What The New RBI Guidelines Mean For NBFC P2P Lending In India?

NBFC P2P lending platforms in India have experienced significant growth since their emergence in the last decade. According to industry estimates, the assets under management- AUM in the sector are expected to be INR 10,000 crore1.

To bring order to this fast-developing space, the Reserve Bank of India (RBI) established a regulatory framework in 2017. It classifies these platforms as a distinct category of non-banking financial companies or NBFCs.

However, as the industry grew, concerns arose around practices like guaranteeing returns and selling unrelated products. In response, on August 16-2024, the central bank introduced stricter measures to address these issues. This blog talks about the revised rules and their implications for the sector’s future.

Understanding Peer-To-Peer Lending Platforms

Peer-to-peer (P2P) lending platform connects individuals seeking loans with those willing to lend. Unlike banks, these online systems act as facilitators. Making sure the transactions are smooth without stepping into the role of a financial institution. They primarily handle the logistics and credit evaluations to ensure safety.

For those seeking loans, the appeal lies in the zero paperwork and instant disbursement compared to conventional options. Meanwhile, those offering capital are drawn to the prospect of better returns. Compared to what they might receive from traditional investment products. For example, the first RBI-registered P2P platform offers lenders returns of up to 12%. This rate is commonly seen across other platforms on average.

The platform assesses their profiles and categorises them by creditworthiness. From there, potential investors choose the profiles they find suitable, with the entire process — from disbursement to repayment — managed through the platform.

Overview Of RBI's Regulatory Reforms

The RBI’s regulations target a fast-growing sector that had 302 P2P lending startups in 2015. Currently, as of March 2024, there are 263 RBI-registered P2P NBFC platforms. These entities must act solely as intermediaries. They connect borrowers with lenders without recording the transactions on their own balance sheets.

To ensure only credible participants enter this market, prudential norms are mandated. Safeguarding data is essential. Additionally, cross-border transactions are restricted, and all transfers must occur directly between the parties involved. By placing these platforms under a formal NBFC structure, the RBI ensures a more transparent and regulated environment for alternative financing options.

Key Changes In The New RBI Guidelines For P2P

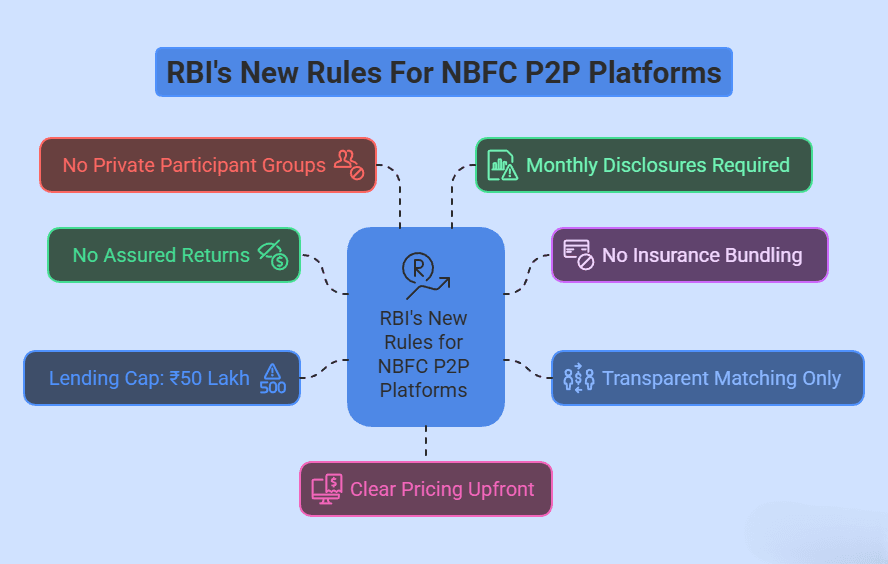

1. Prohibition of Assured Returns and Liquidity Options

The Reserve Bank has banned NBFC P2P lending platforms from promoting offerings with guaranteed returns tied to specific durations. It addresses misleading marketing that often masks the inherent uncertainty in peer-to-peer finance. Platforms now need to shift their approach, ensuring they accurately represent the risks involved. Eliminating liquidity options further reinforces this shift. It requires participants to reassess their expectations. Also, engage with the full spectrum of potential outcomes.

2. Limitations on Insurance Cross-Sales

The rules for P2P have also imposed restrictions on selling non-loan-related insurance. In particular, those linked to credit guarantees. The goal is to simplify the process by preventing the unnecessary addition of financial products. Which may confuse or complicate transactions. This ensures that P2P maintains a clear focus on their core function without veering into unrelated services.

3. Tighter Lender-Borrower Matching Policies

New regulations for NBFC P2P lending platforms call for a more structured and transparent process for connecting lenders and borrowers. Platforms must implement board-approved policies that guarantee fairness and clarity in these transactions. The prohibition of closed user groups aims to ensure inclusivity, preventing preferential treatment or restricted access. These measures aim to create a more open environment, encouraging equal opportunities for all participants.

4. Lending Limit

The rule enforces strict limits on how much money can be loaned through peer-to-peer networks. A single participant's exposure across these lending platforms is capped at INR 50 lakh. When a lender’s total contributions go beyond INR 10 lakh, they are required to submit a financial certificate. This document, verified by a Chartered Accountant, must confirm that the individual’s assets meet the minimum threshold of INR 50 lakh. These measures help ensure responsible participation and mitigate financial risks within the system.

5. Prohibition on Participant Matching

Connecting or linking individuals within a restricted group is strictly prohibited. This applies whether they are brought in through a third-party agency or any other method. For example, such a group could consist of borrowers or lenders introduced by affiliates or service partners of the NBFC-P2P.

6. Accurate Disclosure on Websites

The platforms must clearly display several key details on their website. According to recent guidelines, a thorough monthly report on portfolio performance is essential. This should include a breakdown of non-performing assets (NPAs) by age category. Lenders must be informed about any financial losses, whether related to principal or interest.

Additionally, a disclaimer needs to appear prominently on all websites, apps, and marketing materials. It should clearly state that the entity is registered with the Reserve Bank, which does not verify the accuracy of claims or guarantee loan repayments.

7. Pricing Policy

The pricing structure needs to be transparent. NBFC-P2Ps should clearly state all applicable charges at the point of lending. These can either be a specific amount or a set percentage of the loan principal. Importantly, these charges should remain unaffected by the borrower’s repayment behaviour.

Escrow Account Mechanism

RBI has implemented a detailed framework to manage fund flow on NBFC-P2P platforms. Each platform must maintain two distinct accounts:

- One handles the money coming from lenders before loans are issued.

- The other collects repayments from borrowers.

This structure ensures that financial operations remain transparent and free from misuse.

The guidelines emphasise strict separation. Money from the lenders' accounts cannot be redirected to pay off loans, and repayments from borrowers are not allowed to fund new loans. This clear division helps maintain accountability across the system. Additionally, a T+1 rule mandates that funds must be settled within one business day. Cash transfers are prohibited to ensure efficiency and prevent delays. All transactions must move through bank accounts. It further reinforces security and clarity within the P2P lending ecosystem.

With these new RBI regulations limiting liquidity and fund flexibility in P2P lending, investors may need more secure, regulated alternatives. Grip offers SEBI-compliant investment options designed to provide fixed returns with transparency and reduced risk.

Impact Of The New RBI Guidelines On The P2P Lending

One of the most notable shifts is the prohibition on advertising the NBFC P2P lending platform as a secure investment offering fixed returns. In response, several lending platforms have paused onboarding new clients. To ensure compliance with the revised standards. Investors who were attracted to the perceived safety of these options may now reconsider their involvement. It may lead to a recalibration in the way such services appeal to potential participants.

A significant change is the removal of the ability to sell active loans in the secondary market. Previously, this option provided liquidity and flexibility for those seeking early exits. Without this feature, transaction volume could see a decline, as participants face fewer opportunities for immediate returns. Additionally, the lending process might slow down, affecting both parties in the transaction chain.

The introduction of the T+1 settlement requirement adds a layer of operational complexity. Processing such frequent, small repayments increases the logistical burden on service providers, leading to concerns about higher costs and potential delays.

Conclusion

The new RBI guidelines for P2P lending platforms usher in tighter control over NBFC-P2P operations in India. The prohibition of guaranteed returns and liquidity options shifts the risk profile. It requires investors to approach P2P lending with a more cautious outlook. The removal of secondary market transactions limits early exits, which could reduce flexibility and liquidity.

However, the increased transparency and stricter oversight aim to create a safer, more stable environment. For those willing to adapt to this new landscape, P2P lending can still offer competitive returns, though with a clearer understanding of the associated risks.

Looking for a secure alternative to P2P lending? Explore Securitised Debt Instruments (SDIs) like LoanX and LeaseX by Grip, offering SEBI-compliant, fixed-income investments with reduced risk and greater transparency.

Frequently Asked Questions

1. What is the limit of P2P lending?

The Reserve Bank of India limits the total exposure of a lender to borrowers across all P2P platforms to INR 50 lakh. If a lender's total lending exceeds INR 10 lakh, they must provide a certificate from a Chartered Accountant. It should show a minimum net worth of INR 50 lakh. This helps maintain control over lending and ensures that lenders have sufficient financial backing.

2. Who bears risk in P2P lending?

In P2P lending, the lender bears the risk. If the borrower defaults on the loan, the lender may lose part or all of their money. P2P platforms act as intermediaries and do not take on the credit risk themselves. They simply connect borrowers and lenders. The platform's role is to facilitate the transaction and assess creditworthiness. However, the risk remains with the individual lender. It is important for lenders to be aware of this before investing.

3. Is P2P income taxable?

Yes, income earned from P2P lending is taxable. The interest earned by the lender is considered income and must be reported under "Income from Other Sources." It is taxed according to the lender's individual income tax slab rate. There are no specific exemptions for P2P lending income.

4. Why can’t NBFC-P2P platforms promise fixed returns anymore?

Because P2P lending carries credit risk, RBI regulations prohibit NBFC-P2P platforms from assuring fixed returns. Investors earn based on borrower repayments, not guaranteed income.

5. How does the escrow account system work for P2P lending?

All funds move through escrow accounts managed by a bank trustee. This ensures borrower repayments go directly to lenders, reducing fraud and mismanagement risk.

6. What happens if a lender’s total exposure crosses INR 10 lakh?

RBI caps individual lender exposure to INR 10 lakh across all P2P platforms. If exceeded, the platform must restrict further lending until the limit is maintained.

7. What are the disclosure requirements for NBFC-P2P platforms now?

Platforms must disclose borrower credit scores, default rates, and recovery details upfront. This improves transparency and helps lenders assess risks before investing.

8. Are NBFC-P2P platforms allowed to cross-sell insurance products?

Yes, but only with explicit RBI approval. Platforms cannot force-sell insurance and must ensure it directly supports lending activities like credit protection.

References

1. The Economic Times <https://economictimes.indiatimes.com/tech/technology/p2p-lenders-dial-rbi-for-secondary-market-access-instant-liquidity-options/articleshow/112144201.cms?from=mdr>

2. Reserve Bank of India <https://www.rbi.org.in/scripts/bs_viewcontent.aspx?Id=3164#3>

3. The Economic Times <https://economictimes.indiatimes.com/news/economy/policy/rbi-tightens-guidelines-for-nbfc-p2p-lending/articleshow/112573403.cms?from=mdr>

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001