FD Vs ELSS: Which Tax-Saving Option Works Better For Investors In 2026?

Raghav and his daughter Anika were going through a small list of investments they had been postponing for months. For Raghav, saving had always meant protection. A tax-saving FD felt familiar, fixed tenure, assured returns, and no anxiety about markets. He pointed out that when responsibilities are many, certainty matters more than ambition.

Anika listened, but countered with her own logic. She explained that investing in ELSS instead of tax-saving FDs was not about quick gains. It is about letting your money grow with time. At her age, she could afford volatility, and the shorter lock-in gave her flexibility. To her, avoiding the market felt like avoiding opportunity altogether.

Raghav admitted that his comfort came from experience; Anika’s confidence came from starting early. Neither was wrong; they were just shaped by different phases of life. But the question remained: safety or growth, or FD VS ELSS, which one really fits better?

Introduction To FD Vs ELSS

The Indian market is evolving quickly. It can be attributed to higher participation among the middle class and younger generations. While an influx of young investors has definitely increased the overall risk appetite of the market, the demand for stable tax saving options is still very much alive. However, this has created a new dilemma between safety and growth, or more precisely, between ELSS vs fixed deposit. So if you are also wondering what the best tax saving investments India are, read on and find out.

Also Read: Best Corporate FDs Of 2026

What Is An FD For Tax Saving?

A Fixed Deposit (FD) for tax savings is exactly what it sounds like. It is a fixed deposit that helps people grow their funds without tax liability. Under it, individuals and HUFs can claim a tax deduction of up to INR 1,50,000 in a financial year (old tax regime). As they are fixed, they come with a lock-in period, usually 5 years, during which you cannot withdraw them. However, as they are a solid asset, you can get a loan against them.

What Is ELSS?

An equity-linked savings scheme (ELSS) is an equity-linked mutual fund. Under it, investors enjoy an 80% exposure to equity. It is the only mutual fund scheme that is eligible for tax deduction under Section 80C. Here, investors are eligible for a tax deduction of up to Rs 1,50,000 annually. However, ELSS tax benefits 80C are not the only reason for its popularity. It is highly popular among investors seeking both growth and stability, and who will not shy away from a little risk.

FD Vs ELSS: Key Differences That Matter

Choosing between FD and ELSS goes beyond returns alone. It involves understanding how risk, lock-in periods, taxation, liquidity, and growth potential align with your life stage, income stability, and long-term financial priorities in a changing investment landscape.

Particulars | Equity-linked savings scheme (ELSS) | Fixed Deposit (FD) for tax saving |

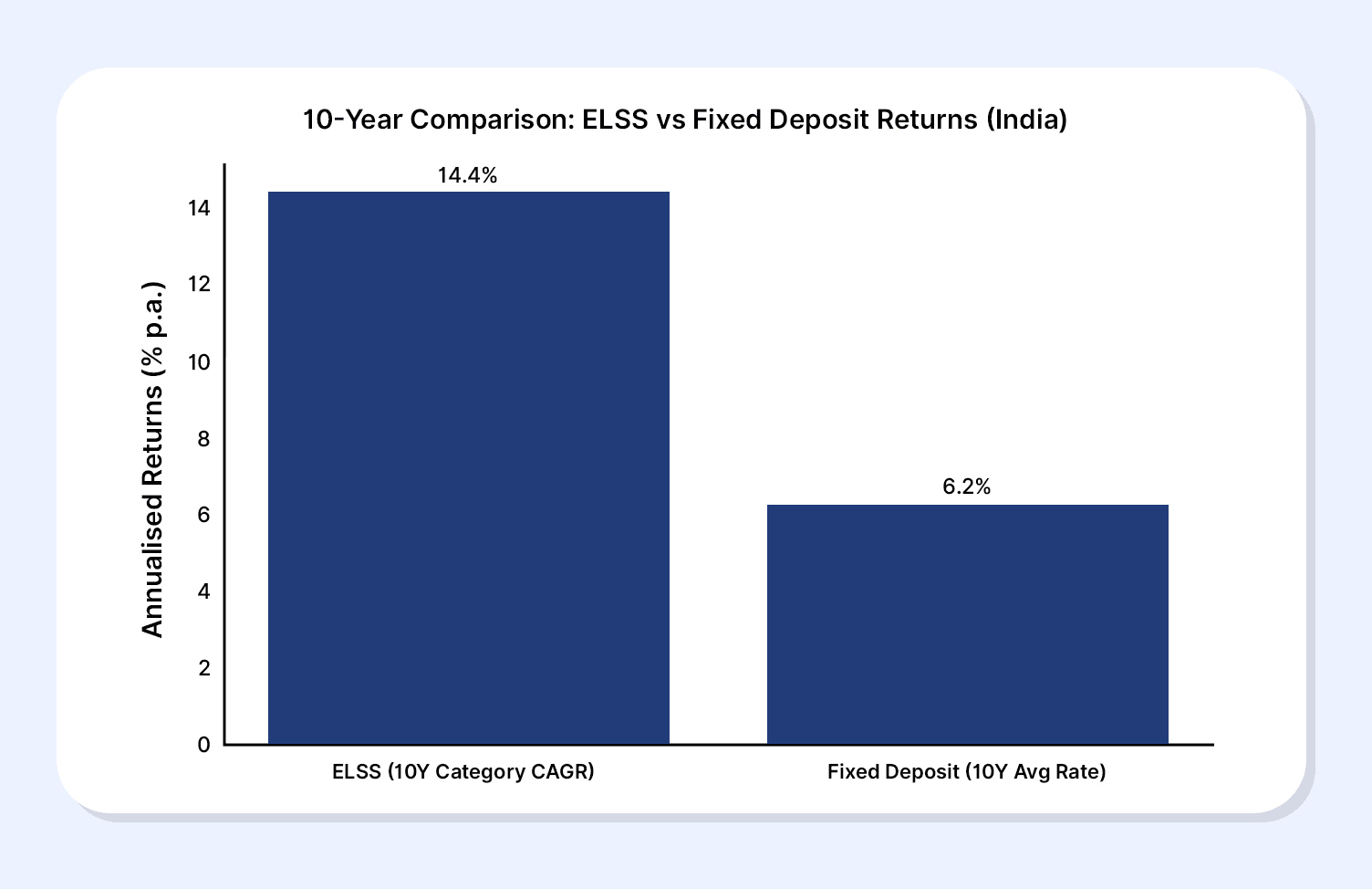

Returns | Returns on ELSS are not fixed as they are subject to equity market risks. However, historical data show that many leading ELSS has delivered a 14%-16% CAGR over the last 5 years. | The bank decides the return rate on tax-saving FD. Usually, the interest rate ranges from 6% to 7.5%. |

Tenure | ElSS has a 3-year lock-in period. After completing the lock-in period, you can redeem or reinvest your funds. | Tax-Saving FDs have a 5-year lock-in period. You can extend it up to 10 years. After completing the lock-in period, you can redeem or reinvest your funds. |

Risks | As ELSS has equity exposure, it carries substantial risk. However, the high growth potential compensates for the risk. | Tax-saving fixed deposits are a much safer option than market exposure, as they offer more. |

Online option | It is easy to start an ELSS online. You can choose between a lump sum and an SIP option. | Most banks now allow opening tax-saving FDs online via net banking or mobile apps, though some still require a branch visit |

Figure 1.0: 10 Year CAGR Comparison of ELSS and FD in India

Which One Should Investors Choose?

Raghav and Anika are not the only ones having this disagreement. In fact, with the younger millennials and Gen Z dominating the economy, ELSS vs tax saving FD has become one of the biggest questions. However, there is no correct answer to it. The right choice between ELSS mutual funds vs tax saver FD depends on your goals and risk appetite.

1. For Conservative Investors

If you are more conservative in your investment approach or in a situation that does not allow risk-taking, you should opt for a tax-saving fixed deposit. They will enable you to hedge against market volatility and provide predictable returns.

2. For Long-Term Wealth Creation

On the flip side, if you have a higher tolerance for risk or are looking for higher returns over a long period of time, equity-linked savings schemes are a good choice for you. For instance, ELSS for salaried employees, is growing as young employees have the bandwidth to take long-term risks.

How To Combine ELSS + Fixed Income For Stable Growth

While the FD vs ELSS returns comparison is a great way of deciding between the two options, you do not necessarily have to pick one and let go of the other. In fact, you can create a balanced investment basket for yourself by combining both. While the ELSS will offer exponential growth, the tax-saving fixed deposit will neutralise market risk. If you are not sure where to start, you can use modern platforms like Grip Invest, which offer advanced features to help you navigate to your best options.

Frequently Asked Questions

1. Is ELSS better than FD for tax saving?

Both ELSS and FD for tax saving have their benefits and downsides. The key is to invest, keeping your financial goals and risk profile in mind.

2. Which has a lower risk: FD or ELSS?

When talking about risk, a fixed deposit for tax savings has lower risk, as it is not exposed to the capital market, unlike ELSS.

3. What is the lock-in for ELSS?

ELSS has a lock-in period of three years, which is the shortest among all Section 80C tax-saving options, after which the investment can be redeemed.

Reference:

1. Bajaj finance, accessed from: https://www.bajajfinservmarkets.in/fixed-deposit/what-is-the-history-of-fixed-deposits-through-time

2. Groww, accessed from: https://groww.in/mutual-funds/category/best-elss-mutual-funds

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001