RBI Banking Reforms 2026: Key Updates For Investors, Banks And Corporates

Post the introduction of the Asset Quality Review by RBI, the Non-Performing Assets reduced significantly. From a peak of 14.58% in March 2018, the gross NPA ratio of public sector banks decreased to 3.12% in September 2024, and to 2.58% in March 20251.

To further diminish the NPAs, boost capital adequacy and ease lending restrictions, amidst US-led headwinds, the RBI has unveiled a set of new banking sector reforms in India on 1 October 20252.

This blog explores the key RBI banking reforms in India in detail.

RBI Banking Reforms India: Key Reforms Explained

RBI Governor Sanjay Malhotra noted concerns over US Tariffs and announced the following reforms.

1. Risk-Based Deposit Insurance India

Deposits held with commercial banks are insured up to INR 5,00,000 per deposit per bank by the Deposit Insurance and Credit Guarantee Corporation3.

Currently, all banks pay DIGCC a uniform premium of INR 12 paise for every INR 100 of their deposits for this insurance cover. In this recent announcement, the RBI has changed this uniform premium into a risk-based structure.

Stronger banks with better risk management, capital adequacy and asset quality will pay lower premiums, while riskier banks will bear higher premiums. Moreover, the current rate of INR 12 for every INR 100 of deposits will serve as a ceiling.

For example, if Bank A has a better risk profile than Bank B, it will pay a lower premium than Bank B. However, the premium payable by Bank B won’t exceed the current rate of INR 12 paise for every INR 100 deposit.

Now, let us move on to the next RBI banking reforms in India, aiming to promote an optimal risk profile.

2. Basel III Norms and Expected Credit Loss Provisioning in India

RBI announced that all Scheduled Commercial Banks and All India Financial Institutions must follow the Expected Credit Loss approach for provisioning, rather than the incurred-loss approach that is currently followed4.

Provisioning refers to the process of setting aside a part of profit to meet losses from NPAs. Under the current incurred-loss system, banks use current or past losses for provisioning. However, ECL is a forward-looking system that uses weighted estimates for probable losses.

RBI has made ECL provisioning applicable from 1 April 20275. A glide path till March 2031 is also given to reduce any shocks arising from increased provisioning.

Now, another key aspect in this regard is the Basel III norms in India. These norms set minimum ratios, like the 11.50% minimum capital to risk-weighted assets ratio, to ensure the maintenance of high-quality capital by banks to absorb losses6. RBI has also stated that revised Basel III Capital adequacy norms will take effect from 1 April 20277. A draft on the same will be issued shortly8.

To give Indian banks a competitive edge and ease of business, the RBI has also eased lending norms. The next section sheds light on the same.

RBI Lending Reforms 2026

Discussed below are the key lending reforms brought in by the RBI reforms 2026 to ease lending while optimising oversight.

1. Banks can now adjust interest rate spreads sooner. Certain charges levied on borrowers can be cut without abiding by a three-year lock-in9.

2. Working capital loans, which were initially restricted to jewellers, can now be extended to any producer using bullion as a raw material.

3. In a move to ease IPO financing norms in India, the RBI has raised the IPO financing limit to INR 25 Lakhs from INR 10 Lakhs per person10.

4. Individual loans secured by shares are increased from INR 20 lakh to INR 1 crore.

5. Borrowing rules are eased for companies with bank loans above INR 10 crores by removing the prior cap and extra capital requirements.

Next, we must discuss the related-party lending framework, a key aspect of RBI banking reforms in India.

RBI’s New Guidelines On Related Party Lending

According to the related party lending norms, a bank or NBFC requires board approval and adherence to other norms for lending to its own directors, affiliates and other related entities. It also includes promoters, shareholders and key management persons with over 5% equity11.

The table below shows the scale-based nature of the approval requirement.

| Bank Scale | Bank Asset (INR) | Loan amount above which board approval is required (INR) |

| Large | 10 lakh crore | 50 Crore |

| Mid | 1 Lakh crore to 10 lakh crore | 10 Crore |

| Small | Below 1 lakh crore | 5 Crore |

Source: ETEdge12

Now, let us move on to the final key banking reform 2026, the ECB and rupee internationalisation reforms.

Rupee Internationalisation Reforms And ECB Norms India

External Commercial Borrowing refers to credit that particular Indian entities can obtain from non-residents, like foreign banks. RBI has liberalised ECB rules to make borrowing easier. Discussed below are some of them.

- Banks can now raise funds up to USD 1 billion or 300% of their networth, whichever is greater, through the ECB. The current ceiling was USD 750 million13.

- Elimination of cost-caps on the ECB is also noted.

- With a floor of 3 years, the minimum maturity requirement is reduced for most sectors.

The RBI reforms 2026 also move to internationalise the rupee through the following measures14.

- Authorised dealer banks can now extend credit to non-residents from Nepal, Sri Lanka and Bhutan in Indian rupees.

- A reference rate for currencies of major trade partner countries of India will be established by the RBI.

- Investment in commercial papers and corporate bonds can be made by foreign banks through their Special Rupee Vostro Accounts Balance.

The RBI banking reforms India are aiming to bring significant ease for different economic stakeholders. Let us examine these advantages in detail.

RBI Banking Reforms India: Advantages For Investors, Banks And Companies

Discussed below are the key benefits of the RBI reforms 2026 for different stakeholders.

Benefits For Banks

The banks and financial institutions expect the following benefits.

- Through measures like risk-based deposit insurance premiums, the banks can take advantage of their optimal risk management.

- The capital position of companies can also strengthen over time as the reforms aim to boost the ecosystem by simplifying and modernising procedures.

- The banks now have flexibility in the lending sector.

- Various reforms have made compliance requirements similar to global standards, making Indian banks competitive in the global space.

Benefits For Investors

Discussed below are some benefits that investors may expect over time.

- Banking stocks might improve their valuations, giving a market opportunity.

- Bank bonds can get stronger, backed by these reforms, resulting in safer fixed-income generation.

Benefits For Borrowers and Corporations

Discussed below are the benefits for businesses and corporations.

- The increase in IPO financing limit can make credit access easier and more efficient.

- The reforms can reduce the financing cost of infrastructure and other large projects.

However, despite these advantages, there might be some challenges associated with the RBI banking reforms in India.

Risks And Challenges Of The RBI Banking Reforms

Discussed below are the key challenges of the banking reforms.

- The transition from old provisions to new ones can put fiscal pressure on institutions.

- Delay in implementing the norms might diminish their benefits.

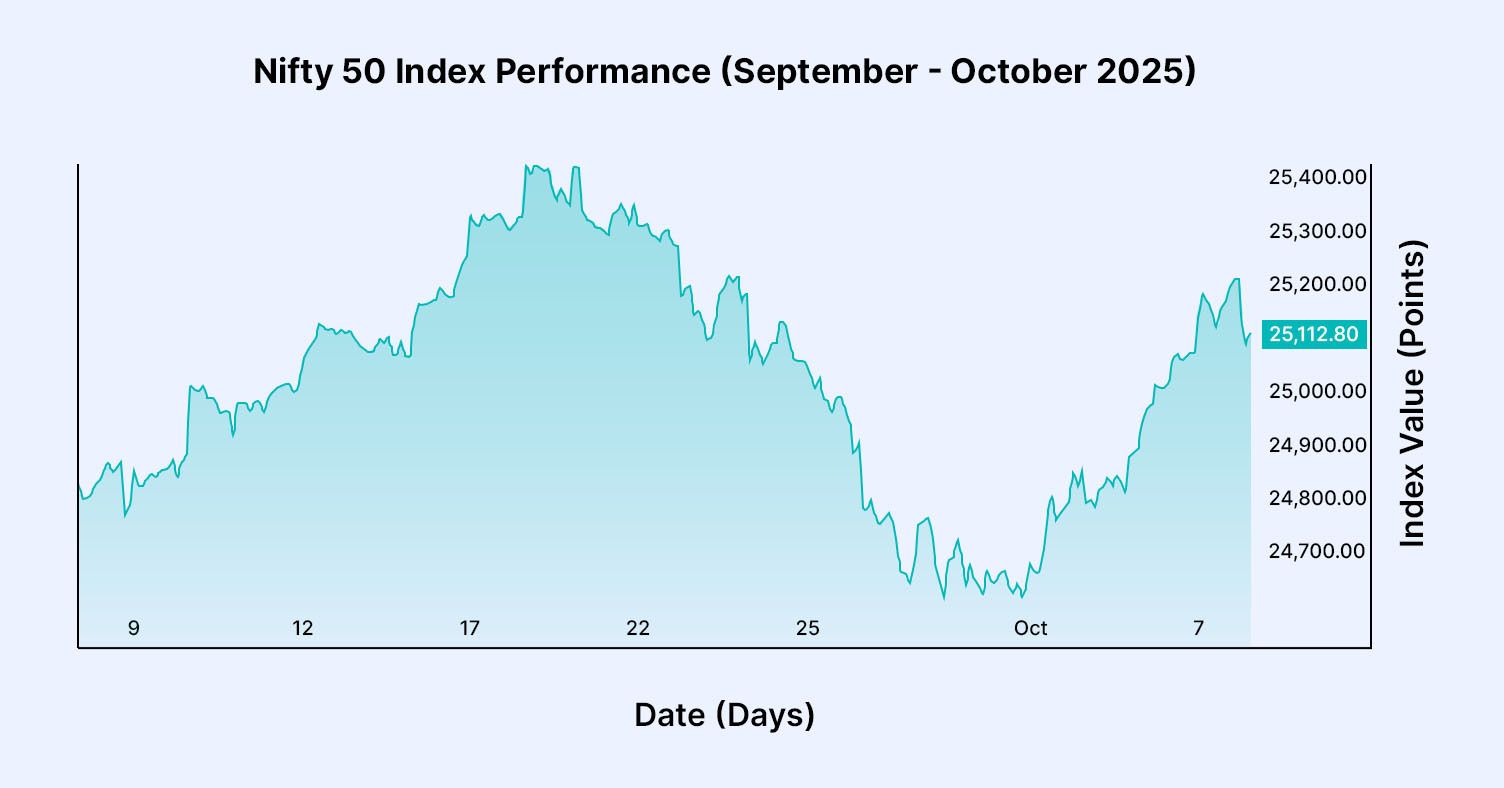

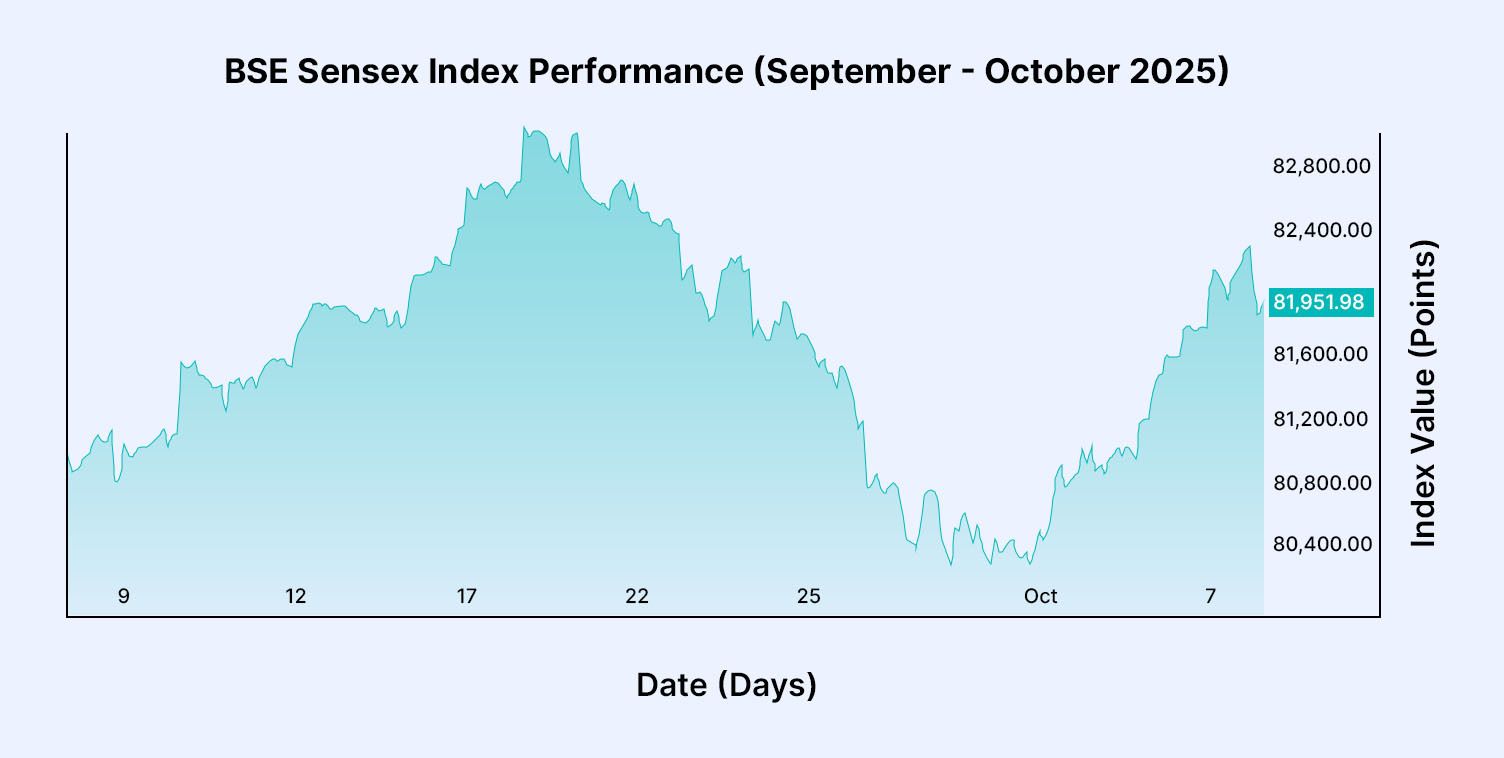

However, despite the challenges, Sensex and Nifty extended early gains post-reform announcement. Sensex jumped about 600 points, backed by banking stock buy-ins15.

While the NSE Nifty rose 170.7 points to 24,781.80, the BSE Sensex rose 599.43 points to 80,867.05.

However, making the best of these trends requires optimising your portfolio.

How To Position Your Portfolio Around These Reforms

Investors can benefit from these reforms through the following instruments.

- Stocks: Inclusion of optimal banking and financial stocks can aid in portfolio optimisation. Stocks of Axis Bank, ICICI Bank and Kotak Mahindra Bank were the top gainers on 1 October 202616.

- Bonds: Several reforms directly or indirectly benefit the bond market. Curated platforms like Grip can offer a range of bonds with up to 9% to 14% yield.

Conclusion

The RBI’s 2026 banking reforms mark a transformative moment for India’s financial sector, driving it toward global standards and greater resilience. These wide-ranging changes are expected to make Indian banks stronger, promote prudent risk management, and boost both credit and investor confidence.

With improvements such as risk-based deposit insurance, forward-looking provisioning, more flexible lending norms, and steps toward rupee internationalisation, the reforms are poised to unlock new opportunities across banking, bonds, and equities. Investors keen on optimising their portfolios should closely watch quality banking stocks and fixed-income opportunities poised to benefit from these regulatory shifts.

As these policies take effect, the potential for sustainable growth, better risk-adjusted returns, and a more globally competitive Indian banking system has never been higher. Login to Grip Invest to explore curated opportunities that align with India’s evolving financial landscape.

FAQs On RBI’s Banking Reforms

1. What changes have been made to the lending norms under RBI reforms?

RBI has eased several lending restrictions, including allowing banks to finance mergers and acquisitions, increasing IPO financing limits from INR 10 lakhs to INR 25 lakhs, and raising loan limits against shares from INR 20 lakhs to INR 1 crore.

2. What is the related-party lending rule introduced by RBI?

Banks and NBFCs now require board approval for loans to related parties such as directors, promoters, and affiliates. The approval threshold varies by bank size to enhance governance and transparency.

3. How do RBI’s reforms support rupee internationalisation?

The reforms allow authorised dealer banks to extend rupee credit to residents in neighboring countries, reduce maturity requirements on External Commercial Borrowings (ECBs), and facilitate foreign bank investments via rupee vostro accounts.

4. How will RBI’s 2026 reforms affect investors?

Improved bank capitalization and risk management may uplift banking stocks and strengthen bank bonds, offering safer and potentially more lucrative investment options.

References:

1. Ministry of Finance Press release, accessed from: https://tinyurl.com/2z6fv29r

2. Times of India, accessed from: https://timesofindia.indiatimes.com/business/india-business/in-major-reforms-rbi-expands-credit-for-companies-limits-on-loansagainst-shares-hiked-5x-to-rs-1cr/articleshow/124267663.cms

3. Money Control, accessed from: https://www.moneycontrol.com/banking/rbi-to-introduce-risk-based-deposit-insurance-premium-flat-rate-to-act-as-ceiling-article-13592520.html

4. Times of India, accessed from: https://timesofindia.indiatimes.com/business/india-business/opinion-rbis-risk-regulation-reset-balancing-growth-with-stability/articleshow/124286768.cms

5. The Business Standard, accessed from: https://www.business-standard.com/finance/news/ecl-framework-proposed-to-be-implemented-from-april-1-2027-rbi-guv-125100100511_1.html

6. Bank Of Maharashtra, accessed from: https://bankofmaharashtra.in/writereaddata/documentlibrary/9ddb730f-d3fd-4690-a802-05a4366fd22b.pdf

7. CNBC TV18, accessed from: https://www.cnbctv18.com/business/finance/rbi-implement-expected-credit-loss-framework-basel-iii-norms-from-april-2027-19699413.htm

8. The Business Standard, accessed from: https://www.business-standard.com/finance/news/ecl-framework-proposed-to-be-implemented-from-april-1-2027-rbi-guv-125100100511_1.html

9. Times of India, accessed from: https://timesofindia.indiatimes.com/business/india-business/rbis-new-norms-brings-flexibility-for-borrowers-and-banks/articleshow/124218000.cms

10. Times of India, accessed from: https://timesofindia.indiatimes.com/business/india-business/in-major-reforms-rbi-expands-credit-for-companies-limits-on-loansagainst-shares-hiked-5x-to-rs-1cr/articleshow/124267663.cms

11. The Economic Times, accessed from: https://economictimes.indiatimes.com/news/economy/policy/rbi-proposes-revised-framework-for-lending-to-related-parties/articleshow/124295168.cms

12. ET Edge, accessed from: https://etedge-insights.com/industry/bfsi/govt-orders-fair-probe-after-export-firm-wintrack-hhalts-india-ops-alleges-bribery-and-harassment-by-chennai-customs/

13. Indian Express, accessed from: https://www.newindianexpress.com/business/2025/Oct/04/sweeping-ecb-reforms-rbi-moots-1-billion-cap-wider-eligibility-easing-fund-usage

14. Times of India, accessed from: https://timesofindia.indiatimes.com/business/india-business/internationalising-of-rupee-rbi-announces-slew-measures-to-promote-indian-currency-heres-all-you-need-to-know/articleshow/124250609.cms

15. The Hindu, accessed from: https://www.thehindu.com/business/markets/stock-markets-extend-morning-gains-post-rbi-policy-sensex-jumps-nearly-600-points/article70115807.ece

16. The Hindu, accessed from: https://www.thehindu.com/business/markets/stock-markets-extend-morning-gains-post-rbi-policy-sensex-jumps-nearly-600-points/article70115807.ece

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001