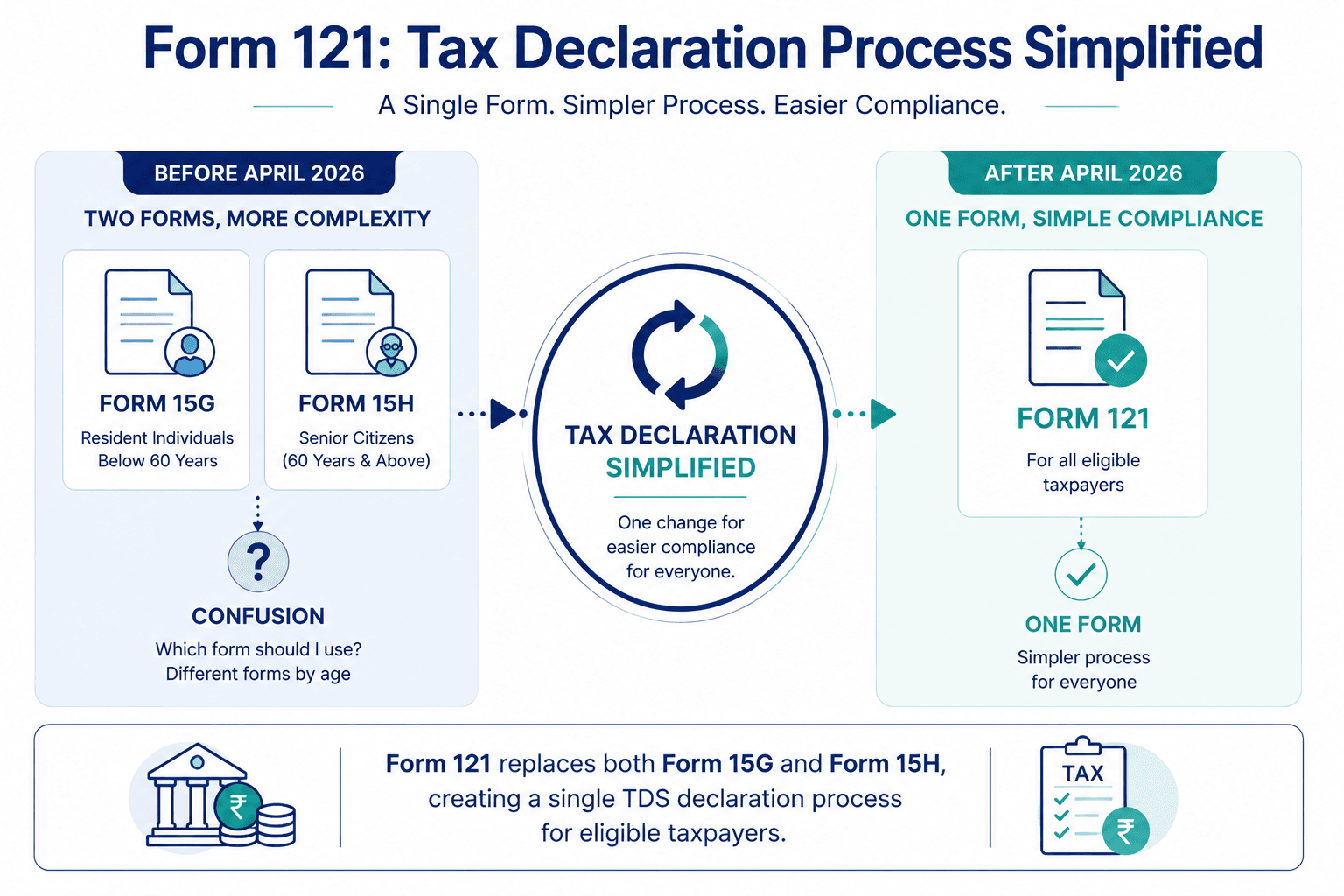

Form 121 Explained: The New Tax Form Replacing 15G And 15H

Banks, issuers and other payers may deduct TDS-Tax Deducted at Source on FD, bond interest, PF withdrawals and Pension, Insurance Commission, Rent, Interest on deposits, etc., once the prescribed threshold is crossed. To avoid TDS , eligible taxpayers have so far relied on Forms 15G and 15H1.

From 1 April 2026, that process is set to change, with Form 121 replacing both declarations for the relevant tax years. With 9.19 crore individual ITRs filed in FY 2024–25, even a small compliance change can matter to a very large number of taxpayers2.

In this blog, let us understand what Form 121 is, how it works, and what it could mean for investors.

How To Download Form 121?

You can download the pdf of Form 121 from the following link:

What Were Forms 15G And 15H

Forms 15G and 15H were widely used as a TDS declaration form India taxpayers (as per Section 393(6) of the 2025 Act) could submit to request that tax was not deducted at source on certain incomes, including fixed deposit, bond interest.

- Form 15G was generally meant for resident individuals below 60 years of age and certain other eligible persons, such as HUFs, subject to the prescribed conditions. Its purpose was to declare that the person’s estimated tax liability for the year was nil, so TDS need not be deducted on eligible income such as bank deposit interest.

- Form 15H was meant for resident individuals aged 60+ years. It helped eligible senior citizens receive interest income without TDS, provided their estimated tax liability for the financial year was nil3.

Under the updated framework, both have now been replaced by Form No. 121.

What Is Form 121

Form 121 is the new unified self-declaration form that eligible taxpayers can submit to a bank, issuer or other payer to request that TDS is not deducted on certain incomes.

This applies when their estimated tax liability for the financial year is nil.

As a Form 15G replacement and Form 15H replacement, Form 121 removes the need to choose between two separate declarations based on age.

This makes the process more streamlined for taxpayers as well as payers4.

Source: Income Tax India5

In terms of eligibility, it can be used by resident individuals below 60 years, resident senior citizens, and other eligible persons, subject to the prescribed conditions. Companies and firms are excluded.

As for timing, Form 121 has to be furnished before the scheduled transaction date. It must be submitted to each payer separately.

Difference Between Form 15H vs 15G vs 121

Here are the key features of Form 121:

| Basis | Form 15G | Form 15H | Form 121 |

| What it was for | A declaration to ask the payer not to deduct TDS on eligible income | The same purpose, but meant for senior citizens | A single replacement form now used for the same broad purpose |

| Who it applied to | Resident individuals below 60 and certain other eligible resident persons, excluding companies and firms | Resident individuals aged 60 or above | Eligible taxpayers who would earlier have used either Form 15G or Form 15H |

| Age split | Below 60 years | 60 years or more | No separate form by age, since both earlier forms are merged into one |

| Tax condition | Could be used only where the estimated tax liability for the year was nil | Could be used only where the estimated tax liability for the year was nil | The nil-tax-liability condition continues under the new framework |

| Income threshold point | Also carried the additional condition that the person's total income for the year, including the income for which the declaration was being filed, should not exceed the basic exemption limit. | This extra cap did not apply in the same way for senior citizens | The merged form retains the underlying eligibility conditions but removes the need for separate forms based on age, both below-60 and senior citizen taxpayers now use a single form |

| Legal basis | Section 197A of the Income-tax Act, 1961 | Section 197A of the Income-tax Act, 1961 | Section 393(6) of the Income-tax Act, 2025 |

| Form format | Separate form | Separate form | Unified form that replaces both from tax years starting on or after 1 April 2026 |

| Main practical change | Taxpayers had to decide whether 15G was the right form | Taxpayers had to decide whether 15H was the right form | That confusion is removed because there is now one common form instead of two |

How Form 121 Impacts FD And Bond Investors

The move to Form 121 could change how eligible FD and bond investors handle TDS declarations. Here are the key impacts:

1. Avoiding TDS on interest income:

If you meet the conditions, Form 121 can be submitted so that TDS is not deducted on eligible income, including fixed deposit interest and certain bond interest. It is not mandatory for everyone.

It is meant only for those who want non-deduction of tax and qualify under the rules. The declaration must be filed separately for each tax year.

2. Applicability for bank deposits and bonds:

This matters directly to FD investors because interest on deposits is explicitly covered under Form 121. Similarly, bond investors receiving interest from issuers or platforms may also use the form, subject to eligibility and the nature of the bond structure.

Since the form has to be submitted to each payer separately, investors holding FDs across multiple banks or bonds issued by different entities may need to file multiple declarations.

3. Impact on senior citizens:

One practical change is that senior citizens will no longer use a separate Form 15H. Under the new system, both taxpayers below 60 and those aged 60 or above will use Form 121, making it a common declaration form across eligible age groups.

Resident senior citizens can use it, subject to the prescribed conditions

Step by Step Process To Submit Form 121

Submitting Form 121 is fairly straightforward, but the sequence matters.

- First, check that you are eligible to file it and that your estimated tax liability for the tax year is nil.

- Then keep the key details ready, including PAN, tax-year details, income details, and the particulars of the bank or payer from whom you will receive the income.

You should also file it early enough for the payer to act on it before the income is credited or paid. For FD investors, that usually means submitting the declaration before the first relevant interest credit. Once the payer accepts it, the declaration is recorded in the prescribed system, so accuracy in PAN, income details, and tax-year information is important6.

A. Online submission

If your bank offers internet or mobile banking support for Form 121, the online route will usually be the simpler option.

- Start by downloading the form or opening the bank’s digital filing page.

- Then enter your PAN, tax-year details, income details, and the nature of income for which you want TDS not to be deducted, such as fixed deposit, bond interest. Since the declaration is time-sensitive, submit it before the bank credits or pays the income.

After submission, the bank verifies the declaration and assigns a Unique Identification Number (UIN) - a composite identifier comprising the sequence number, tax year, and the payer's TAN and reports the details through the prescribed monthly and quarterly filings.

For investors, that means accuracy matters.

If the PAN, income details, or tax-year information do not line up properly, the declaration can run into processing issues.

B. Offline Submission

If your bank does not provide a digital option, you can submit Form 121 in paper form. In that case:

- Obtain the form from the Income-tax Department website or the bank,

- Fill in the required particulars carefully, and submit it to the branch or payer that will make the payment.

The underlying rules stay the same. You still need a valid PAN, complete income details, and timely submission before the payment or credit date.

One declaration does not cover every bank, and it does not carry forward automatically into the next tax year.

So, if you hold FDs across multiple institutions, you may need to repeat the process bank by bank. That is a small but important compliance point for deposit investors.

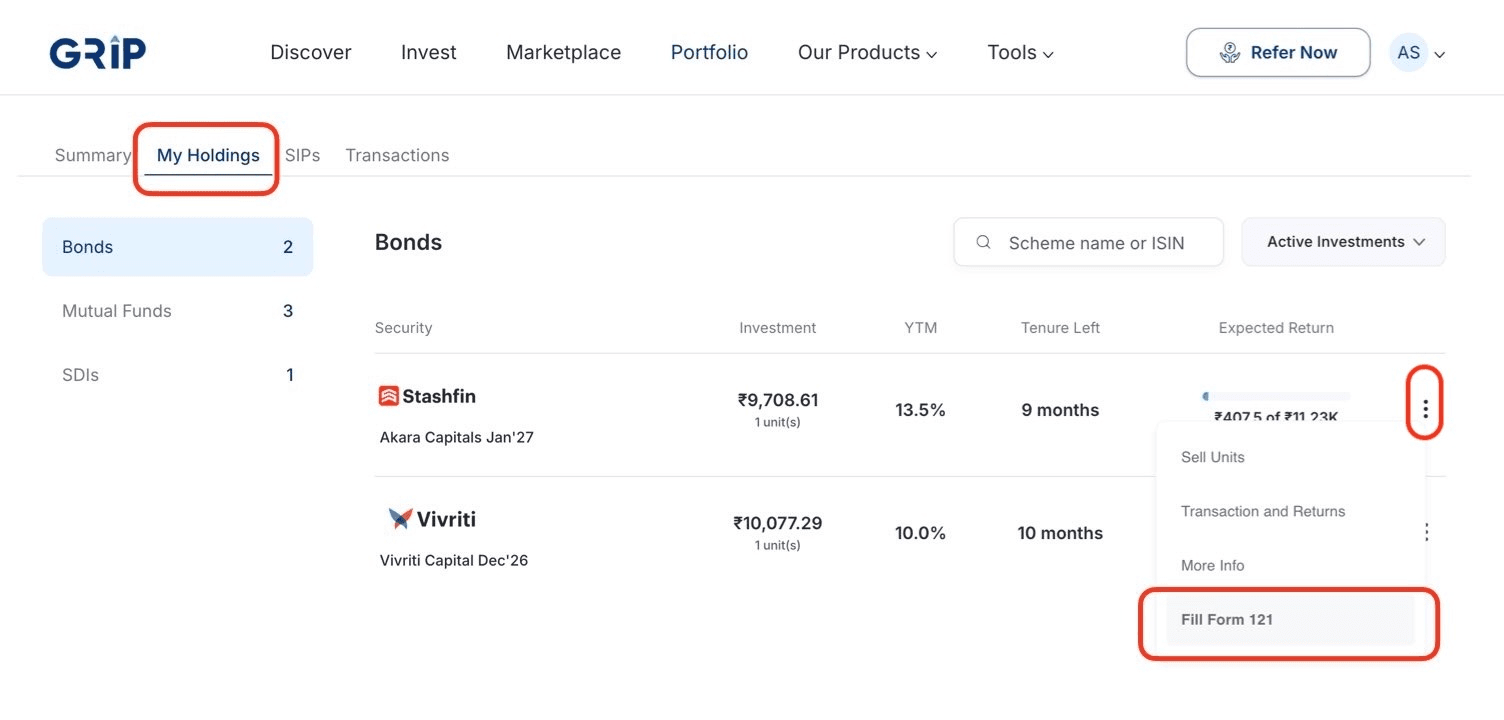

Submit Form 121 Effortlessly: Now Live on Grip

Form 121 is now officially live on the Grip platform, making TDS exemption claims faster and simpler than ever. No more manual filling - details are auto-prefilled for each holding, and you can verify, eSign with Aadhaar, and submit in seconds.

Quick Steps to Submit Form 121 Online

Step 1: Log in to Grip and navigate to My Portfolio > My Holdings.

Step 2: Find your investment, click the 3 dots (…) next to it.

Step 3: Select Fill Form 121—your details will be pre-populated.

Step 4: Review for accuracy, complete Aadhaar eSign, and submit instantly.

Click here to check your holding

Key Reminders Before Submitting

- Submit separately for each issuer/holding.

- Confirm your tax liability is NIL - Form 121 only exempts TDS, not income tax.

Grip pre-fills based on your data; double-check everything. Errors could lead to rejection or Income Tax penalties.

Conclusion

Form 121 marks a shift towards a simpler and more streamlined TDS declaration system by replacing both Form 15G and Form 15H. By introducing a single unified form, the new framework removes age-based confusion while continuing to focus on the core condition of nil tax liability.

For FD investors and other income earners, this change makes compliance more straightforward but also highlights the importance of timely and accurate submission. Since Form 121 must be filed separately for each payer and financial year, staying proactive becomes essential to avoid unnecessary TDS deductions.

As tax processes become more digitised and structured, understanding such updates can help investors manage cash flows more efficiently and avoid delays in refunds. Alongside this, diversifying beyond traditional deposits into fixed-income options available on platforms like Grip can help optimise returns while maintaining predictable income.

FAQs On Form 121

1. What is Form 121 and who can use it?

Form 121 is a unified TDS declaration form that replaces Forms 15G and 15H. It can be used by eligible resident taxpayers with nil estimated tax liability.

2. How is Form 121 different from Form 15G and 15H?

Form 121 combines both forms into one, removing the age-based distinction while retaining the same eligibility conditions for non-deduction of TDS.

3. Can Form 121 be used to avoid TDS on Bond interest?

Yes, eligible taxpayers can submit Form 121 to request non-deduction of TDS on Bond interest, provided their tax liability is nil.

4. Is it mandatory to submit Form 121 every year?

Yes, Form 121 must be submitted separately for each financial year and to each payer where you want TDS exemption.

5. Can I submit Form 121 online?

Many banks offer online submission through net banking or mobile apps, but it can also be submitted offline at the branch if required.

6. What happens if Form 121 is not submitted on time?

If not submitted before the income is credited, the payer may deduct TDS, which can only be claimed later while filing your ITR.

References:

1. Income Tax Department, accessed from: https://www.incometaxindia.gov.in/documents/20117/43120/FAQs-on-Interplay-and-Transition.pdf#page=38

2. PIB, accessed from: https://www.pib.gov.in/PressNoteDetails.aspx?ModuleId=3&NoteId=154926®=3&lang=2

3. Income Tax India, accessed from: https://www.incometaxindia.gov.in/documents/20117/43120/FAQs-on-Interplay-and-Transition.pdf#page=38

4. Income Tax India, accessed from: https://www.incometaxindia.gov.in/documents/d/guest/fn-121

5. Income Tax India, accessed from: https://www.incometaxindia.gov.in/documents/20117/43120/FAQs-on-Interplay-and-Transition.pdf#page=39

6. Income Tax India, accessed from: https://www.incometaxindia.gov.in/documents/d/guest/fn-121

Author: Grip Invest Editorial Team

The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001