Digital Rupee In India (2026): Benefits, Use Cases And Future Impact

The Digital Rupee, India's Central Bank Digital Currency (CBDC), launched by the Reserve Bank of India (RBI) in December 2022, marks a significant milestone in the nation’s financial evolution (HDFC Bank, 2025). As of 2026, the Digital Rupee, or e-Rupee, continues to advance through pilot projects for both retail (CBDC-R) and wholesale (CBDC-W) transactions.

This blog analyses the benefits, use cases, and future impact of the Digital Rupee, examining its potential to transform India's economy while catering to the challenges, such as privacy and infrastructure.

Benefits Of The Digital Rupee

The Digital Rupee offers numerous advantages over traditional currency, aligning with India’s “Digital India” initiative:

- Cost Efficiency: Storing, Printing, and transporting physical currency incurs significant costs. The Digital Rupee eliminates these expenses, reducing financial burdens and contributing to environmental sustainability.

- Financial Inclusion: By enabling digital wallets that don’t require a bank account, the e-Rupee extends financial services to unbanked and underbanked populations, particularly in rural areas.1

- Real-Time Transactions: The Digital Rupee facilitates instant, secure payments, enhancing efficiency for consumers and companies2.

- Programmability: Features such as restricted usage for government grants ensure funds are used as intended, reducing fraud.

- Enhanced Security: Built on a secure platform, potentially blockchain, the e-Rupee minimizes risks of counterfeiting and fraud compared to physical cash.

Use Cases Of The Digital Rupee

The Digital Rupee is being tested across numerous applications, demonstrating its versatility:

- Retail Transactions (CBDC-R): Consumers can use the e-Rupee for everyday purchases, such as groceries or utility payments, through digital wallets integrated with payment gateways such as Razorpay3.

- Wholesale Transactions (CBDC-W): The RBI’s Negotiated Dealing System-Order Matching (NDS-OM) CBDC enables banks to settle government securities through delivery versus payment (DvP) mechanisms, streamlining financial operations.

- Cross-Border Payments: While in early stages, the e-Rupee's main motive is to facilitate faster and cheaper international remittances, reducing reliance on intermediaries.

- MSME Financing: Small and medium enterprises/businesses that benefit from quicker access to funds through digital transactions, which improves the cash flow and efficiency.

- Government Disbursements: Programmable features that allow the targeted delivery of subsidies or welfare payments, ensuring funds reach intended recipients.

Future Impact Of Digital Rupee

The Digital Rupee holds significant potential to transform India’s financial ecosystem by the year 2029-30, especially when India’s digital economy is projected to contribute one-fifth of national income (Press Information Bureau, 2025). The primary impacts include:

- Reduced Cash Dependency: With India’s cash propensity at 17% (cash withdrawn to GDP ratio), the e-Rupee could shift the economy toward digital payments, aligning with global trends.

- Enhanced Monetary Policy: The RBI can leverage the e-Rupee’s traceability and programmability to monitor transactions and combat illicit activities, improving financial governance.

- Global Competitiveness: Internationalizing the Rupee through cross-border CBDC pilots could strengthen India’s position in global trade.

- Challenges to Address: Privacy concerns, cybersecurity risks, and the need for robust digital infrastructure remain critical hurdles. Balancing anonymity and traceability is essential for adoption.

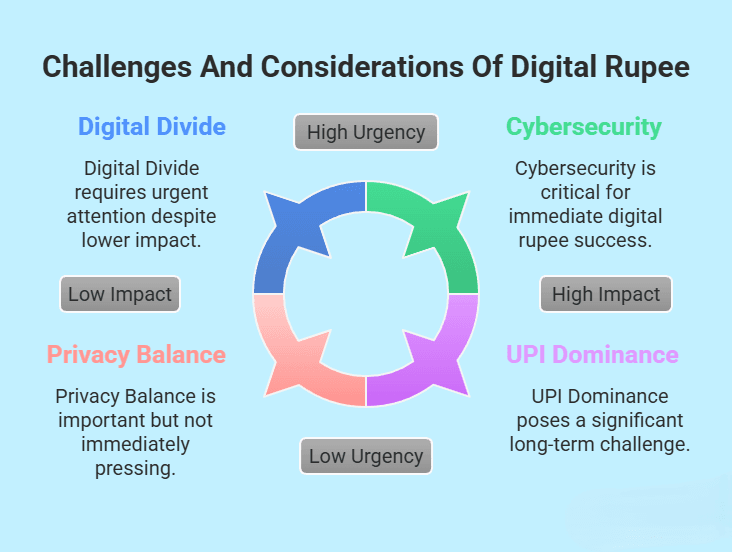

Challenges And Considerations Of Digital Rupee

Despite its promise, the Digital Rupee faces challenges:

- Digital Divide: Limited internet access and digital literacy in rural areas may hinder adoption.

- Cybersecurity: Robust safeguards are needed to protect against hacks, especially for cross-border transactions.

- Competition With UPI: The Unified Payments Interface (UPI) dominates digital payments in India, with the e-Rupee accounting for only a small fraction of transactions as of late 2024. Incentivizing adoption is crucial.

- Privacy: Balancing anonymity for low-value transactions with traceability for regulatory purposes requires careful data management.

Data Table: Key Metrics Of The Digital Rupee

Metric | Details |

Launch Date | December 2022 (Retail and Wholesale Pilots) |

Participating Banks | SBI, HDFC, ICICI, HSBC, Kotak Mahindra, Bank of Baroda, Yes Bank, etc. |

e-Rupee Usage (2024) | Small fraction of the total banknotes in circulation |

Projected Digital Economy Contribution | One-fifth of the national income by 2029-30 |

Conclusion

The conclusion says that Digital Rupee is poised to redefine India’s financial landscape by promoting efficiency, inclusion, and innovation. Its benefits, such as cost savings and real-time transactions, and diverse use cases, from retail payments to cross-border transfers, underscore its potential. Moreover, addressing challenges like digital infrastructure and privacy concerns is critical for widespread adoption.

As India advances toward a digital economy, the e-Rupee could play a pivotal role in shaping a more inclusive and resilient financial future.

Login to Grip Invest to explore innovative, future-ready investment options beyond traditional assets and be part of India’s evolving digital financial ecosystem.

Frequently Asked Questions On Digital Rupee

1. What is the Digital Rupee, and how does it work?

The Digital Rupee is India’s central bank digital currency (CBDC), issued by the RBI. It works like physical cash but in digital form, enabling secure, real-time transactions via wallets and mobile apps.

2. How is the Digital Rupee different from UPI?

Unlike UPI, which transfers money between bank accounts, the Digital Rupee is actual legal tender, just in digital form. It doesn't need intermediaries like banks for peer-to-peer transfers.

3. What are the key benefits of using the Digital Rupee?

Benefits include lower cash handling costs, real-time payments, better financial inclusion for the unbanked, secure transactions, and programmable features for targeted subsidies or grants.

4. Can I use the Digital Rupee for everyday purchases?

Yes, the retail version of the Digital Rupee (CBDC-R) can be used for daily transactions like shopping or paying bills using compatible digital wallets.

References:

1. HDFC Bank accessed from: https://www.hdfcbank.com/personal/useful-links/quick-links/digital-rupee

2. Forbes, accessed from: https://www.forbes.com/sites/digital-assets/2025/03/10/a-2025-overview-of-what-you-need-to-know-about-the-digital-rupee/

3. Razor Pay, accessed from: https://razorpay.com/blog/the-e-rupee-and-what-it-means/

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001