Premature FD Withdrawal: Penalty Rules And Smart Alternatives

Introduction

Fixed deposits (FDs) are among the most trusted investment options for many Indians — offering guaranteed returns, safety, and peace of mind. Yet, even the most careful investors often find themselves prematurely breaking their FDs. Why does this happen so often. The answer usually lies in one word — liquidity. When unexpected expenses arise — a medical emergency, sudden travel, or an irresistible investment opportunity — cash on hand becomes more valuable than fixed returns.

Unfortunately, inadequate emergency planning forces investors to dip into their long-term savings, sometimes losing interest income and incurring penalties1. In today’s unpredictable financial climate, understanding why and when investors break FDs is not just about managing money — it is about building flexibility into your financial plan. Let us explore how better liquidity management can help you avoid breaking your FDs early and keep your savings strategy on track. As a starting point, it helps to clearly understand what actually qualifies as a “premature” FD closure in the first place, and why that definition matters for your returns.

What Counts As Premature FD Closure

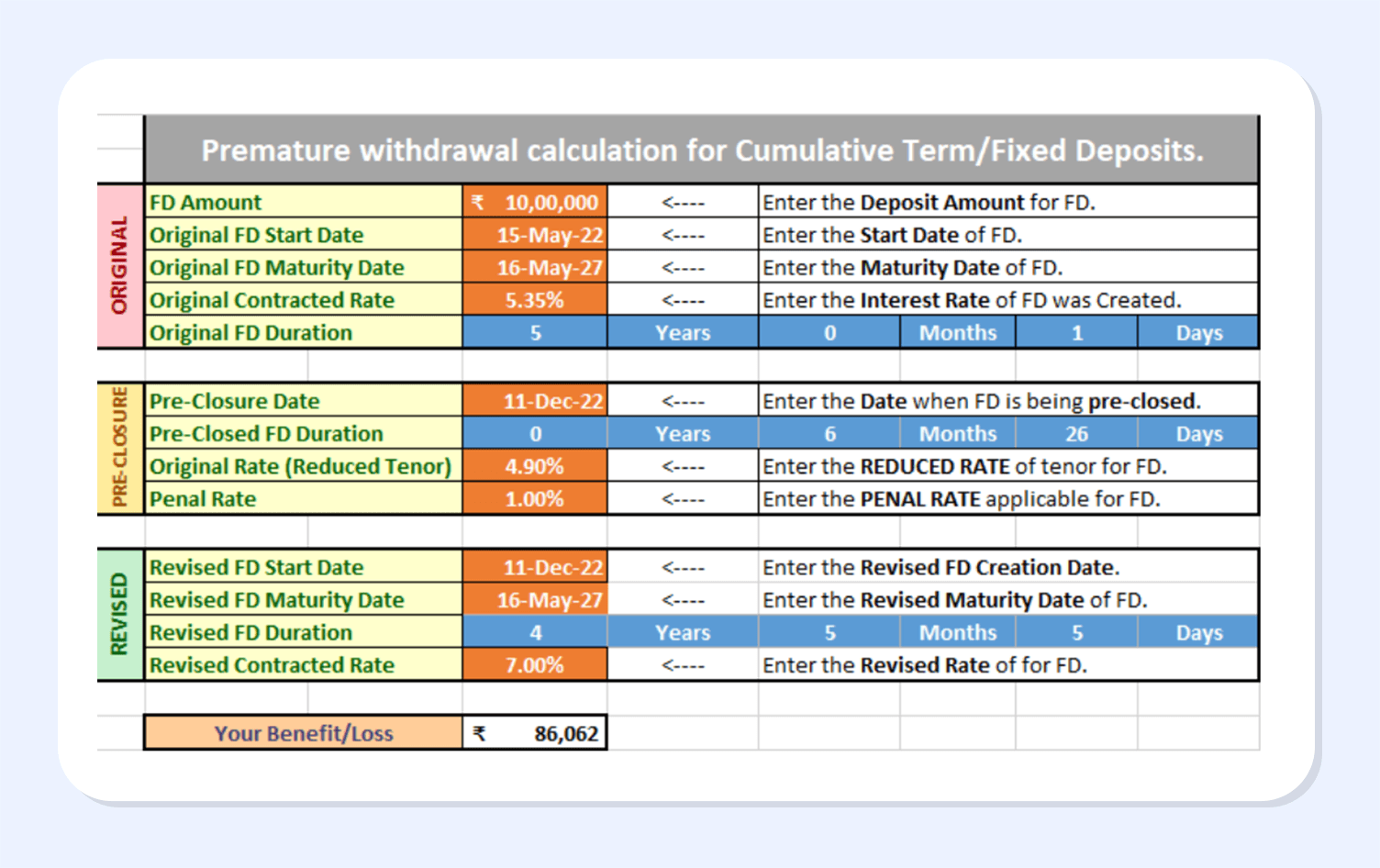

Premature FD closure simply means breaking your fixed deposit before the original maturity date chosen at the time of opening the deposit. Any full withdrawal of the FD amount before this agreed tenure is treated as premature closure by banks and NBFCs. Even if you have held the FD for a large part of the tenure, redeeming it even a day before maturity usually falls under this definition.

In most cases, premature closure triggers two key consequences: a lower interest rate and a penalty. Instead of the original contracted rate, the bank recalculates your interest at the rate applicable for the period actually completed, which is often lower. On top of that, many institutions apply a penalty margin (for example, 0.5%–1%) on the applicable rate, further reducing your effective return. Some special FDs, like certain tax-saver deposits, may not allow premature closure at all during the lock-in period, except in very specific cases such as the depositor’s death2.

Understanding what counts as premature closure is crucial, because even a seemingly small decision to break an FD early can significantly erode the returns you had planned for3. This is why it is important to know the penalty rules that apply when you withdraw an FD before maturity, which is what the next section will cover in detail.

Penalty Rules For FD Premature Withdrawal

When you opt for premature withdrawal of a fixed deposit (FD) in India, banks and NBFCs enforce specific penalty rules to protect their interest rate commitments and discourage early exits. These penalties typically involve two components: a reduced interest rate calculation and an additional penalty fee, ensuring your returns take a hit if you break the FD before maturity4.

How Penalties Are Calculated

Banks first recalculate interest based on the lower of your original contracted rate or the prevailing rate for the actual period the FD was held. For example, a 5-year FD at 7.5% withdrawn after 2 years might earn only the 6.25% rate applicable for 2-year tenures. On top of this, a penalty of 0.50% to 1% is deducted from the applicable rate5.

- Small deposits (under INR 5 lakh): Often 0.50%–0.75% penalty.

- Large deposits (INR 5 lakh+): Up to 1% penalty.

- No interest if withdrawn within 7 days of opening.

Partial withdrawals (e.g., up to 25%–50% of principal) may sometimes be penalty-free after a minimum holding period, like 3–6 months, but this varies by bank.

Bank-Specific Penalty Examples

Here is a comparison of common penalty structures (as of late 2025; always verify latest rates):

| Bank/NBFC | Penalty Rate | Key Conditions |

| SBI | 0.50%–1% | 1% for >INR 5 lakh; no penalty on death |

| HDFC Bank | 1% | After 7 days; partial up to 25% free after 3 months |

| ICICI Bank | 0.50%–1% | Higher for senior citizens sometimes waived |

| Bajaj Finance | 0.25%–1% | Depends on tenure completed |

| Axis Bank | 1% | No penalty on first partial withdrawal up to 25% |

Source: policy bazaar6

Tax-saver FDs (under Section 80C) are strictly non-withdrawable before 5 years, except in cases like depositor death or court orders. Senior citizens may get penalty waivers or higher rates, and some banks exempt penalties for tenures renewed into longer FDs.

Exceptions And Tips

No penalties apply in humanitarian cases (e.g., depositor's death, certified illness) or for bank staff FDs. To minimize losses, maintain a separate emergency fund and ladder your FDs across tenures. Always review your FD certificate or bank app for exact terms—rules differ slightly per institution and can change with RBI guidelines. Next, we will break down the key differences between full premature FD closure and partial withdrawals to help you choose wisely.

1. Alternatives to Breaking an FD

Breaking an FD early often costs 0.5–1% in penalties plus lower interest rates, but these alternatives preserve your principal and returns. Each provides liquidity without full closure, tailored for Indian investors facing emergencies or opportunities7.

2. Loan Against FD

Borrow up to 90–95% of your FD value as a loan, with your deposit as collateral—keeping it intact to earn original interest (typically 7–7.5%). Rates are 1–2% above FD rates: SBI charges 1% extra (e.g., 8.25% if FD is 7.25%), up to INR 5 crore; HDFC/ICICI offer 2% extra on 90% value (min INR 25,000 FD). No credit checks, processing fees nil at SBI, and flexible repayment suit short-term needs.

3. Sweep-in FDs

Link your savings account to an FD for automatic liquidity: excess balance (above threshold like INR 25,000–INR 1 lakh) sweeps into FD earning 6.5–7.5%, then sweeps back in INR 1–INR 25,000 units as needed—no penalties. HDFC uses LIFO (last in, first out) for breaks; Indian Bank multiples of INR 10,000–INR 25,000 for tenures 7 days–1 year. Ideal for irregular cash flows, maintaining FD returns on idle funds.

4. Liquid Funds

Park surplus in liquid mutual funds for 7–7.2% average 1-year returns (2025 data), beating savings accounts (3–4%) with T+1 redemption (instant up to INR 50,000). Top picks: Invesco India Liquid (7.17% 1Y), Groww Liquid (7.23% 1Y); low-risk via T-bills/CDs, expense ratios 0.1–0.2%. Minimal exit loads post-7 days, safer than equities for parking INR 1 lakh+ short-term8.

Grip: Blend these—e.g., 3-month emergency in liquid funds (7%+), ladder FDs with sweep-in, loan for big needs—to access INR 50,000–INR 5 crore flexibly while securing 7%+ yields vs. breaking FDs. Verify bank terms quarterly per RBI updates.

Also Read: Best Corporate FDs Of 2026

Conclusion

Premature FD withdrawal is often less about poor discipline and more about poor liquidity planning. Once you understand how penalties work, it becomes clear that breaking an FD should be the last option, not the first reaction. Smarter alternatives like loans against FD, sweep-in facilities, and liquid funds allow you to access cash without sacrificing hard-earned interest. What this really comes down to is building flexibility into your savings strategy so short-term needs do not derail long-term goals. Platforms like Grip Invest encourage this balanced approach by helping investors look beyond traditional FDs and explore regulated fixed-income options that offer better liquidity management while still prioritising safety and predictability

FAQs On FD Premature Withdrawal

1. How is premature FD penalty calculated?

Banks apply the lower of original or period-held rate (e.g., 6.5% for 1-year on 2-year FD), minus 0.5–1% penalty (1% for INR 5L+). Example: INR 1L at 7% for 1 year yields ~INR 5,500 after 1% cut, not INR 7,000.

2. Can tax-saving FDs be closed early?

No—5-year lock-in under Section 80C; premature withdrawal barred except depositor death (nominee/legal heir paid penalty-free).

3. Do senior citizens get penalty waivers?

Yes, many banks (e.g., RBL, public sector) waive 1% penalty for seniors, paying rate for actual tenure held.

4. Is FD loan cheaper than breaking FD?

Yes—loans cost 1–2% above FD rate (e.g., 8–9% vs. 7%), retaining full FD interest vs. penalty + rate cut loss.

References:

1. IndusInd bank, accessed from: https://indie.indusind.bank.in/indie/blogs/impact-of-premature-closure-on-your-fixed-deposit.html

2. Bajaj finserv, accessed from: https://www.bajajfinserv.in/investments/how-premature-withdrawal-of-fixed-deposits-affects-your-interest-calculation

3. Policy bazaar, accessed from: https://www.policybazaar.com/fd-interest-rates/articles/tax-saver-fd-premature-withdrawal/

4. Policy bazaar, accessed from: https://www.policybazaar.com/fd-interest-rates/articles/tax-saver-fd-premature-withdrawal/

5. Policy bazaar, accessed from: https://www.policybazaar.com/fd-interest-rates/articles/tax-saver-fd-premature-withdrawal/

6. Policy bazaar, accessed from: https://www.policybazaar.com/fd-interest-rates/articles/tax-saver-fd-premature-withdrawal/

7. Bank bazaar, accessed from: https://www.bankbazaar.com/fixed-deposit/premature-withdrawal-of-fixed-deposit.html

8. Policy bazaar, accessed from: https://www.policybazaar.com/fd-interest-rates/bank-of-india-fd-rates/fd-premature-withdrawal/

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks and shenanigans that take place in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001