India’s Big Advantage From The Dollar Collapse

Introduction: The Cracks In Dollar Dominance

The rise of the dollar began in 1944 when Bretton Woods replaced sterling as the global benchmark1. Its hold strengthened in 1971 after the gold link was abandoned, leaving the system reliant only on U.S. credit.

Resistance emerged time and again, questioning this dominance. This is called de-dollarization. It describes the gradual push to reduce dollar dependence in trade, finance, and reserves. Countries such as India, China, and Brazil favour local currency settlements, pointing to a gradual rebalancing of global power.

In 2025, tariffs and debt concerns have unsettled long-standing partners and brought old doubts back to the surface. Hence, let us now look closer at the recent dollar collapse and what drives this decline.

The Dollar's Decline: Causes And Evidence

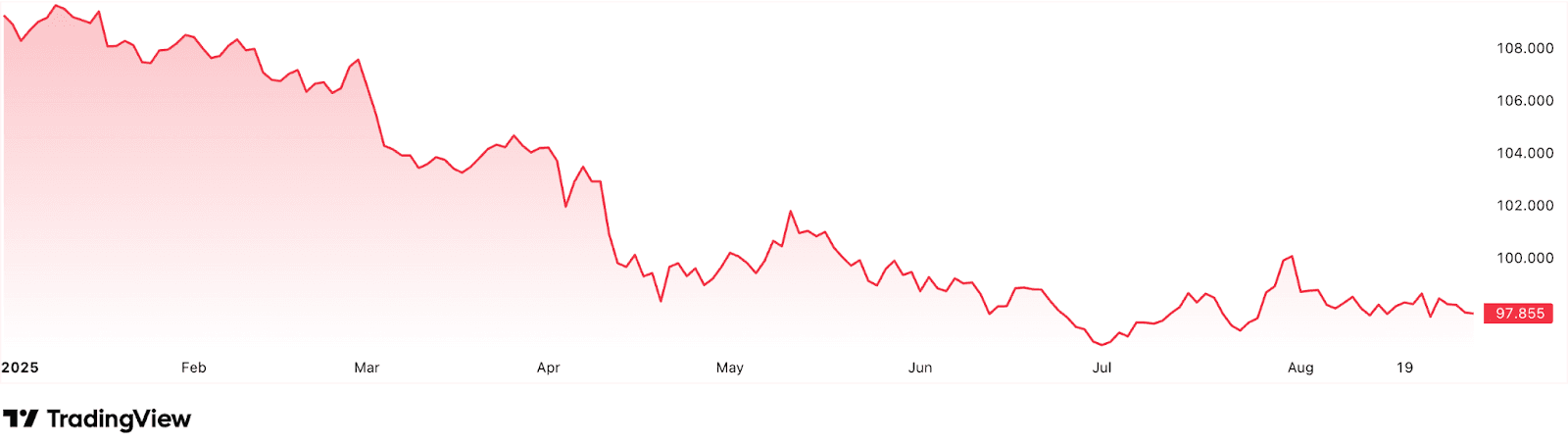

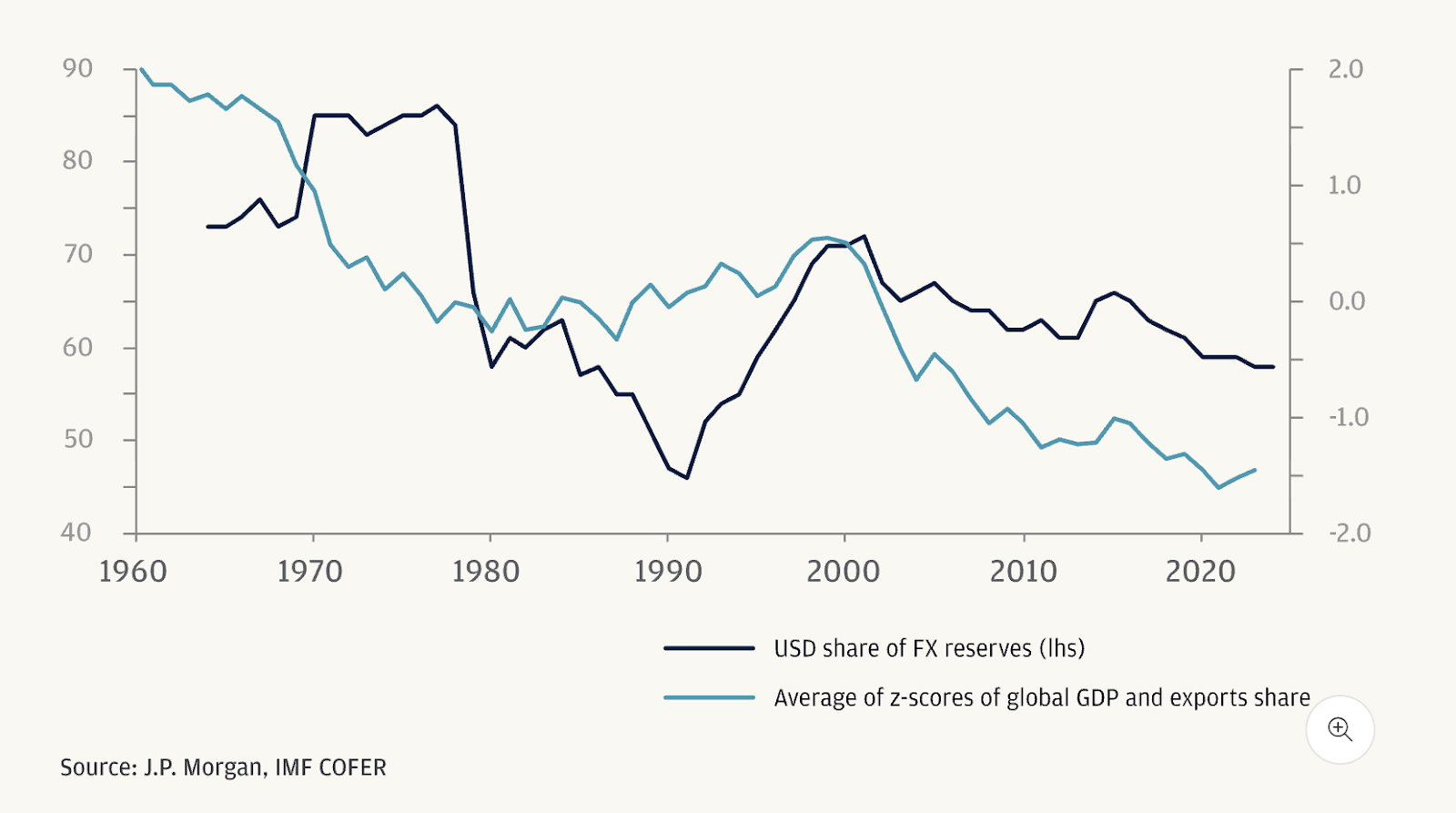

The dollar index has fallen 9.8% year to date, despite a 6% gain over the past five years as of August 30, 20252. At the same time, its share within global Foreign Exchange (FX) Reserves has also narrowed steadily, moving from 65% (2016) to 57% (2024)3. The shifting mood is visible, and it is time to explore the reasons behind why the USD is falling.

Source: Trading View4

1. Why Dollar Is Falling?

- U.S. Policy Uncertainty: Markets remain hypersensitive to political cues. In July 2025, a comment on removing Fed Chair Powell triggered a 1.2% slide within an hour6. Threats of 100% tariffs on nations trading outside the greenback system added to this policy whiplash, raising doubts about credibility.

- Ballooning U.S. Debt: By June 2025, national debt touched USD36.2 trillion against the GDP of USD30.3 trillion, a ratio of 119.4%7. This imbalance, worsened by fiscal measures such as the USD4.1 trillion OBBBA (One Big Beautiful Bill Act, suggests output is trailing obligations.

- Inflation Fears: Consumer prices increased 0.3% in June, a 3.5% annual pace, after a 0.1% gain in May8. Tariff-driven costs are feeding into essentials and imports, from apparel to furnishings. Audio-video equipment prices jumped 1.1% in June and 11.1% year on year, their largest rise on record. Such pressures erode trust in the dollar’s stability.

- Erosion Of The U.S. Exceptionalism: Projections for 2025 growth fell from 2.3% to 1.4%9. Inflows into U.S. equity ETFs shrank to USD5.7 billion from USD 10.2 billion a year earlier, while Europe drew USD42 billion. Capital is no longer anchored in the belief that American markets will consistently lead.

The dollar’s decline can be a temporary phenomenon. But clear signals suggest it could be part of a broader move toward de-dollarisation. Let us check.

2. Visible Signs Of De-Dollarisation

- Fixed Income/Bond Markets: Foreign ownership in American Treasuries (sovereign debt) has diminished. From holding more than 50% during the global financial crisis, overseas investors now account for barely 30% in early 202510. With yields across developed economies moving higher, Washington faces a heavier financing burden if demand continues to soften.

- Commodity Markets: Russian oil and coal are being settled in yuan or local currencies, with India, China, and Turkey among key participants. Even Saudi Arabia has explored yuan pricing for oil, while Bangladesh has used yuan to fund a nuclear project. Such moves capture the current mood of diversification away from the greenback.

As we have seen the reasons behind the US dollar crash, now consider what a weaker dollar could mean for the world economy.

Global Implications Of A Weaker Dollar

1. Impact On The U.S. Economy

A softer US dollar value can make American-made goods more attractive abroad, giving exporters some relief. Yet this advantage is offset when import bills climb, a trend magnified by tariff-driven costs. Inflationary concerns rise. Borrowing also grows more costly. Households then confront higher expenses, from furnishings to fuel, while borrowing expenses rise across mortgages and consumer credit. The Treasury also shoulders a heavier load, as servicing obligations grow costlier. These pressures, combined with questions about policy direction, challenge the currency’s role as a trusted safe haven.

2. Impact On Other Economies

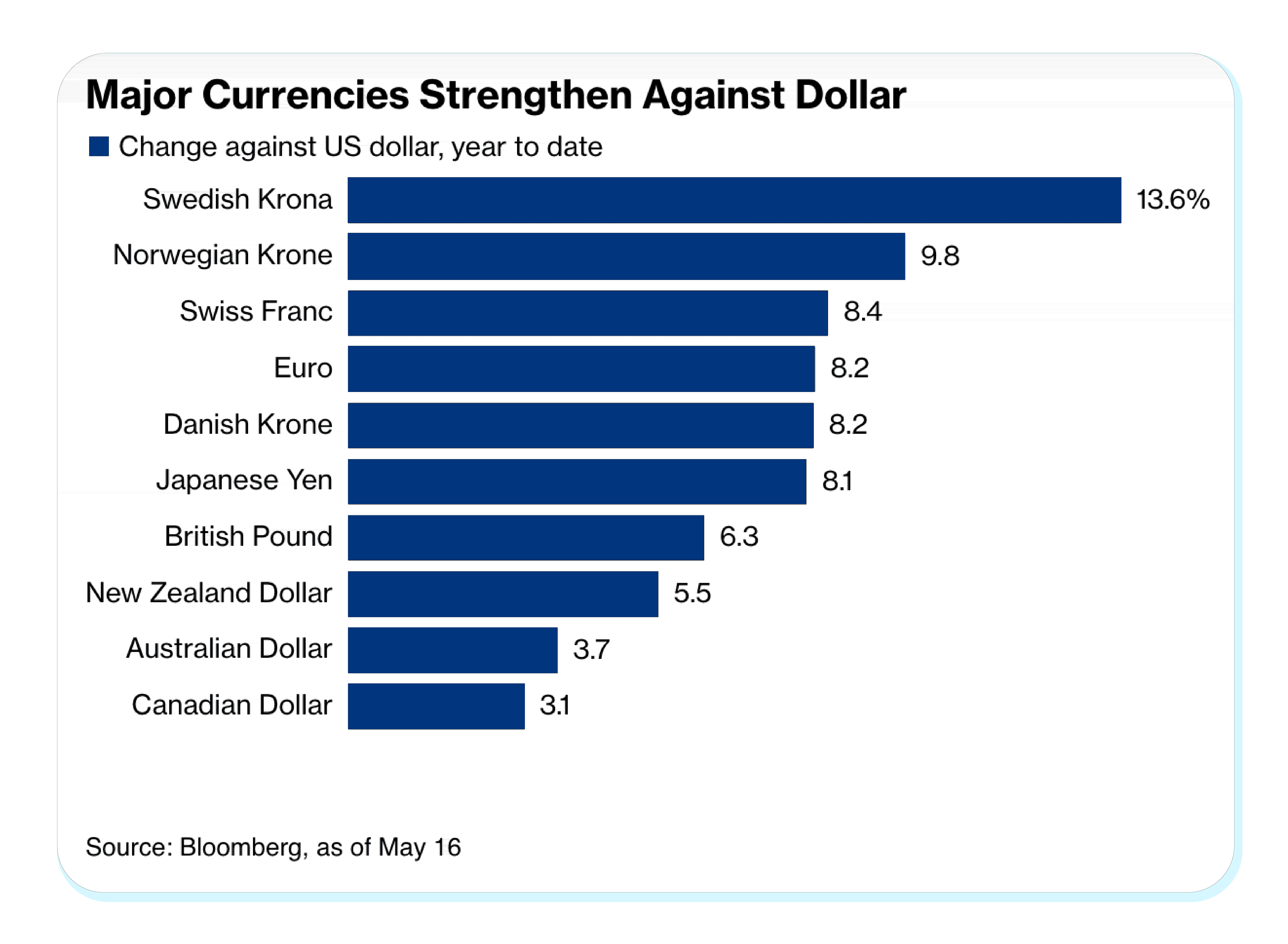

For other nations, the effects of the US dollar crash vary. It strengthens the position of major currencies like the euro and yen, attracting capital into European and Japanese bonds. Traditional hedges also benefit. Gold prices have climbed about 31% since the start of the year (as of 30 August), as global investors diversified away from dollar assets11. Emerging markets, meanwhile, remain unevenly exposed. Dollar deposits across 18 countries have reached roughly $830 billion, with Latin America showing the highest reliance12. Here is how major currencies have moved against the U.S. dollar YTD ( as of May 16, 2025).

Let us now focus on the benefits the Indian economy gains from watching de-dollarization closely.

India's Position: A Beneficiary In The De-Dollarization Trend

The INR recently breached 88 per USD, marking a record low after Washington doubled duties on Indian shipments to 50%14. This decline highlights India’s vulnerability to external shocks, setting the context for why reduced reliance on the reserve currency matters.

A weaker U.S. currency eases the import bill, especially for crude oil and high-value items like semiconductor tools, machinery, and electronics. Lower costs support inflation control and improve the current account balance. India also benefits from translation gains on its USD 717 billion in external liabilities, reducing repayment burdens when converted back into INR15.

Diversifying reserves away from a dollar-heavy structure adds another buffer. Allocating more into euros, yen, yuan, or gold reduces exposure and frees resources for growth-linked spending in infrastructure, technology, and industrial projects. This creates greater policy flexibility at home without being directly pulled by U.S. cycles.

Still, exposure to the United States is deep. Outsourcing contracts in IT, along with pharmaceuticals and textiles, rely on steady demand from American buyers. Weakness in the greenback threatens pricing power and could force renegotiation of deals. Overseas inflows, more than USD 129 billion in 2024, also risk losing value and straining household consumption in remittance-heavy states16.

The Enduring Strength And Future Of The Dollar

Despite current pressures, the “TINA” doctrine—There Is No Alternative—still shields the USD strength. Investors may question American fiscal management, but no rival currency yet matches the depth of U.S. capital markets, the scale of its economy, or the liquidity its assets provide. Gold and regional currencies have gained traction, but none offer the stability and global acceptance that the dollar commands.

Its transactional role confirms this dominance. Roughly 50% of international payments move through the USD17. Around 55% of cross-border loans and 60% of deposits remain denominated in the greenback, while nearly 60% of foreign currency debt is issued in dollars. In foreign exchange markets, the dollar is involved in nearly 88% of all trades. This breadth ensures that even amid volatility, the dollar retains its unrivalled position at the core of global finance.

Conclusion

Supremacy of the US dollar value is under strain, yet de-dollarization remains a distant prospect. For India and other emerging markets, this order signals both opportunity and risk, as diversification gains pace while the world still revolves around the greenback.

FAQs On Dollar Collapse

1. Is it true that the U.S. dollar is going away?

It continues to dominate global payments and reserves. What you see today is a gradual search for alternatives.

2. How much will 1 dollar be in Indian rupees in 2025?

On 1 January 2025, it was at 85.22, and by 29 August, it had moved to 87.30 against the INR18.

3. What is the future of USD vs INR?

The currency pair is likely to stay influenced by trade flows and monetary policy. Movements ahead will depend on growth trends and capital flows.

References:

1. US News, accessed from: https://money.usnews.com/investing/articles/de-dollarization-what-happens-if-the-dollar-loses-reserve-status

2. Trading View, accessed from: https://in.tradingview.com/symbols/TVC-DXY/?timeframe=YTD

3. IMF, accessed from: https://tinyurl.com/mhuf4698

4. Trading View, accessed from: https://in.tradingview.com/symbols/TVC-DXY/?timeframe=YTD

5. JP Morgan, accessed from: https://www.jpmorgan.com/insights/global-research/currencies/de-dollarization#section-header#3

6. JP Morgan, accessed from: https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/market-updates/on-the-minds-of-investors/where-is-the-us-dollar-headed-in-2025/

7. Pew Research, accessed from: https://www.pewresearch.org/short-reads/2025/08/12/key-facts-about-the-us-national-debt/

8. Reuters, accessed from: https://www.reuters.com/world/us/feds-inflation-fears-may-start-be-realized-with-june-cpi-data-2025-07-15/

9. JP Morgan, accessed from: https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/market-updates/on-the-minds-of-investors/where-is-the-us-dollar-headed-in-2025/

10 . JP Morgan, accessed from: https://www.jpmorgan.com/insights/global-research/currencies/de-dollarization#section-header#4

11. Money Control, accessed from: https://www.moneycontrol.com/commodity/international-gold-price?symbol=XAUUSD:CUR

12. JP Morgan, accessed from: https://www.jpmorgan.com/insights/global-research/currencies/de-dollarization#section-header#6

13. Bloomberg, accessed from: https://www.bloomberg.com/news/articles/2025-05-16/how-a-weaker-us-dollar-affects-the-economy

14. Reuters, accessed from: https://www.reuters.com/world/india/rupee-plunges-all-time-low-steep-us-tariffs-logs-4th-month-loss-2025-08-29/

15. Business Standard, accessed from: https://www.business-standard.com/india-news/india-s-external-debt-increases-10-7-to-717-9-billion-at-dec-end-125033100595_1.html

16. World Bank, accessed from: https://blogs.worldbank.org/en/peoplemove/in-2024--remittance-flows-to-low--and-middle-income-countries-ar

17. Federal Reserve, accessed from: https://www.federalreserve.gov/econres/notes/feds-notes/the-international-role-of-the-u-s-dollar-2025-edition-20250718.html

18. Mumbai Port, accessed from: https://mumbaiport.gov.in/show_content.php?lang=1&level=2&ls_id=1342&lid=1067

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks, including delay and/ or default in payment. Read all the offer-related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for the consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001