Top 11 Thumb Rules For Smarter Investments In 2026

They say, “The best time to plant a tree was 20 years ago. The second best time is now.”

This philosophy applies to investment planning in India as well. A sound investment strategy prioritises starting the investment journey early and maintaining disciplined, long-term investments, rather than chasing quick, high-risk returns.

Experienced investors often adhere to certain standard rules and norms to curate their portfolios and investment strategies.

These investment strategies in India are a must-know for any prospective or current investor in the Indian markets. While these norms are not absolute, they set standards that can help guide decisions. Therefore, this blog decodes key thumb rules of investing, suited to the Indian markets, like the 100 minus age rule, the rule of 72 investing, and more.

The time-tested formulas can complement informed investing if deployed after thorough research and understanding.

Top 11 Thumb Rules For Smarter Investments In 2026

1. The 50:30:20 Rule for Budgeting

The crux of investment strategies in India is building an optimal budget. Without efficient budgeting, investors will not be able to carve out a sufficient corpus for investing and wealth creation. The 50:30:20 rule offers a framework that can help individuals build a suitable budget by distributing their total post-tax income into three key buckets.

According to the 50:30:20 rule rule, individuals can allocate 50% of their post-tax income to necessities and needs, like groceries, electricity bills, and so on, while 30% of it can go towards wants, like dining out, entertainment, etc. The remaining 20% is for savings and investments. It is this 20% of the post-tax income that helps build wealth over the long term.

Investors can automate the investment of this 20% of their post-tax income by setting an autopay or by opting for a Systematic Investment Plans (SIPs), such that the amount gets debited automatically for investing into preferred assets like mutual funds, corporate bonds, etc. For example, if Mr K has a post-tax income of INR 1,00,000, the pie-chart below shows their budgetary allocation according to the 50:30:20 rule.

2. Rule of 72 (or 76): Estimate Doubling Time

Understanding how quickly your money can grow is essential for long-term planning. The Rule of 72 helps you estimate how long it will take for your investment to double.

Simply divide 72 by your expected annual rate of return. For example, at an 8% return rate, your money would double in approximately 9 years (72 ÷ 8 = 9).

For more precise calculations with higher return rates, some financial advisors recommend using 76 instead of 72. This is one of the best thumb rules for investing 2026.

| Rate of Return | Years to Double (Rule of 72) |

| 4% | 18 years |

| 6% | 12 years |

| 8% | 9 years |

| 10% | 7.2 years |

| 12% | 6 years |

This rule of 72 explained helps visualize the long-term impact of different investment options and reinforces the importance of seeking higher returns for long-term goals.

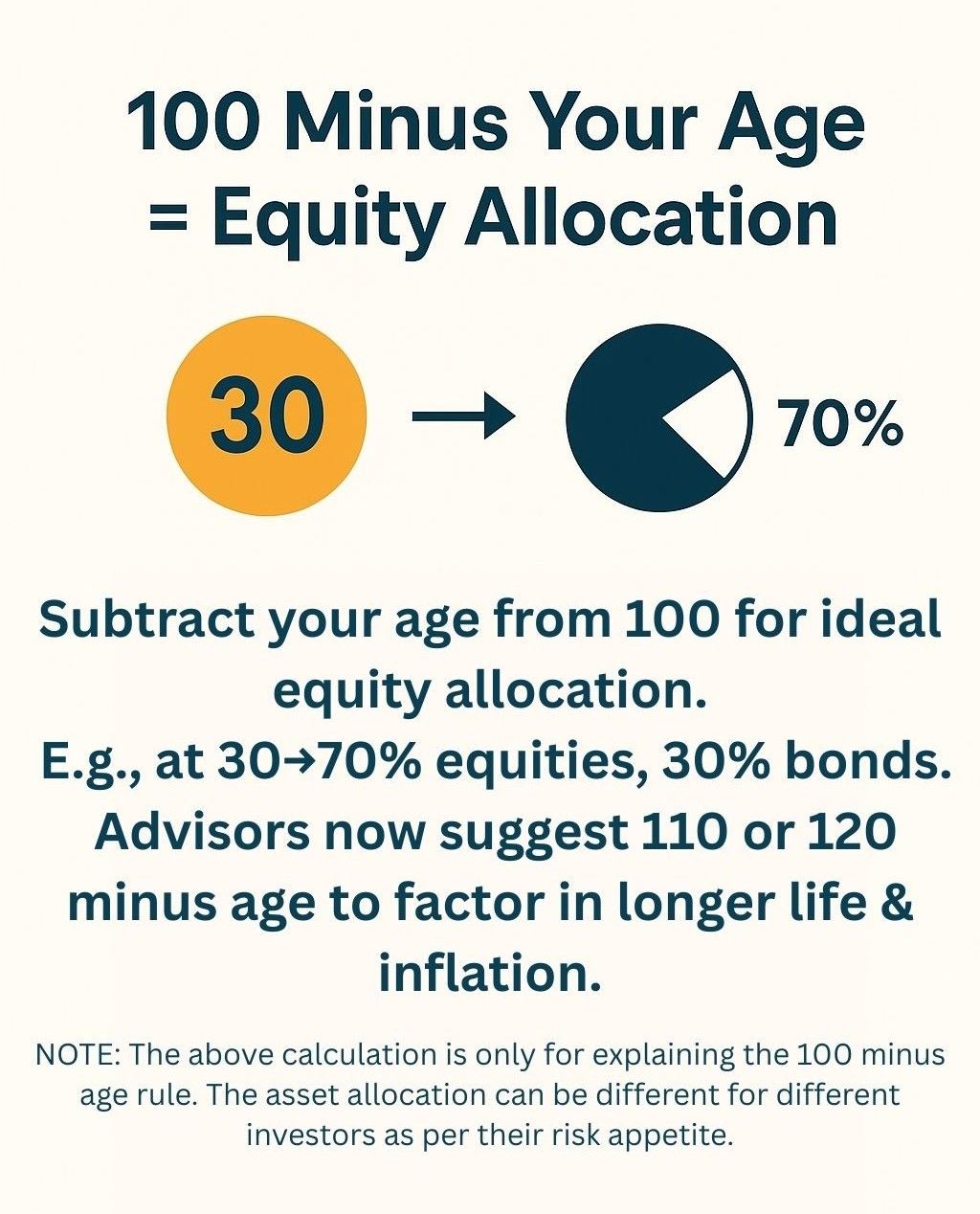

3. 100 Minus Your Age = Equity Allocation

The 100 minus your age rule provides a starting point for determining how much of your portfolio should be invested in equities.

Subtract your age from 100, and the result suggests your ideal equity allocation. For instance, a 30-year-old would allocate 70% to equities and 30% to safer investments like bonds.

This rule acknowledges that younger investors can afford to take more risks with a longer time horizon to recover from market downturns. As you age, the allocation gradually shifts toward more conservative investments.

Many modern financial advisors suggest updating this to "110 minus your age" or even "120 minus your age" to account for increased life expectancy and the need for growth to combat inflation.

4. Emergency Fund Rule

The standard emergency fund rule India recommends maintaining 6-12 months of essential expenses in highly liquid assets.

This financial buffer protects your investment strategy during unexpected situations like medical emergencies, job loss, or major repairs. Without this safety net, you might be forced to liquidate investments at inopportune times, potentially realizing losses.

You can keep these funds in high-yield savings accounts or short-term fixed deposits for easy access while earning some interest.

5. SIP Rule: Invest at Least 10% of Income

For consistent wealth accumulation, the SIP rule suggests investing a minimum of 10% of your income through Systematic Investment Plans. This disciplined approach leverages rupee-cost averaging, where you purchase more units when prices are low and fewer when prices are high.

You can maintain a 7+ year investment horizon, diversify across 5 areas including quality, value, growth, mid/small cap, and global, prepare for the 3 phases of investment cycles: disappointment, irritation, and panic, and increase your SIP amount every 1 year.

6. Debt vs Equity Rule: 60:40 for Conservative Investors

The traditional 60:40 portfolio rule suggests allocating 60% to equities and 40% to fixed-income investments for a balanced approach. Conservative investors might prefer this allocation to minimize volatility while still generating reasonable returns. However, this is not a fixed asset allocation thumb rules.

Within the fixed-income portion, consider diversifying across corporate bonds. These options provide predictable cash flows while offering potentially higher yields than government securities.

Corporate bonds from established companies can offer yields 1-3% higher than comparable government securities, making them attractive for income-focused investors.

7. Loan EMI Rule: Keep it Under 40% of Income

The loan EMI rule emphasises maintaining total EMI payments below 40% of your monthly income. Exceeding this threshold can severely restrict your ability to invest and build wealth.

This includes all loans: home, vehicle, personal, and credit card payments. If your EMIs exceed 40%, prioritize debt reduction before increasing investments.

Many successful investors follow a stricter 30% EMI limit to maintain greater financial flexibility and increase their investment capacity.

8. Retirement Corpus Rule: 20x Annual Expenses

The retirement corpus rule suggests accumulating at least 20 times your annual expenses to ensure a comfortable retirement. This multiplier accounts for inflation and provides a sustainable withdrawal rate.

For example, if your current annual expenses are INR 12 lakh, aim for a retirement corpus of at least INR 2.4 crore. This target assumes a conservative withdrawal rate and accounts for inflation-adjusted expenses.

This rule works in conjunction with the 4 percent withdrawal rule India, which suggests you can safely withdraw 4% of your retirement corpus annually without depleting your principal over a 30-year retirement period.

9. Insurance Rule: 10x Your Annual Income

The insurance rule recommends coverage of at least 10 times your annual income.

For example, if your annual income is INR 15 lakh, consider a life insurance coverage of at least INR 1.5 crore. This ensures your family can maintain their lifestyle and meet financial obligations in your absence.

Term insurance is the most cost-effective option for this purpose, offering high coverage at affordable premiums compared to endowment or unit-linked insurance plans. This is one of the best investment planning tips 2026.

10. Diversification Rule: Never Keep All Eggs in One Basket

The diversification rule remains one of the most fundamental principles of investing. Spreading investments across various asset classes, sectors, and geographies reduces risk and smooths out returns.

Modern portfolio theory suggests that proper diversification can optimize returns for a given level of risk. You can consider the 10 5 3 rule investment, which says, historically, equities have delivered around 10%, bonds about 5%, and cash equivalents approximately 3% over the long term.

11. 4% Withdrawal Rule for Retirement

While the 20x rule states the amount of retirement corpus an investor must strive to build before they retire, the 4% withdrawal rule states the amount of money an investor can withdraw from the fund post-retirement.

According to the rule, investors can withdraw 4% of their total retirement corpus in the first year, and then increase subsequent yearly withdrawals according to the inflation rate. In doing so, the rule assumes that the corpus can last around 30 years. Furthermore, it is important to note that the corpus left after withdrawal should remain invested so that they continue to grow with returns.

For instance, if Mr P has a retirement corpus of INR 1 crore, he can withdraw INR 4 lakhs in the first year. Now, in the second year, if the inflation rises by 2%, then he can withdraw INR 4,08,000 (INR 4 lakhs + 2% of INR 4 lakhs).

However, a key criticism of this rule is that it assumes withdrawal to be based on inflation rather than return earned, creating a possible scenario where the corpus might deplete faster than it grows. Therefore, the investors must take these investment strategies in India as a guiding principle, rather than stringent rules, and tweak the numbers to suit individual requirements.

Also Read: Know About The 8-4-3 Rule Of SIP

Modern Investment Rules For Today’s Investors

Optimal investing requires a planned approach or systematic discipline for efficient diversification and portfolio allocation. Discussed here are various norms that experienced investors often follow.

- Long-term approach: Volatility is an intrinsic characteristic of the market. Such fluctuations often ease over time. Therefore, experienced investors often take a cautious approach before reacting hastily. Maintaining long-term goals and avoiding the temptation to react to sudden market turns might be detrimental. Furthermore, investors who try to time the market or make short-term gains often indulge in high-risk investments.

- Avoid reacting to trends: Often, certain investments become a trend that everyone talks about, like cryptocurrency. However, not every asset class suits every investor. Therefore, rather than investing based on hype, an investor should ideally analyse their individual risk profile and goals to choose assets that suit them.

- Research and Analysis: Before undertaking any investment, the investor should ideally undertake a holistic analysis of the asset class or category and the particular asset in question. Investors should look into risk, returns, and other nuances, along with understanding if the asset suits their own circumstances and goals.

- Periodic Review: An investor should periodically review their portfolio, say quarterly or annually, to gauge if the assets are performing according to expectations. If any asset consistently underperforms, the investor can liquidate and redirect funds into another medium. Moreover, the investor can control the overall risk level of the portfolio and ensure that it is in line with the goals.

However, despite the several norms and thumb rules, investments can still perform unexpectedly. In such a scenario, it is important to analyse the situation and make necessary decisions.

When Investment Thumb Rules Fail

Every investor is unique with their distinct goals and risk tolerance. However, investment rules and norms are generic principles to guide overall investment philosophy. Therefore, such rules might falter if not applied with certain guardrails.

- Ignoring personal goals: The norms and rules might serve as guiding principles. However, the primary objective is to fulfil the personal goals that the investor sets. Therefore, investors might tweak the rules to suit their needs and goals.

- Overlooks risk tolerance: While risk tolerance principles give an umbrella norm, the actual risk tolerance of an investor might not adhere to the uniform rules. For instance, it is usually believed that risk tolerance reduces with age, but compare the risk tolerance of a 25-year-old with several dependents and a 50-year-old millionaire. Contrary to the norm, in this case, the 50-year-old might have a higher risk tolerance.

- Prolonged Volatility: If marketplace uncertainty persists for a long time, say during wars or complete political instability, investors might bear a detrimental impact on their portfolio despite following norms.

In an ideal scenario, investors should take the investment thumb rules as guiding principles to make decisions based on their individual investment needs and goals.

Conclusion

These 10 investment thumb rules are not just popular sayings, they are time-tested strategies that help Indian investors build discipline, reduce financial stress, and grow wealth steadily over time. From budgeting with the 50:30:20 rule to calculating your retirement needs and diversifying your portfolio, each rule offers a practical framework to strengthen your financial future.

While these thumb rules are a great starting point, remember that your personal goals, income level, and risk appetite should always guide your final investment plan. Combine these with timely financial advice and modern investing tools for better outcomes.

Explore fixed-income options like Bonds, SDIs, and now Mutual Funds, all on one platform—only on Grip Invest.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001