Rule Of 72 Explained 2026: Formula, Examples And Double Investment Fast

The Rule of 72 can be an efficient tool in the dynamic landscape of personal finance, where complex calculations and projections can seem intimidating. This useful mathematical tool enables Indian investors to rapidly calculate how long it would take to double the investment.

The Rule of 72 is a simple method for evaluating prospective growth, whether across assets like bonds, mutual funds, fixed deposits, etc.

This blog decodes the Rule of 72 through the Rule of 72 formula, definition, sub-types and more to aid informed investing and planned growth.

Understanding The Rule Of 72

What Is The Rule Of 72?

The Rule of 72 is a financial formula used to estimate the time required for an asset to double the investment made at a constant, compound interest rate. This compound interest rule of 72 offers a quick approximation of the anticipated returns, without intricate computations.

The Rule of 72 formula is simple and can be used quickly. Investors need to simply divide the number 72 by the annual interest rate (or the expected rate of return) to obtain a rough estimate of the number of years it will take for your investment to grow to twice its initial value. The Rule of 72 formula below estimates the investment doubling time.

Rule of 72 formula = 72Rate of interest

The Rule of 72 example below explains the formula more.

The investment of Mr A earns a consistent 6% annual return. He can use the Rule of 72 formula and divide 72 by 6. The result implies that it would take 12 years to double the investment.

This straightforward compound interest rule of 72 is grounded in the mathematical principles of compound interest and is derived from the natural logarithm of 2, which is approximately 0.693. While the Rule of 72 provides the most accurate approximations for interest rates falling between 6% and 10%, it remains a dependable and useful guideline for a broader range of rates as well to calculate the investment doubling time.

Why Use The Rule Of 72 In Personal Finance?

In India, the Rule of 72 is a practical technique for simplifying intricate investment calculations, where financial literacy is on the rise. It empowers everyday investors to easily compare options such as fixed deposits (FDs) with reliable returns or mutual funds with fluctuating growth, without relying on calculators or complex financial tools or techniques.

This rule raises informed decision-making and sparks discussions about long-term wealth-building, supporting India’s growth that mainly focuses on attaining financial independence.

Also Read: Learn About The 8-4-3 Rule Of SIP

Rule Of 72 Vs Rule Of 69 Vs Rule Of 114

One common way to estimate how long it will take for an investment to double is by using the Rule of 72, which takes into account the rate at which the investment will compound. There are other methods available for estimating the amount of time it will take to double an investment, such as the Rule of 69, which applies to investments that are compounded continuously, and the Rule of 114, which estimates the amount of time it will take for depreciation or inflation to decrease an investment by half.

The Rules of 72, 69, and 114 each have their own application in determining how long it will take for an investment to grow due to compounding. Comparing the relationships of these three methods will help improve the application of each method to an investment growth calculation and will provide a greater degree of accuracy to the examples of compounding power across different financial metrics.

Each of these rules has its own unique applications depending on how frequently your investment is compounded and what you are trying to accomplish through the growth of your investment, which will, in turn, sharpen the calculation of the overall growth of your investment.

1. Rule of 72 for Annual Compounding

You can estimate the amount of time it will take for an annual investment to double by using the Rule of 72, which divides 72 by the interest rate earned on the annual investment. The Rule of 72 is an easy way and can be used as a guideline in estimating the power of compounding when calculating example investments.

2. Rule of 69 for Continuous Compounding

When investing, many sophisticated models use continuous compounding, which uses the Rule of 69. The Rule of 69 divides 69 by the interest rate earned to calculate the doubling time of an investment, making it slightly quicker than the Rule of 72. Thus, the Rule of 69 is used to calculate the investment growth of derivatives and reinvested dividends.

3. Rule of 114 for Halving Periods

Using the 114 to find an interest rate method to construct another through determining the time to reach the value of half, using 114 divided by a rate can also be used for losses, inflation, etc. Therefore, when used in conjunction with the Rule of 72, you can obtain a complete array of tools to show the comparative effects of the total compounding power when creating your plans.

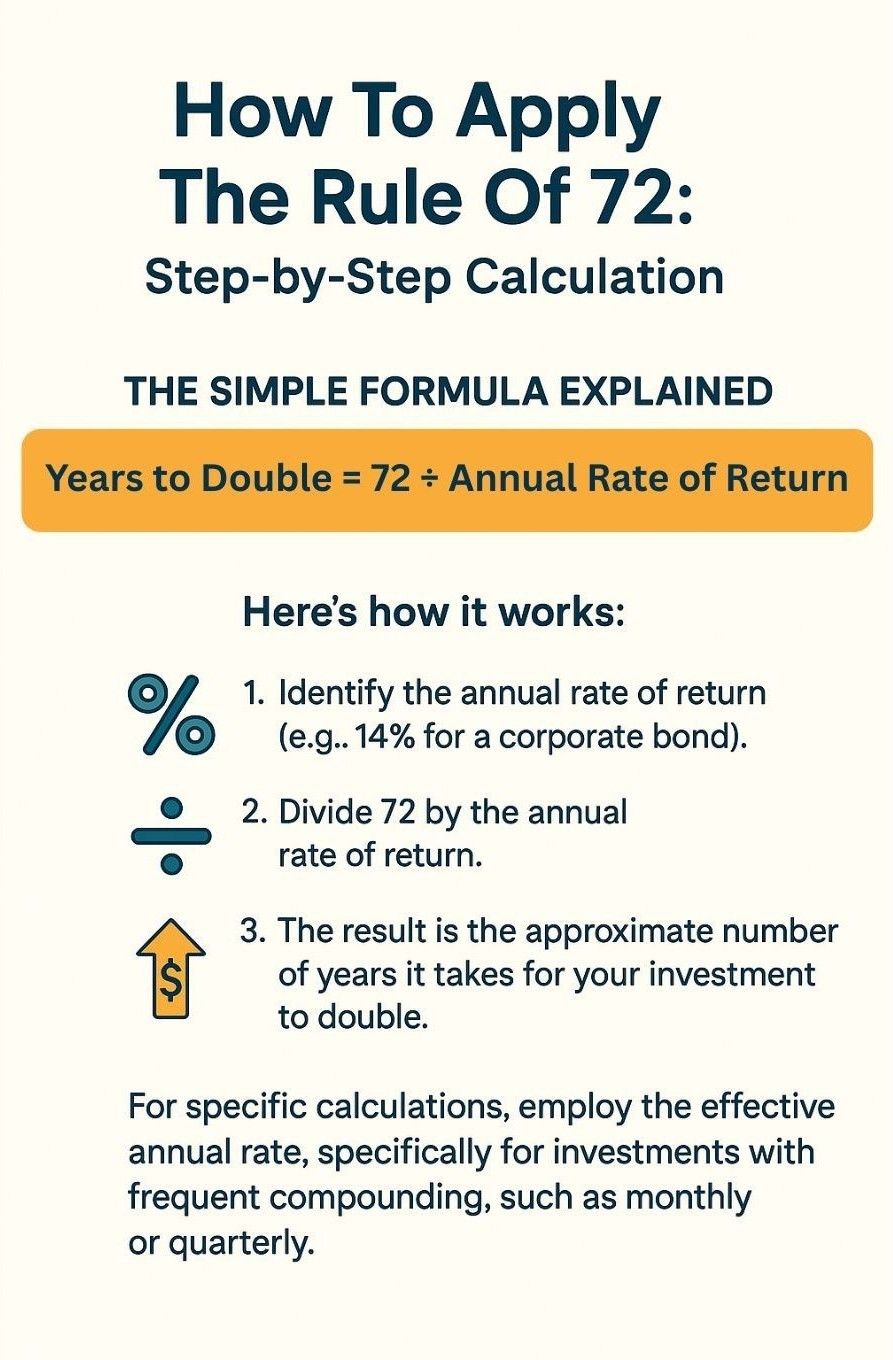

How To Apply The Rule Of 72: Step-by-Step Calculation

The Simple Formula Explained

The Rule of 72 formulas is very simple:

Years to Double = 72 ÷ Annual Rate of Return

Here is how it works:

- Identify the annual rate of return (e.g., 14% for a corporate bond).

- Divide 72 by the annual rate of return.

- The result is the approximate number of years it takes for your investment to double.

For specific calculations, employ the effective annual rate, specifically for investments with frequent compounding, such as monthly or quarterly. The rule, developed on the basis of continuous compounding, provides a close approximation instead of an exact value1.

Practical Examples: Doubling Your Investment

Let us apply the Rule of 72 to a hypothetical scenario-

Suppose you invest INR 1,00,000 in a corporate bond offering a 14% annual return, compounded annually.

- Calculation: 72 ÷ 14 = 5.14 years

- Result: Your INR 1,00,000 will grow to INR 2,00,000 in approximately 5.14 years.

Now, consider a mutual fund with an expected return of 12% per year:

- Calculation: 72 ÷ 12 = 6 years

- Result: The same INR 1,00,000 would double to INR 2,00,000 in about 6 years.

For a fixed deposit at 7%:

- Calculation: 72 ÷ 7 = 10.29 years

- Result: Your investment doubles in just over 10 years.

These examples highlight how the Rule of 72 helps compare investment options.

Rule of 72 vs. Other Investment Thumb Rules

The Rule of 72 is not the only thumb rule in personal finance. Let us compare it with two popular ones: the 100 Minus Age Rule and the 50:30:20 Rule2.

| Thumb Rule | Purpose | Formula/Method | Use Case |

| Rule of 72 | Estimates time to double an investment | 72 ÷ Annual Rate of Return | Comparing investment growth |

| 100 Minus Age Rule | Guides asset allocation | 100 – Your Age = % in Equities | Balancing risk in portfolio |

| 50:30:20 Rule | Budgeting framework | 50% Needs, 30% Wants, 20% Savings/Investments | Managing monthly finances |

100 Minus Age Rule: This suggests allocating a percentage of your portfolio to equities based on your age (e.g., at 30, invest 100 – 30 = 70% in equities). It is useful for risk management but does not address growth timelines like the Rule of 723.

50:30:20 Rule: This budgeting rule allocates 50% of income to needs, 30% to wants, and 20% to savings or investments. It is great for financial discipline but does not estimate investment growth4.

The Rule of 72 shines for its focus on growth timelines, making it ideal for long-term planning.

When The Rule Of 72 Becomes Less Accurate

The Rule of 72 is accurate only for moderate compounding rates when estimating multiple investment values over the short- and long-term for determining nears, and how often yields are produced at these rates.

The Rule of 72 works best with yields that yield between 6% and 10%; however, deviations increase as yields become higher than 20% or lower than zero percent. These deviations result in considerable discrepancies in how the logarithmic roots are calculated for true investment value.

Frequent compounding creates further changes in how estimated investment returns are derived, so modifications to the example works created to illustrate the effects of the compounding power should be completed. Being aware of these fluctuations will help you use these examples effectively, and as such, use a compounding calculator when assessing any significant financial decision, instead of just visualizing the numbers; you need to visually calculate them as well.

1. Extreme Interest Rates

With extremely high rates, the Rule of 72 overestimates doubling times of investment value because compounding is more effective and thus moves compound interest returns away from true exponential curves.

2. Low Interest Environments

At rates of near zero percent, the Rule of 72 does not give reliable investment return estimates due to the extreme amount of time calculated for doubling periods. Because of this, the use of precise tools and accurate input calculations should continue over simplified methods for calculating an estimated multiple of an investment return.

3. Variable Compounding Frequencies

Doubling time of an investment can be reduced further using daily compounding rather than annually compounded by the Rule of 72. This means that we must make adjustments to scenarios that show examples of how compounding works in order to be accurate.

Using The Rule Of 72 To Understand Inflation Impact

Similar to the mutual funds Rule of 72, another variation of the Rule of 72 helps guide inflation impact computation. It is called the inflation Rule of 72. Under this formula, investors calculate how long it will take for their investment to be at ½ its value in terms of purchasing power, given a particular inflation rate. Investors can understand the returns they need to generate to balance the diminishing impact of inflation.

Explained below is how the inflation Rule of 72 works.

1. Real vs Nominal Returns

Before applying the Inflation Rule of 72 to determine the true amount of time it will take for an investment to double, you should subtract inflation from yields, as nominal growth alone can mislead you in using the Rule of 72 for calculating growth due to the impact of how much prices keep rising over time.

For example, if the return from an asset is 8% and inflation is at 2%, the real return becomes 6%. Then, according to the inflation Rule of 72, the amount doubles in 12 years.

| Years required for an amount to double if the interest is 8% (without accounting for inflation) | 9 Years |

| Years required for an amount to double if the interest is 6% (after accounting for inflation) | 12 Years |

Therefore, the inflation Rule of 72 shows how the real value grows, after accounting for inflation, takes longer.

2. Inflation Doubling Time

You may also use the Rule of 72 to calculate how long it will take for inflation to cut your money's purchasing power in half. For instance, prices would approximately double in 12 years (72 ÷ 6 = 12) at a 6% inflation rate, implying that the same amount of money would only purchase nearly half as much as it does now. This illustrates the significance of investing in assets that may yield returns higher than the rate of inflation and take advantage of compounding.

3. Hedging Inflation Risks

Investors can determine if their assets are growing quickly enough to beat inflation by using the Rule of 72. Over time, real purchasing power may be preserved and increased if an investment doubles in value faster than inflation doubles prices. Since they have the potential to produce long-term returns that outpace inflation, assets like stocks and other growth-oriented investments are frequently employed for this purpose.

Rule Of 72 For Debt And Loan Interest

The application of the Rule of 72 applies to debt as well; the Rule of 72 can help to estimate how long it will take for a debt to double, based on the Rule of 72 applying to compounding interest with loans or other types of loans where interest accumulates.

By viewing how quickly an unpaid balance (debt) will grow, you can better prepare a plan to pay off the amount owed, and by flipping the growth calculation of investments to that of liability, you will have a powerful tool for managing the amount of time needed to reach your financial goals. The Power of Compounding serves to highlight the critical importance of paying off obligations quickly or refinancing, thereby promoting good practices in both saving and borrowing.

1. Loan Balance Doubling

High-interest unpaid credit card debt can increase rapidly due to compounding through the Rule of 72, motivating individuals to quickly reduce their total debt.

2. Mortgage Payoff Insights

With regards to long-term loans, the amount of time it would take for your original investment to double when considering both principal and interest will be slower than with a shorter-term loan (e.g., less than ten years). Thus, as interest rates decrease, the Rule of 72 provides opportunities for borrowers to refinance their mortgages for the purpose of maximizing investment growth by increasing their cash flow.

3. Debt Snowball Warning

The example of compounding in reverse illustrates how quickly small amounts of debt can become large amounts of debt over time. Therefore, in order to establish financial independence more quickly, it is best to pay off your highest interest rate debts first. This can be accomplished through the Rule of 72.

Using The Rule of 72 In Indian Investments

Estimating Returns for Mutual Funds, FDs, and Bonds

India’s investment landscape is diverse, from mutual funds to fixed deposits and bonds.

The Rule of 72 helps evaluate these options:

1. Mutual Funds: Equity mutual funds in India have historically delivered 10–15% annualized returns (e.g., large-cap funds averaged 12.5% over the past decade, per AMFI data [4]). At 12%, your money doubles in 6 years (72 ÷ 12).

2. Fixed Deposits: FDs offer 6–8% returns (e.g., SBI FD rates for 5 years were 6.5% in 2024)5. At 7%, doubling takes 10.29 years.

3. Corporate Bonds: High-quality corporate bonds may offer 10–14% returns6. At 14%, doubling happens in 5.14 years, as shown earlier.

Impact of Compounding: Why It Matters

Compounding is the magic behind the Rule of 72. In India, where inflation averages 5–6% (RBI data, 2024)7, compounding helps your investments outpace rising costs.

For example, an INR 1,00,000 investment at 12% doubles to INR 2,00,000 in 6 years, and with continued compounding, it could grow to INR 4,00,000 in another 6 years. This exponential growth is why long-term investments are powerful.

Spotlight On Alternative Investments

Beyond traditional options, there is an alternative investment like those offered by platforms such as Grip Invest provides diversified returns. Grip offers curated investment opportunities in bonds and structured debt, often yielding 10–14% [8]. By utilizing the Rule of 72, a 12% return from such an investment doubles your money in 6 years, making it a convincing option for portfolio diversification.

Advanced Applications Of The Rule Of 72

The Rule of 72 has several advanced applications in retirement planning, portfolio allocation, budgeting, and more. Let us decode some of them.

Rule of 72 for Retirement Planning: How Much to Save at Age 30, 40, 50

The number of times your retirement savings will double until you retire may be estimated using the Rule of 72, which directly explains how much you need to save now. For example, Mr P wants to reach INR 2 crore by 60 years of age. If his portfolio earns an average return of 7.2%, the period required to double an investment as per the Rule of 72 becomes 10 years. The table below illustrates how investment differs with age.

| Starting age | Years left to retire at 60 | Doubling periods (Years to Retire / 10) | Required starting corpus (Future value / 2 ^ no. of doublings) |

| 30 Years | 30 Years | 3 doublings | 25 lakhs |

| 40 Years | 20 Years | 2 doublings | 5 lakhs |

| 50 Years | 10 Years | 1 doublings | 10 lakhs |

This illustrates the power of compound interest over time by showing that starting at age 30 requires 4 times less than the amount required to start at age 50.

Rule of 72 vs 100 Minus Age Rule: Which Is Better for Portfolio Allocation

The table below explains the difference between the Rule of 72 and the 100 Minus Age Rule.

| Parameter | Rule of 72 | 100 Minus Age Rule |

| Purpose | Estimate the time required to double the investment | Guides debt and equity allocation based on age |

| Formula | 72 / Return Rate = Time to Double Investment | 100 - Age = % Equity Allocation |

| Example | If K invests INR 1,00,000 at 8% interest, it will become INR 2,00,000 in 9 years

72 / 8% = 9 | Mr K is 30 years old and wants to determine asset allocation 100 - 30 means 70% allocation in equity and 30% in debt |

The Rule of 72 and 100 Minus Age rule complement each other, rather than competing. Investors can determine the return rate required to double their investments within the desired timeframe, using the Rule of 72. Then, based on the return rate target set, investors can diversify their funds, based on their age, into equity and debt assets with the help of the 100 Minus Age Rule.

Rule of 72 vs 50:30:20 Rule: Growth Timeline vs Budgeting Discipline

The table below explains the difference between the Rule of 72 and the 50:30:20 Rule.

| Parameter | Rule of 72 | 50:30:20 Rule |

| Purpose | Explains the investment growth timeline | Ensures budgeting and discipline in finance |

| Formula | 72 / Return Rate = Time to Double Investment | 50% of net income after tax to needs, 30% to wants, 20% to debt and savings |

| Timeframe | Years to decades | Monthly |

50:30:20 guarantees that you will regularly save aside 20% of your monthly income. Subsequently, the Rule of 72 can be employed to choose assets based on the tenure required for the investment to double.

5 Common Rule of 72 Mistakes That Lead to Wrong Calculations

Financial rules are rarely absolute due to the dynamic environment in which they operate. Not accounting for the intrinsic nature of assets and their category, while using a financial rule to judge investability, can result in error. Discussed below are some of these situations.

1. Using a Decimal Rather Than a Percentage for the Interest Rate: The most common error is dividing 72 by the interest rate as a decimal (e.g., 0.08) rather than as a percentage (e.g., 8). In the formula, R is the percentage interest rate. This error results in estimates of doubling time that are 100 times too great.

- Accurate computation: 72 ÷ 8 equals 9 years to double at 8%

- Inaccurate computation: 72 ÷ 0.08 = 900 years

2. Using the Rule for Investments with Simple Interest: The Rule of 72 does not apply to simple interest investments; it only applies to compound interest investments. It is sometimes used incorrectly to savings accounts, bonds, or fixed deposits that solely compute interest on the initial principal.

3. Using It Outside the Interest Rate Range of 6% to 10%: With a peak accuracy of 8%, the Rule of 72 is best used for interest rates between 6% and 10%. The error rises dramatically outside of this range. Investors can use the Rule of 69 or the Rule of 70 for more accuracy when dealing with extremely low rates that are less than 6%. They can also adjust the numerator higher for really high rates (over 10%). For example, use 76 for rates above 20%. Often, investors change 72 by 1 for every 3 percentage points deviation from 8%.

4. Ignoring Various Compounding Frequencies: Annual compounding is implicitly assumed by the Rule of 72. The actual doubling time is somewhat less than what the rule predicts when investments compound more monthly, quarterly, etc.

5. Taking it Too Literally for Dynamic Interest Environments: Although real-world assets like stocks, bonds, and equity mutual funds have variable returns, the Rule of 72 implies a constant, stable yearly rate of return. The rule is no longer applicable for exact computations if the interest rate changes for any reason. Therefore, in the case of assets with varying interest, the 72 rule should be taken as an indication.

Apart from the Rule of 72, there are other assets as well. Let us compare the Rule of 69 vs 72.

Conclusion

The Rule of 72 is a straightforward formula that simplifies investing for Indian investors. It offers an easy way to calculate how fast your money can grow in options like mutual funds, fixed deposits, bonds, or other assets. After implementing this rule of 72, you can make informed decisions, align your investments with your financial objectives, and harness the benefits of compounding.

Whether you are a beginner or a seasoned investor, the Rule of 72 is a valuable tool for effective financial planning in India’s vibrant economy.

FAQs On The Rule of 72

References

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001