Best Corporate FD In India: Higher Returns With Calculated Risk

Ashok noticed Sunita filling out some paperwork one evening and casually asked what she was working on. She told him that she was applying for a fixed deposit. Ashok laughed lightly and said, “You should have told me. I could have helped you with this.” He went on to mention a recent conversation with a friend who had just retired from a bank, adding that such contacts usually know where to get the best rates.

Sunita smiled and asked, “Did your banker friend also tell you that there are fixed deposits beyond bank FDs?” Ashok paused, surprised, and asked what she meant. Sunita calmly explained that after working for over three decades in the corporate sector, she had picked up a few things herself. She pointed out that corporate FDs can offer better flexibility and potentially higher returns, making them a useful way to diversify their savings.

Introduction — Why Investors Look Beyond Bank FDs

Fixed deposits have been a staple of people's financial portfolios for a long time. However, with the recent repo rate cuts by the

Reserve Bank of India (RBI), several banks and small finance banks had to slash their FD interest rates. This had a direct impact on people’s savings, nudging them to seek fixed deposit alternatives that could earn them higher returns. The goal is simple: look for a higher fixed income yield, which many, like Sunita, found in corporate fixed deposits India.

What Is A Corporate FD?

As the name suggests, a corporate fixed deposit is a fixed deposit offered by a corporation. They are usually provided by Housing Finance Companies (HFCs)/Non-Banking Financial Companies (NBFCs). As corporations provide them, they are not affected by the RBI’s repo rate, and therefore, corporate FD interest rates stay competitive even when traditional FDs’ return rates get flat.

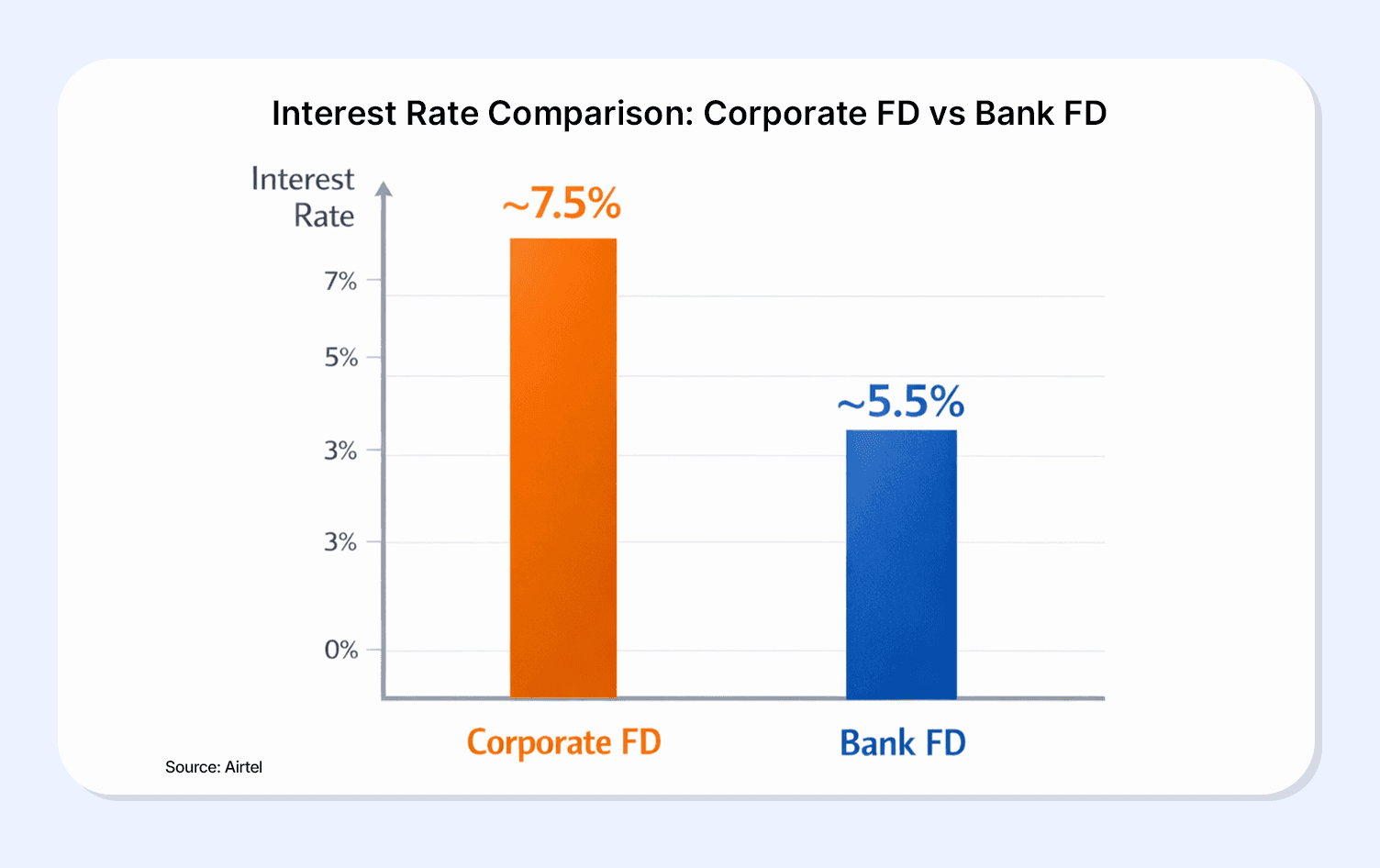

Corporate FD Vs Bank FDs

Corporate fixed deposits India have emerged as one of the most reliable fixed deposit alternatives due to several reasons, like higher interest rates and ease of access. Here are a few things that set them apart from traditional bank FDs.

Particulars | Bank FDs | |

Interest Rate | Corporate fixed deposits India usually offer a higher interest rate (1-3%). | The interest rates of Bank FDs are usually low compared to Corporate fixed deposits India. |

Liquidity | While they do enjoy some liquidity, they usually carry a penalty on premature withdrawal. | Bank FDs have more flexibility when it comes to premature withdrawals. |

Taxation | Interest earned on Corporate fixed deposits India is taxable, irrespective of whether they are reinvested or withdrawn. | Similarly to Corporate fixed deposits India, bank FDs are also taxable in India. |

How to Choose The Best Corporate FD

Choosing the best corporate FD goes beyond comparing interest rates. It requires evaluating risk, issuer reliability, and investment suitability to ensure returns are not only higher but also aligned with long-term financial stability.

1. Issuer Quality

The first and foremost thing to check while looking for the best corporate FD is the issuer. If the issuing company is not financially strong or reliable, even if the corporate FD interest rates appear attractive, the investment cannot be considered safe. One effective way to do this is to check the credit ratings assigned by recognised rating agencies such as CRISIL, CARE, and ICRA before investing. These ratings indicate the issuer’s creditworthiness and ability to meet repayment obligations.

2. Diversification Across Issuers

Diversification is the cardinal rule of financial investment across the board and applies to corporate FDs as well. No matter how attractive the terms of FD are, it is never advisable to invest all the savings in a single scheme. Rather, diversify your portfolio across issuers.

3. Risk Analysis

The RBI does not regulate corporate FDs; therefore, they are not covered under the insurance cover offered by the RBI subsidiary, the Deposit Insurance and Credit Guarantee Corporation (DICGC). It is thus crucial that investors carefully assess the financial stability of the issuing company.

While looking for the best corporate FD, it is crucial to understand that the definition of 'best' will vary depending on personal factors. Therefore, while considering various financial factors, also take into account whether the FD's tenure aligns with your financial needs. An option with high corporate FD interest rates might not be best for you, if its tenure does not align with your finances.

Also Read: FD Auto Renewal: What Are The Risks & Benefits and How To Do It?

Best Corporate FD In India

The best corporate FD in India can differ from one investor to another, as suitability depends on individual risk tolerance, return expectations, and investment goals rather than interest rates alone. However, here are a few examples of well-rated corporate FDs known for competitive returns and reliability:

Corporate FD | Why It Is Good |

Shriram Finance | AA+ ratings from ICRA and IND AA+/Stable by India Ratings and Research back the Shriram Finance Corporate FD. Further, it offers competitive returns, with interest rates up to 8.15% pa, and an additional 0.50% benefit for senior citizens and 0.05% for women2. |

Bajaj Finserv | Bajaj Finance Corporate FDs carry top credit ratings such as CRISIL AAA/Stable and ICRA AAA/Stable, indicating high safety for investors. The Interest rates for customers below 60 years are up to 6.95% pa, while they are up to 7.30% pa for senior citizens3. |

Suryoday | It's a small finance bank |

Manipal Housing Finance Syndicate | Manipal Housing Finance Syndicate’s Corporate FD has been rated “ACUITE A” by Acuite Ratings & Research Limited. The interest offered by the entity can go up to 8.25% pa with an additional 0.25% for senior citizens4. |

PNB Housing Finance Ltd. | It comes with CARE ‘AA+/Stable’ & CRISIL ‘AA+/Stable’ ratings, indicating a high level of safety. The highest interest rate for the PNB Housing Finance Ltd. Corporate FD can go up to 7.92% pa. There is an additional 0.25% for seniors, but only on deposits up to INR 1 crore5. |

Sundaram Home Finance | Sundaram Home Finance has been rated [ICRA] AAA (Stable) by ICRA & CRISIL AAA/Stable by CRISIL. The interest rate for the FD can go up to 7.15% pa for the general public and up to 7.50% pa for senior citizens6. |

ICICI Home Finance | It showcases the highest degree of safety with ratings like AAA/Stable by CRISIL, AAA/Stable by ICRA, and AAA/Stable by CARE, offering rates up to 7.10% and a senior citizen bonus of 0.35%7. |

LIC Housing Finance | Backed by a CRISIL AAA rating, LIC Housing Finance emphasizes safety and consistency, with rates reaching 6.80% and an additional 0.25% for senior citizens8. |

Conclusion

Corporate FDs can make sense if you are willing to take measured credit risk in exchange for higher returns than bank FDs. They work best when you focus on well-rated issuers, diversify across companies, and match the tenure to your financial goals.

What this really means is that chasing the highest corporate FD interest rate without looking at risk can backfire, while a balanced approach can genuinely improve your fixed-income returns.

That said, corporate fixed deposits are not the only fixed deposit alternatives available today.

For investors who want better transparency, stronger risk assessment, and diversified exposure, platforms like Grip Invest offer access to regulated fixed-income instruments such as corporate bonds and structured debt opportunities.

These can help you move beyond traditional FDs while staying aligned with long-term financial discipline and capital protection.

FAQs

1. Are corporate FDs safe in India?

The RBI does not regulate corporate FDs, and therefore, they are not insured by DICGC, which increases the risk. However, this does not make them completely unreliable. Several factors, such as a high credit rating from a reputable agency, indicate reliability.

2. What is better corporate FD or bond?

Both corporate FD and bond have their pros and cons. The better option will be determined by factors such as your financial goal, the return rate, whether the tenure aligns with your financial timeline, etc.

3. Are corporate FDs taxable?

Yes, just like other fixed-income instruments, corporate FDs are taxable. It wil be taxed as per your income tax slab.

References:

1. Airtel, accessed from: https://www.airtel.in/blog/fixed-deposit/company-fixed-deposit-vs-bank-fixed-deposit-which-is-better/

2. Shriram, accessed from: https://tinyurl.com/fzd4f3ca

3. Bajaj finserv, accessed from:

https://www.bajajfinserv.in/investments/fixed-deposit-interest-rates

4. Manipal housing, accessed from: https://manipalhousing.com/uploads/deposit-application.pdf

5. PnB housing, accessed from: https://www.pnbhousing.com/fixed-deposit/interests-rates#fixedtable_scroll_box

6. Sundaram home, accessed from: https://www.sundaramhome.in/deposits

7. ICICI, accessed from: https://www.icicihfc.com/fixed-deposit

8. LIC housing, accessed from: ??https://www.lichousing.com/corporate-deposits

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip, the latest financial knick-knacks and shenanigans that take place in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities are subject to risks. Read all the offer-related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading. This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for the consequences of any actions taken based on the information provided. For more details, please visit https://www.gripinvest.in/.

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001.