Expenses Disallowed Under Section 43B Of The Income Tax Act: Rules, Examples And Compliance Guide

Introduction: Why Section 43B Is Important For Tax Compliance

Businesses and enterprises are the backbone of an economy. They boost economic growth, facilitate the circulation of money, and even create job opportunities. However, people always assume that these benefits come only from the top multinational, multidimensional businesses.

Historically speaking, medium and small businesses have contributed significantly to the economy. As of November 20, 2025, a total of 7.16 crore MSMEs have been registered on the Udyam Registration Portal and the Udyam Assist Platform (UAP), collectively employing around 31.33 crore people.

Given their scope and economic impact, the government has taken several steps to make them more mainstream, ensuring ease of doing business and better tax procedures. One of such initiatives includes a list of allowed expenses and expenses disallowed under Section 43B of Income Tax Act.

What Is Section 43B Of The Income Tax Act?

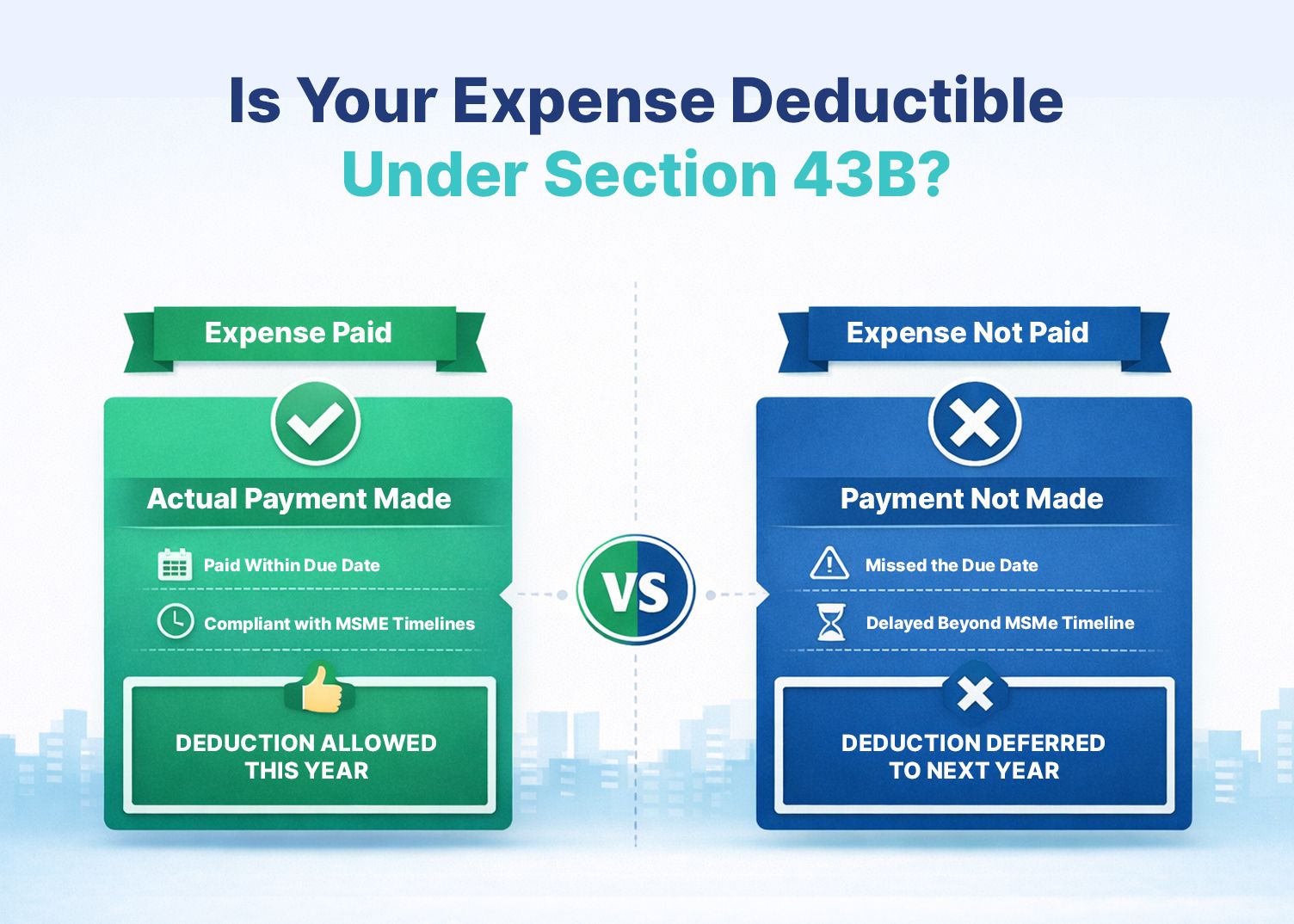

Section 43B of the Income Tax Act states that certain deductions are allowed only on actual payments. Unlike normal accounting methods (where expenses are deducted when they accrue or arise, whichever is earlier), Section 43B requires actual payment of specific expenses before a deduction is allowed for tax purposes. This means that expenses such as taxes, bonuses, and interest can only be deducted in the year they are paid, not in the year they are booked in the accounts.

- Payment basis deduction rule

The section requires that expenses are allowed as tax deductions only when they are actually paid, not merely recorded in the books of accounts. Earlier, businesses could claim deductions on an accrual basis (when the expense was incurred), even if the payment had not actually been made. This ensures that the government receives dues without unnecessary delay.

- Purpose of the provision

The purpose of section 43B is to ensure that the outflow of the reporting business matches its tax returns. It prevents taxpayers from misusing deductions by stopping them from claiming unpaid expenses. The section has also been a great move for MSMEs (Micro, Small, and Medium Enterprises), especially after the introduction of clause (h), which ensures timely payments to these enterprises.

Expenses Covered Under Section 43B

There are a wide range of expenses that are allowed under Section 43B of the Income Tax Act. These mostly include a business's statutory dues and employee benefit-related payments. Here is the Section 43B expenses list:

- Tax, Duty, Cess or Fee Paid Under Any Law: Any tax, duty, cess, or statutory fee payable under existing laws is allowed as a deduction only when actually paid. This includes GST, customs duty, excise duty, and similar government levies.

- Interest on Statutory Taxes and Duties: Interest payable on delayed payment of taxes, duties, or cesses is deductible only upon actual payment. Mere accrual or provision in books does not make the interest amount deductible.

- Employer’s Contribution to Recognized Employee Benefit Funds: Employer contributions to recognized funds such as Provident Fund, superannuation fund, gratuity fund, or NPS are deductible only when paid within prescribed due dates, including the income tax return filing deadline.

- Bonus or Commission Paid to Employees: Bonus or commission payable to employees is allowed as a deduction only when actually paid. It must relate to employment compensation and cannot include dividends paid to employees as shareholders.

- Interest on Loans from Public Financial Institutions or State Financial Corporations: Interest on borrowings from public financial institutions or state financial corporations is deductible only on actual payment, provided it complies with the specific terms and conditions of the loan agreement.

- Interest on Loans and Advances from Scheduled Banks: Interest on loans or advances taken from scheduled banks is allowed as a deduction only when actually paid, in accordance with the loan terms, regardless of the accounting method followed.

- Leave Encashment Provided to Employees: Leave encashment liability is deductible strictly on actual payment to employees. Provisions made in accounts for future leave encashment do not qualify for deduction until paid.

- Payments to Indian Railways: Any sum payable to Indian Railways is allowed as a deduction only in the year of actual payment. Accrued amounts recorded in books cannot be claimed without payment.

- Payments to Micro and Small Enterprises: Payments due to micro and small enterprises must be made within the timelines specified under the MSMED Act. Delayed payments are deductible only in the year of actual settlement.

Common Compliance Mistakes Businesses Make

The government has been endeavouring to make income tax filing easier. However, despite their regular efforts, it is normal for taxpayers to feel confused and make mistakes. This is especially true for businesses, as they handle a large number of transactions, regardless of size. This is also true when the reporting is done under Section 43B. Some of the most common compliance mistakes that businesses make under Section 43B are:

- Late payments impact

Section 43B states that deductions are allowed only if the payment is made on time. If you don't pay your taxes, employer contributions, bank interest, or MSME amounts on time, you won't be able to claim them for that financial year. This raises taxable income and the total amount of taxes owed until the payment is finally made.

- Documentation issues

To make a Section 43B claim, you need to show proof of payment, such as challans, bank statements, and supplier classification details for MSMEs. If you don't have enough documentation or report due dates wrong, you could be disallowed during the assessment. Bad record-keeping greatly increases the risks of not following the rules and possible tax disputes.

How to Ensure Timely Deduction Claims

To avoid disallowed expenses income tax India issues under Section 43B, businesses must align their accounting systems with statutory payment schedules. They should also strictly follow the statutory rules for payment deductions. Since these are expenses allowed on a payment basis, companies should maintain due-date trackers for GST, PF, interest, and MSME payments, set automated reminders, verify vendor classification, and reconcile liabilities with bank challans before filing returns to prevent deduction deferrals and unexpected tax adjustments.

Conclusion

Section 43B, especially after the introduction of clause (h), has a great impact on how businesses claim their expenses. Unlike the usual accrual-based accounting, under this section, only expenses that have already been paid are allowed. What this means is that if it is not actually paid during the financial year, then the expenses disallowed under section 43B of Income Tax Act.

FAQs

1. What expenses fall under Section 43B?

Section 43B covers statutory dues such as taxes, duties, cess, employer contributions to employee benefit funds, bonus or commission, specified loan interest, leave encashment, payments to Indian Railways, and payments to micro and small enterprises.

2. When can deductions be claimed under Section 43B?

Deductions can be claimed only when the specified expenses are actually paid within the prescribed timelines. Even if recorded in the books, the amount becomes allowable only upon payment.

3. Are unpaid statutory dues deductible?

No, unpaid statutory dues are not deductible in the year they are accrued. The deduction is allowed only in the financial year in which the actual payment is made.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001