Section 16 Deductions FY 2026-27: Standard INR 75K + Pro Tax Guide

Section 16 of the Income Tax Act provides specific deductions for salaried employees and pensioners under the 'Income from Salaries' head. These deductions play a crucial role in reducing taxable income and overall tax burden for working professionals. Understanding these provisions can help you optimize your tax planning strategy effectively.

This comprehensive guide explores the various deductions available under Section 16, their eligibility requirements, and practical tips to maximize your tax savings through proper utilization of these benefits.

What Is Section 16 Of Income Tax Act?

Section 16 of Income Tax Act covers three main deductions that can be claimed from gross salary income to arrive at net taxable income:

- Standard Deduction under Section 16 (i)/(a)

- Entertainment Allowance under Section 16(ii)

- Professional Tax under Section 16(iii)

These deductions prescribed under Section 16 provide tax relief to salaried taxpayers by lowering their net taxable salary.

Also Read: How To Save Tax For Salary Above INR 20 Lakhs

Section 16 Deductions Explained: 3 Key Benefits FY26-27

Specific deductions can be claimed by salaried individuals and pensioners directly from the gross salary to arrive at the taxable income, imposed under Income Tax Section 16. As implied before Chapter VI-A deduction like Section 80C, these deductions are one of the most effective tools for salaried tax savings in FY 2026-27.

There are three main benefits of Section 16. These help reduce the overall tax burden, eliminating complex documentation or investment-linked conditions. The table below discusses the deduction. Individuals who can claim it and its importance.

Deduction | Individuals who can claim | Importance |

Standard Deduction 2026 | Claimed by all salaried employees and pensioners | It is a flat reduction in taxable salary with no proof required. |

Entertainment Allowance Tax | Claimed only by state government and central government employees. However, it is not applicable to the private sector employees

| Offers partial tax relief on allowance. |

Professional Tax Deduction | Claimed by salaried employees | Deduction of tax is paid from the salaried income. |

Deductions Under Section 16 Of The Income Tax Act- Explained

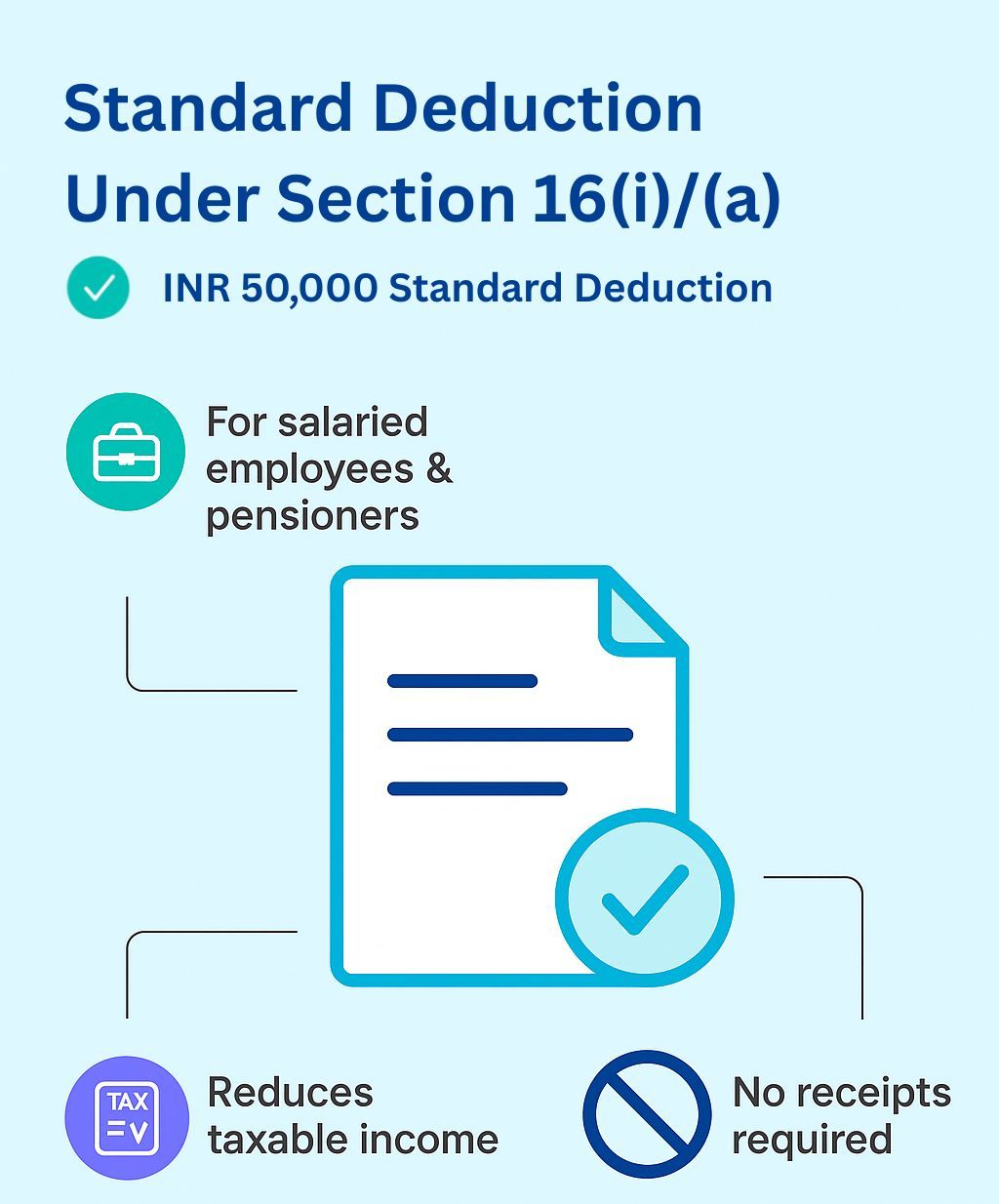

1. Standard Deduction Under Section 16(i)/(a)

Standard deduction under section 16(ia) provides a simple income tax deduction benefit for salaried employees and pensioners with income from salary source. Under this provision, you can claim a standard deduction from your salary income or a pension income in the same manner irrespective of the level of salary income.

Key points to remember:

- Current deduction limit: INR 50,000 (increased from INR 40,000 in Budget 2019)

- Available to all salaried employees (private and government) and pensioners

- Deduction is the lower of INR 50,000 or your actual salary/pension amount

- Operates independently from Section 80C deductions

- Initially excluded from the new tax regime but reintroduced from FY 2023-24

Also Read: Income Tax Exemption Limit Explained

Let us understand the calculation of standard deduction with an example:

The calculation is simple and automatic when reporting salary income on your T1 form. For example, if you have a salary income level of INR 10,00,000. The standard deduction of INR 50,000, or the lesser of INR 50,000 or gross salary level, will be applied to your salary income automatically.

This will result in you reporting your salary income as INR 9,50,000. You may notice the lower taxable income resulted from the application of this standard deduction effectively assisted in reducing your taxable income and, in turn your overall tax liability, all without the need for receipts evidencing expenses.

2.Entertainment Allowance: Govt Employees Only (Limits Table)

Exclusion available to Central and State Government employees, the entertainment allowance tax deduction under Income Tax Section 16 under the old regime, is typically provided to meet official and hospitality expenses. The entertainment allowance is fully taxable for employees in the private sector or public sector undertakings (PSUs).

The benefits of the entertainment allowance tax are subject to specific limits and conditions, unlike the standard deduction. This makes it essential for eligible government employees to understand how much can be claimed to enhance salaried tax savings.

Entertainment Allowance: Deduction Limits

The lowest of the following three amounts is the deduction allowed under section 16(ii)

| Deduction Criteria | Amount |

| 20% of Basic Salary | As applicable |

| Flat Maximum Limit | Rs. 5000 |

| Actual Entertainment Allowance Received | According to the salary structure. |

The lowest value qualifies as a deduction.

Example

Let's take an example of how the entertainment allowance tax is calculated. The following are assumptions to understand the calculations.

| Prticulars | Amount |

| Basic Salary | 50000 |

| Entertainment Allowance Received | 4000 |

| 20% Basic Salary | 10000 |

| Deduction Allowed | 4000 |

Since the lowest of the three limits is 4000, it is also the deductible amount. Due to this, the taxable salary is reduced, and this also contributes to better salary tax savings in the case of eligible government employees.

3. Professional Tax Deduction: State-wise Rates 2026

A state-level levy imposed on salaried employees is a professional tax. This tax amount varied depending on the state of employment. Under Income Tax 16, the Professional tax deduction is limited to the actual amount paid during the FY, subject to a maximum cap of Rs. 2500 annually.

Understanding the applicable slabs is important for accurate tax computation since the rates are different across all states. This also maximises the slalried tax savings under the old tax regime.

The table below shows the Indicative state-wise professional tax rates for FY 2026-27

State | Maximum Professional Tax Annually (Rs.) |

Maharastra | 2500 |

Karnataka | 2400 |

West Bengal | 2500 |

Tamil Nadu | 2500 |

Andhra Pradesh | 2500 |

Telengana | 2500 |

Gujarat | 2400 |

Madhya Pradesh | 2500 |

Kerala | 2500 |

Delhi | None |

Also Read: Gilt Fund Taxation

New Vs Old Regime: What Is Allowed?

Your choice between the old and new regimes has a significant impact on deductions under Section 16 of the Income Tax Act. The new tax regime restricts several deductions that directly affect salaried tax savings while also offering lower slab rates.

The table below shows the Section 16 deduction for both old and new regimes.

Type | Old Tax Regime | New Tax Regime |

Standard Deduction 2026 | Rs. 50000 allowed | Rs. 75000 allowed |

Entertainment Allowance Tax | Allowed for government employees only | Not allowed |

Professional Tax Deduction | Allowed till the actual amount is paid | Not allowed |

The standard deduction 2026 remains the only Section 16 benefit available when comparing both regimes. Deductions linked to the entertainment allowance tax and professional tax deduction are available under the old tax regime.

Conclusion

Section 16 of the Income Tax Act contains important provisions regarding deductions allowed from gross salary income to arrive at net taxable salary. Salaried individuals and pensioners should accurately claim these deductions under Section 16 while filing their ITR to lower their tax liability. Proper compliance and maximum utilisation of these deductions can help taxpayers save significant yearly taxes.

Explore Grip Invest and stay updated on all relevant financial planning opportunities.

Frequently Asked Questions on Section 16 Of Income Tax Act

1. Who can claim standard deduction under Section 16(i)/a)?

The standard deduction under Section 16(i)/(a) can be claimed by all salaried employees and pensioners from the private and government sectors.

2. How can salaried individuals reduce tax liability?

Salaried taxpayers should claim all eligible deductions under Section 16, 80C, 80D, 80E, etc., to lower their taxable income and tax liability.

3. When should ITR be filed to claim Section 16 deductions?

To claim Section 16 deductions, taxpayers should file their ITR within the due date, i.e. 31st July. Delayed filing will lead to the disallowance of these deductions.

4. Do I need to submit proof of expenses to claim the standard deduction under Section 16 (i)/(a)?

No, you do not need to submit any bills to claim a standard deduction. You will receive the deduction by default.

5. I switched employers during the previous fiscal year. Am I eligible for a standard deduction on the earnings I received from each employer separately?

The standard deduction, a fixed amount deducted from an employee's annual salary, remains applicable regardless of the number of jobs held. Only one standard deduction of Rs. 50,000 is permitted for the total income received from all employers collectively.

6. Can I also claim a transport and medical allowance along with a standard deduction?

No, you can only claim the standard deduction of INR 50,000, not the transport and medical allowance from FY 2018-19. For FY 2026-27, the only benefit available under this category is the standard deduction of Rs. 75000

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001