Term Deposit Scheme: Meaning, Types, Benefits And How It Works

Investment has become essential for building long-term wealth. Many investors choose investment options with better returns and less risk. One such investment option is a term deposit scheme. It will allow you to invest a lump sum for a fixed period while earning a predetermined interest rate.

According to RBI, banks are free to determine their own term deposit interest rate and their own term deposit interest rate.

A term deposit account locks your funds for a chosen period of time at a fixed rate of interest. However, a savings account allows you to deposit and withdraw money anytime. A combination of stability, fixed returns and capital protection makes a term deposit a preferred investment choice for many investors.

Why Investors Choose Term Deposit Schemes?

Term deposit schemes are widely used because they provide certainty. Unlike market-linked investments whose value can fluctuate daily, a term deposit offers a fixed interest rate for a predefined tenure. This makes it easier for investors to estimate future returns and plan for goals such as emergency funds, education expenses or short-term savings.

Types Of Term Deposit Schemes

There are different types of term deposit schemes for various investment needs.

1. Bank Fixed Deposits

A fixed deposit scheme offered by a bank is the most popular investment choice. Investors deposit a lump sum amount for a fixed tenure with a fixed interest rate. The interest rate remains unchanged throughout the tenure. It is suitable for individuals seeking capital safety, regular payments, and long-term wealth preservation.

2. Post Office Term Deposits

A post office term deposit is backed by the Government of India, making it one of the safest investment options available. The tenure is about 1,2,3 and 5 years, with interest revised periodically by the government. Many conservative investors prefer post office term deposits because of security and government backing.

3. Corporate Fixed Deposits

These fixed deposits are offered by companies and provide higher returns with relatively higher risks. Investors should always evaluate a company’s financial health before investing.

4. Tax Saver Term Deposits

Tax saver fixed deposits come with a mandatory lock-in period of five years. They qualify for tax deductions under applicable income tax provisions, subject to prevailing tax laws. It is ideal for investors looking to save taxes.

5. Senior Citizen Deposit Schemes

Many banks offer special term deposit schemes for senior citizens with higher interest rates than regular deposits. This scheme helps retired citizens to generate a stable source of income.

Which Type Of Term Deposit Is Suitable For You?

| Investor goal | Suitable option | Why it fits |

| Maximum safety | Post Office Term Deposit | Backed by government/sovereign guarantee; very low credit risk |

| Stable returns | Bank Fixed Deposit | Predictable interest and wide branch/online access |

| Tax saving | Tax Saver Fixed Deposit | 5-year lock-in with Section 80C tax deduction (up to ?1.5 lakh) |

| Higher income potential | Corporate Fixed Deposit | Higher interest than banks but higher credit/default risk; choose high-rated issuers |

| Retirement income | Senior Citizen Deposit | Higher interest rates for senior citizens and payout frequency options (monthly/quarterly) |

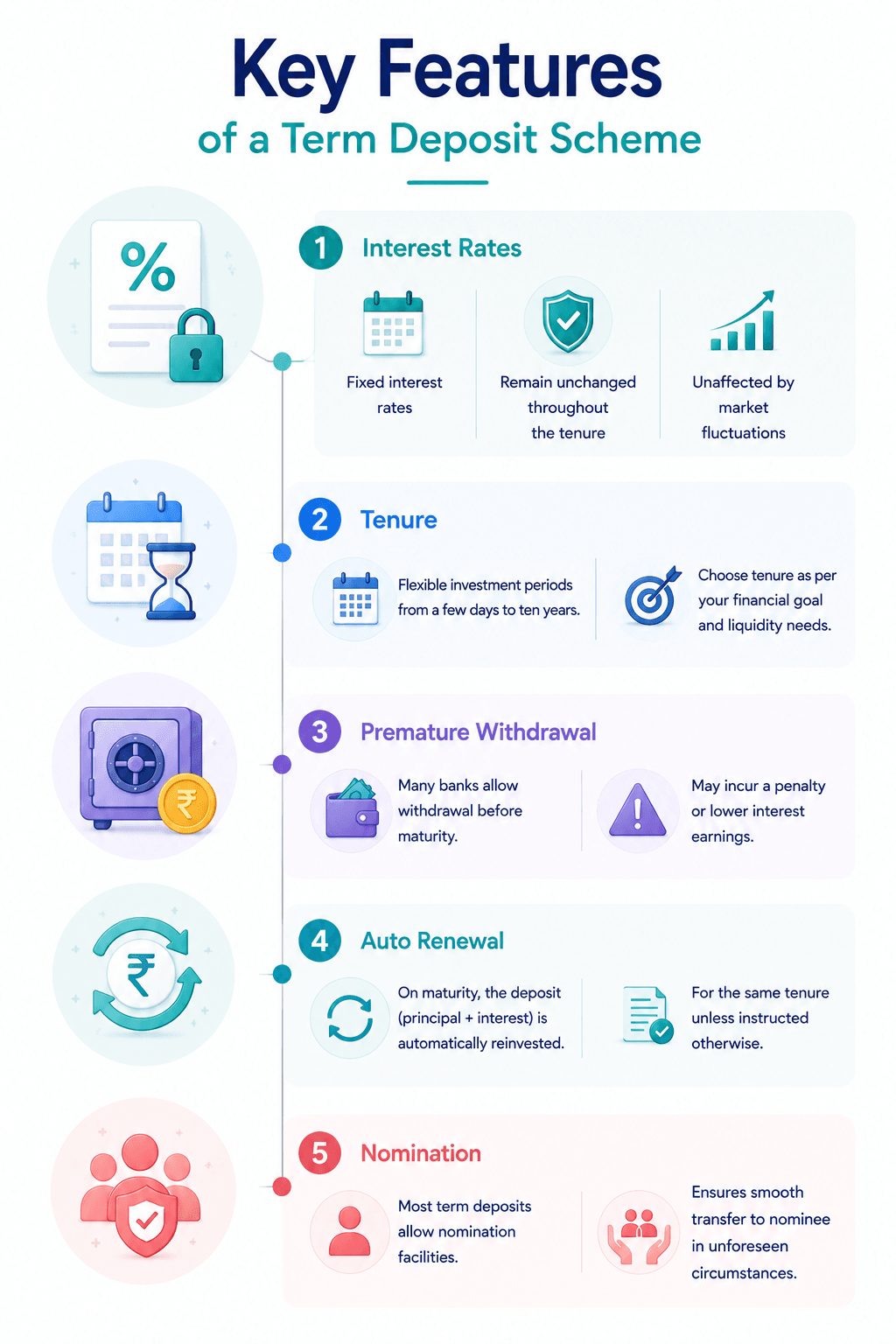

Key Features Of A Term Deposit Scheme

Every term deposit account has features that make it a preferred investment option for conservative investors.

1. Interest rates

Term deposits offer fixed interest rates that remain unchanged throughout the tenure, regardless of any market fluctuations. Interest can be paid monthly, quarterly or annually depending on the deposit type.

2. Tenure

Term deposits offer flexible investment periods, ranging from a few days to ten years. The tenure depends on the investor's financial goal and liquidity requirements.

3. Premature withdrawal

Many banks allow investors to withdraw their deposits before maturity. However, premature withdrawals may incur a penalty or lower interest earnings.

4. Auto renewal

Once the deposit matures, banks also provide an auto-renewal facility. The principal amount plus interest is automatically reinvested for the same tenure unless instructed otherwise.

5. Nomination

Most term deposits allow nomination facilities. During the unfortunate demise of the account holder, the investment is smoothly transferred to the nominee.

How Is Interest Calculated On A Term Deposit?

Interest on a term deposit is calculated according to the interest rate, investment amount, tenure and compounding frequency specified by the bank or institution.

Some deposits pay simple interest, while others compound interest quarterly or at other predefined intervals. Investors should therefore compare the maturity value rather than only the advertised interest rate.

Example:

Suppose an investor deposits INR 5 lakh in a five-year term deposit offering 7% annual interest. If the deposit compounds quarterly, the maturity value will generally be higher than if interest is paid out periodically. The exact return depends on the institution's compounding method and payout option.

Term Deposit Scheme vs Other Investment Option

Before choosing a term deposit scheme. Here is a comparison table between term deposita nd other investment options.

Features | Fixed Deposit | PPF | Corporates Bonds | Debt Mutual Funds |

Risk Level | Very low | Very Low | Moderate | Moderate |

Return | Fixed | Government declared | Market-linked coupons | Market linked |

Lock-in | Flexible | 15 years | Vraies | No fixed |

Liquidity | Moderate | Low | Moderate | High |

Tax Benefits | Only Tax saver FD | Yes | Limited | Depends on the holding period |

Capital Protection | Yes | Yes | Depends on the issuer | Not guaranteed |

Suitable for | Conservative investors | Long-term retirement | Higher income seekers | Diversifaication |

Note: The comparison shows that no single investment is suitable for every financial goal. Term deposits provide predictable returns and capital stability, whereas products such as debt mutual funds and corporate bonds may offer higher return potential in exchange for additional market or credit risk. Investors should compare investments based on their objectives rather than returns alone.

Things To Consider Before Opening A Term Deposit

A term deposit is a safe investment option; however, there are some things investors should consider before investing in it.

- Compare Interest Rates - Different banks, post offices, and NBFCs offer different term deposit interest rates. Comparing them helps you earn better returns.

- Tenure - The investment duration should align with your financial goals. Avoid locking money for a longer time if you anticipate liquidity later.

- Premature Withdrawal Rules - Understand the penalties and conditions associated with early withdrawal of your mine before opening it.

- Institution's Credibility - Before investing in corporate fixed deposits, always verify the company’s credit rating and financial stability.

- Understand Tax Implications - Interest earned from most term deposits is taxable according to your applicable income tax slab. Consider post-tax returns while making investment decisions.

Common Mistakes Investors Make

- Choosing the highest interest rate without checking credibility.

- Ignoring premature withdrawal penalties.

- Locking money for longer than required.

- Not comparing post-tax returns.

- Forgetting nomination.

Is A Term Deposit Scheme Right For You?

A term deposit scheme is ideal for investors who prioritise safety over higher returns. It is best suited for retirees, first-time investors, salaried professionals, and individuals building an emergency corpus.

If your primary objective is capital protection while also earning predictable returns, then a term deposit is a great option for your investment portfolio. However, investors looking for market-linked growth can consider diversification.

Where Does A Term Deposit Fit In Your Portfolio?

A fixed deposit scheme offers stability with guaranteed fixed returns and capital protection. However, relying on a single investment option can limit your income potential. Building a balanced fixed-income portfolio involves combining different investment options depending on your risk tolerance. Investors looking to diversify fixed-income investments beyond traditional deposits can also explore corporate bonds on Grip Invest to build a more balanced income portfolio.

Conclusion

A term deposit scheme remains the most trusted and secure investment option for individuals seeking safety and predictable returns. However, before investing, investors should consider various term deposit options and interest rates offered by them. Tenure period and premature withdrawal rules are also important factors.

Investors looking to diversify their fixed income portfolio, they can explore Grip Invest. It is a platform that offers various investment options that will align with investors' long-term financial goals.

FAQs On Term Deposit Scheme

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001