Home Loan Tax Benefits Under Sections 80C And 24 Explained

Buying a home is the single largest financial commitment most Indian salaried professionals will ever make. A INR 50 lakh home loan at 8.5% over 20 years means paying nearly INR 52 lakh in interest alone — more than the principal itself.

What makes this burden manageable, and even strategically rewarding, is the robust set of home loan tax benefits embedded in the Indian Income Tax Act

For salaried taxpayers in the 30% bracket, the cumulative deductions available under Section 80C (principal repayment), Section 24(b) (interest payment), and Section 80EEA can together reduce taxable income by up to INR 5,00,000 per year — generating annual tax savings of up to INR 1,56,000 (including cess). Over a 20-year loan tenure, that's a potential saving of over INR 31 lakh.

This guide breaks down every major home loan tax deduction available in FY 2025-26, with worked examples, regime comparisons, and practical tips to help you maximise every rupee of benefit.

Principal Repayment Benefit: Section 80C

Under Section 80C of the Income Tax Act, 1961, the repayment of the principal component of your home loan EMI qualifies for a deduction of up to INR 1,50,000 per financial year. This falls under the overall Section 80C umbrella, which also includes instruments like ELSS, PPF, NSC, and life insurance premiums.

Section 80C – Key Facts

- Maximum Deduction: INR 1,50,000 per year (combined with other 80C investments)

- Applicable On: Principal portion of EMI paid during the year

- Property Type: Only for residential property (self-occupied or let out)

- Holding Condition: If sold within 5 years of possession, the deduction is reversed

- Loan Source: Must be from a bank, HFC, NHB, or approved institution

- Tax Regime: Available ONLY under the Old Tax Regime

Important Conditions

- The property must not be sold within 5 years of taking possession. If it is, all deductions claimed under 80C are added back to your income in the year of sale.

- The home loan must be from a recognised lender — not from friends, family, or private lenders.

- The deduction is available from the year in which the loan repayment begins (not during the construction phase).

- Stamp duty and registration charges paid during the year of purchase are also eligible for the INR 1,50,000 deduction under 80C, even without a loan.

Interest Deduction: Section 24(b)

- What Is Section 24(b)?

Section 24(b) allows a deduction on the interest paid on your home loan. This is separate from and in addition to the 80C benefit on the principal, making it a powerful second lever for home loan tax saving.

Section 24(b) – Key Facts

- Self-Occupied Property: Max deduction of INR 2,00,000 per year

- Let-Out Property: No upper limit — full interest paid is deductible

- Under-Construction Property: Interest during construction can be claimed in 5 equal instalments from year of possession

- Loan Purpose: Must be for purchase, construction, repair, or reconstruction

- Tax Regime: Available ONLY under the Old Tax Regime (with INR 2L cap for self-occupied)

Self-Occupied vs. Let-Out Property: A Key Distinction

For a self-occupied home, the maximum interest deduction under Section 24(b) is capped at INR 2,00,000 per year. However, if the property is let out (rented), there is no ceiling — you can deduct the entire interest paid. This makes a let-out property significantly more tax-efficient for high-value loans where interest payments easily exceed INR 2 lakh.

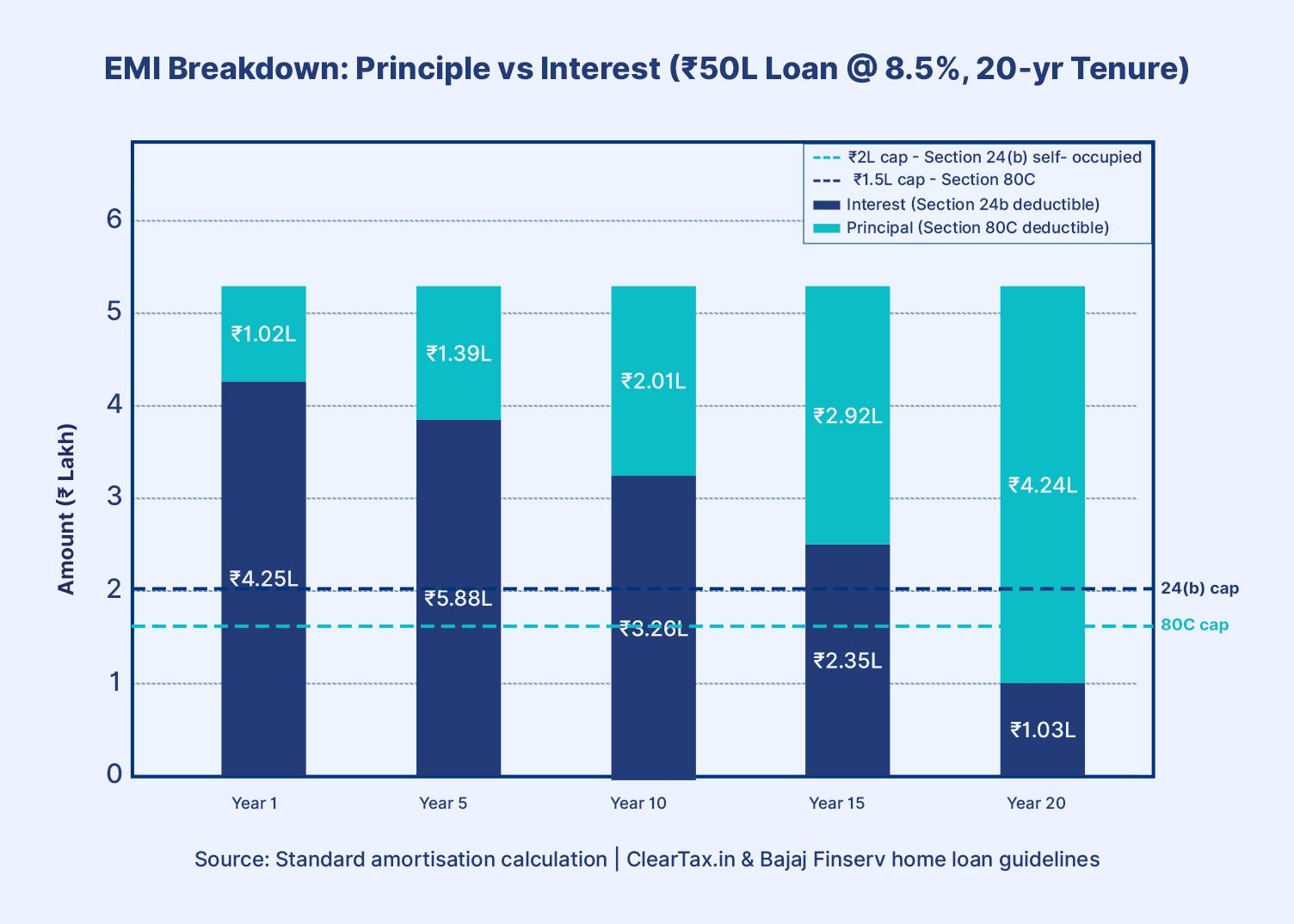

Chart 1: EMI Breakdown — Principal vs Interest Over Loan Tenure

Chart 1: EMI Breakdown — Principal vs Interest (INR 50L @ 8.5%, 20-yr) | Source: Standard amortisation calculation based on ClearTax.in & Bajaj Finserv home loan guidelines

In the early years, interest far exceeds the INR 2L Section 24(b) cap, meaning you lose significant potential deduction. This is why first-time buyers should also pursue Section 80EEA (explained in Section 4) to reclaim more of that interest benefit.

Additional Benefits For First-Time Home Buyers

Section 80EE: For Loans Sanctioned in FY 2016-17

Section 80EE provided an additional INR 50,000 deduction on interest paid, over and above Section 24(b), for first-time buyers. Eligibility: loan sanctioned between 1 April 2016 and 31 March 2017, loan value upto INR 35 lakh, property value upto INR 50 lakh. While no longer available for new loans, existing borrowers who qualified continue to claim it.

Section 80EEA: The Game-Changer for Affordable Housing

Section 80EEA was introduced in Budget 2019 and allowed an additional interest deduction of INR 1,50,000 per year — over and above the INR 2,00,000 under 24(b) — effectively raising the total interest deduction ceiling to INR 3,50,000 for eligible borrowers.

Section 80EEA – Eligibility Conditions

- Loan sanctioned between 1 April 2019 and 31 March 2022

- Stamp duty value of the property must not exceed INR 45 lakh

- Borrower must not own any other residential property on the date of sanction

- Must be a first-time home buyer

- Cannot be claimed simultaneously with Section 80EE

- Available only under the Old Tax Regime

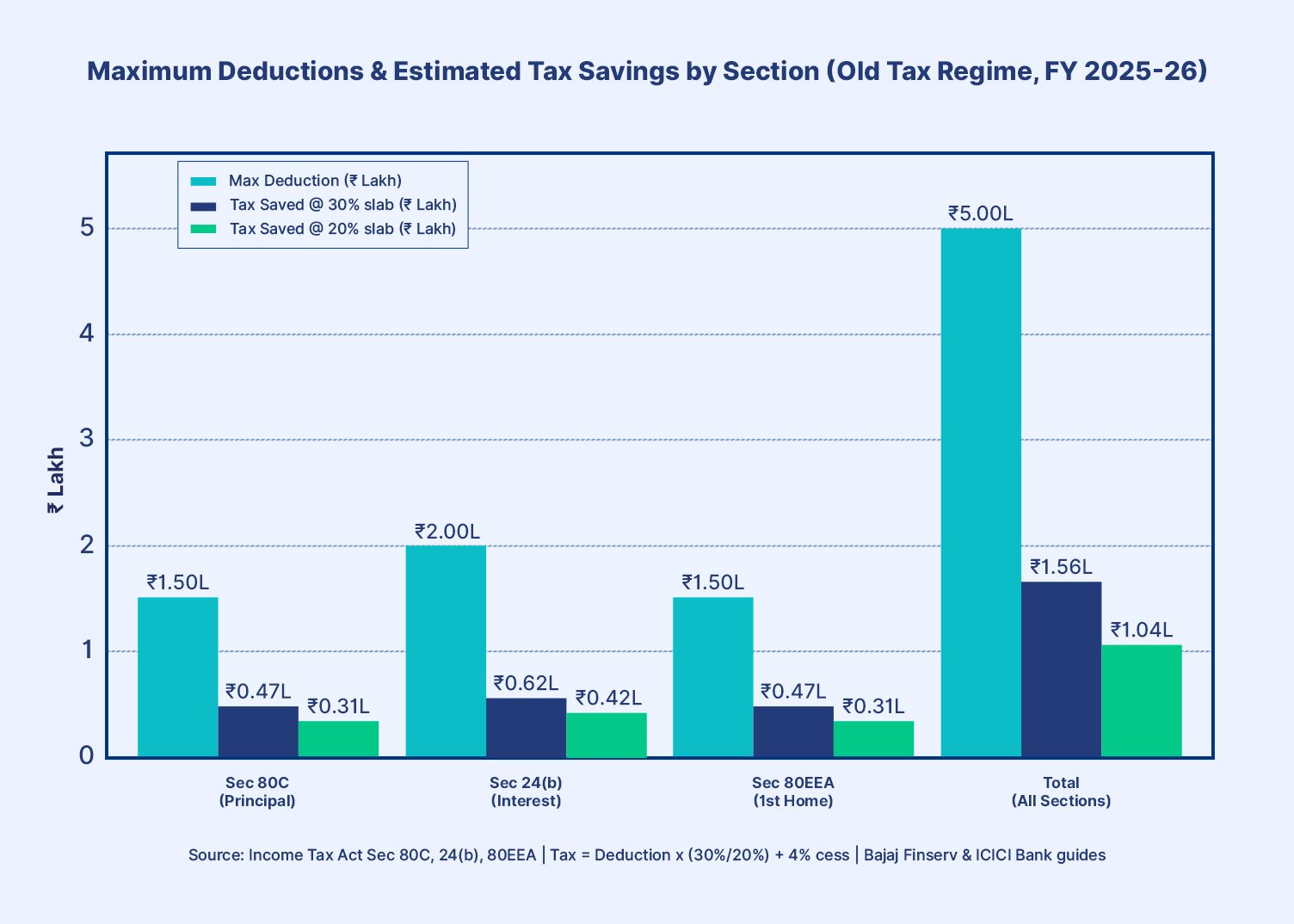

Chart 2: Maximum Deductions & Tax Savings by Section

Chart 2: Max Deductions & Estimated Tax Savings by Section (Old Tax Regime, FY 2025-26) | Source: Income Tax Act Sec 80C, 24(b), 80EEA | Tax = Deduction × slab rate + 4% cess | Bajaj Finserv & ICICI Bank guides

As per the above chart, Section 24(b) delivers the largest single-section saving — up to INR 62,400 annually at the 30% slab. A first-time buyer who also qualifies for 80EEA can stack an additional INR 46,800, making the total potential annual saving INR 1,56,000 — a compelling case for the Old Tax Regime.

| Section | Deduction Available | Amount Claimed (INR ) | Tax Saved @ 20%+cess |

| Section 24(b) – Interest | Up to INR 2,00,000 | 2,00,000 | INR 41,600 |

| Section 80EEA – Additional Interest | Up to INR 1,50,000 | 73,000 (balance) | INR 15,184 |

| Section 80C – Principal | Up to INR 1,50,000 | 1,50,000 | INR 31,200 |

| Total | INR 5,00,000 (max) | INR 4,23,000 | INR 87,984 |

Old Vs. New Tax Regime: Impact On Home Loan Tax Benefits

This is perhaps the most critical decision for any home loan borrower in FY 2025-26. The 2020 budget introduced a New Tax Regime with lower slab rates but without most deductions. Since Budget 2023, the new regime has become the default — but salaried taxpayers can opt out and choose the old regime each year.

| Feature | Old Tax Regime | New Tax Regime (Default) |

| Section 80C – Principal (INR 1.5L) | Available | Not Available |

| Section 24(b) – Interest (INR 2L) | Available | Not Available (self-occupied) |

| Section 24(b) – Let Out Property | Full interest deductible | Available (let-out only) |

| Section 80EEA (INR 1.5L add-on) | Available | Not Available |

| Standard Deduction (Salaried) | INR 50,000 | INR 75,000 |

| Best For | High deduction claimers | Lower income / fewer deductions |

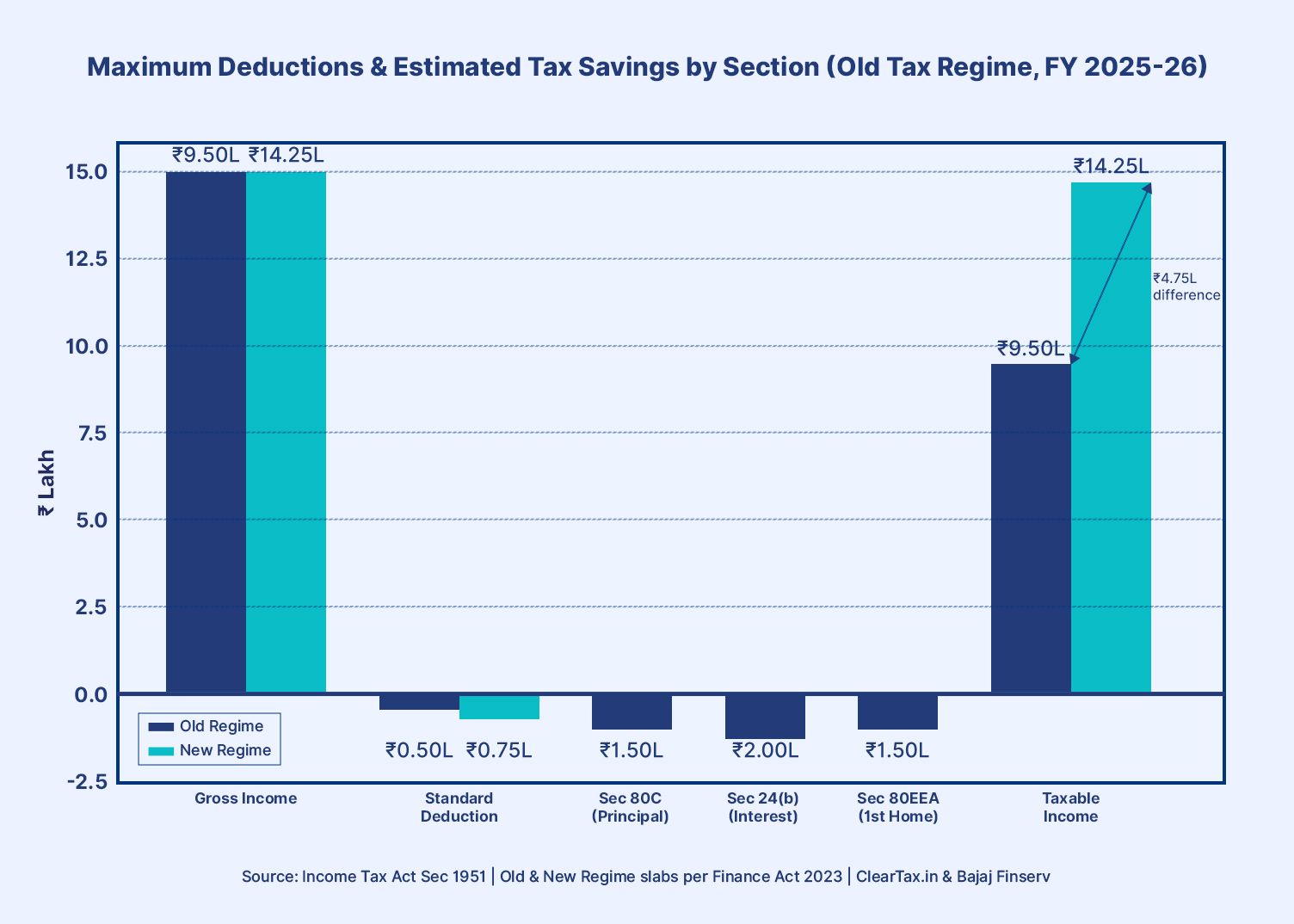

Chart 3: Old vs New Regime — Taxable Income Comparison

Chart 3: Old vs New Tax Regime — Income Adjustments for Home Loan Borrower (INR 15L Salary, FY 2025-26) | Source: Income Tax Act 1961 | Old & New Regime slabs per Finance Act 2023 | ClearTax.in & Bajaj Finserv

| Particulars | Old Regime (INR ) | New Regime (INR ) |

| Gross Income | 15,00,000 | 15,00,000 |

| Standard Deduction | 50,000 | 75,000 |

| Section 80C | 1,50,000 | NIL |

| Section 24(b) | 2,00,000 | NIL |

| Section 80EEA | 1,50,000 | NIL |

| Taxable Income | 9,50,000 | 14,25,000 |

| Tax + Cess (approx.) | 1,21,680 | 1,95,000 |

| Annual Savings vs. New Regime | INR 73,320 more savings | Baseline |

Conclusion

A home loan is not just a liability as it’s a smart tax-saving tool. By claiming deductions under Section 80C (principal) and Section 24(b) (interest), and Section 80EEA if eligible, you can reduce taxable income by up to INR 5 lakh annually under the Old Tax Regime. The key is planning your deductions and choosing the right tax regime.Once your tax savings create surplus cash, consider putting it to work. Platforms like Grip Invest, a SEBI-regulated investment platform, offer fixed-income and alternative investment options starting from INR 10,000 — helping you turn tax savings into long-term wealth.

FAQs

1. How much tax benefit on home loan can I claim in total?

Under the Old Tax Regime, you can claim up to INR 1,50,000 under 80C, INR 2,00,000 under 24(b), and an additional INR 1,50,000 under 80EEA if eligible — totalling INR 5,00,000 in deductions. At the 30% tax bracket (with cess), this translates to a maximum tax saving of approximately INR 1,56,000 annually.

2. Is home loan tax benefit available in the new regime?

Largely no. Under the New Tax Regime, deductions under Section 80C and Section 24(b) for self-occupied properties are not available. However, if your property is let out, you can still claim the actual interest paid under Section 24(b), subject to the INR 2,00,000 set-off limit against other income.

3. Can joint owners claim home loan tax benefits separately?

Yes. If a couple takes a joint home loan and both are co-owners, each co-borrower can independently claim deductions proportional to their share of the EMI — up to INR 1,50,000 under 80C and INR 2,00,000 under 24(b) each, effectively doubling the household's total deductions to INR 7,00,000 per year.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001