How To Gift A Fixed Deposit To Someone In India: A Complete Guide (2026)

In the past, marriages and events meant handing down Shagun in the form of crisp INR 500 notes in colored envelopes. This tradition catches on with less ever-changing drama. More people are trending away from cash to instruments that accrue value in the long run.

Fixed Deposits (FDs) have now come into their own as the preferred choice. Savings in the form of deposits within Indian households remain at 60% in 2025. This can be ascribed largely to perceptions of security as well as assured returns. So, how to gift an FD to someone? Well, an FD as a gift requires more policy-fork awareness.

If you wish to give a “safety net” to a person close to you, here is everything you need to know regarding the gifting of an FD in India.

Can You Gift A Fixed Deposit In India?

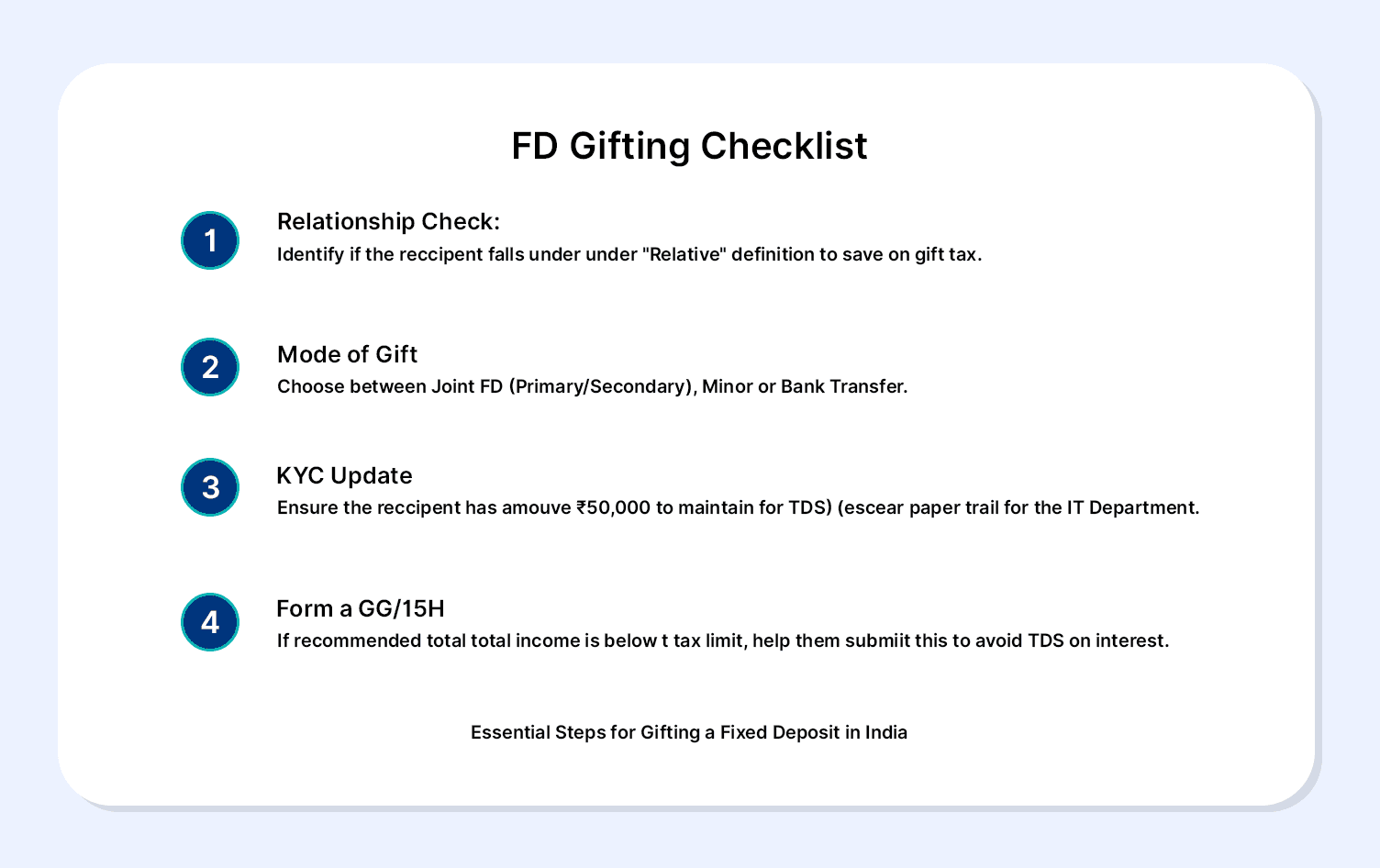

Yes, you can gift fixed deposit but with some conditions. You cannot transfer an existing FD account from your name to another person’s name as you would transfer your mobile balance. An FD is an agreement between a depositor and a bank. To understand how to gift a FD to someone, you generally need to:

- Open a New FD in the Recipient's Name: Directly depositing the funds into a new account.

- Add the recipient as a joint holder: Making a joint FD as gift where the recipient has operational rights.

- The transfer of funds: Moving money into the recipient's account so they can create the FD.

Ownership vs. Nominee: Many people misunderstand nomination for FD gifts to be a gift. A nominee is a beneficiary who is a custodian of cash in a trust account due to the death of the person who made the deposit; they are not the actual owners unless stated in a will. To truly gift financial products to India, you must give the beneficiary the right to its ownership during your lifetime.

Different Ways To Gift An FD

When you enquire “how to gift a FD to someone?” you will find that specific FD gift tax rules apply to different methods. Here are three alternate methods to transferring FD to another person:

1) Joint FD Route

Common among couples/partners or between parents and children. Open an FD account jointly with the beneficiary.

- Operating Mandates: Select “Either or Survivor” (trustees and executors allowed to operate) or “Former or Survivor” (only you will manage until your death).

- Tip: The main holder is responsible for the tax paid on interest for a joint FD. If you want the recipient to own it, you have to make him the main holder.

2) The Minor FD

FD gift from parents to children is a traditional Indian custom, often used for future education.

- Procedure: Open an FD in the minor’s name with you as guardian.

- Transition: Upon the minor's 18th birthday, the FD changes to “Major,” and the minor obtains full control.

3) Funding an FD in Someone Else’s Name

You can transfer the amount of the gift to the recipient's account, and they can open the FD. This is a popular choice for an FD as Raksha Bandhan gift, giving the recipient financial independence.

Case Studies: Real-Life Gifting Scenarios

Scenario A: The Wedding Gift (Non Relatives)

Rahul gifts FD worth INR 1,00,000 to his best friend, Vikram, on his wedding.

Result: Under Section 56 gift tax rules India, Income Tax Act, gifts regarding marriage are exempted as taxable income even if it is not a family member. Vikram is liable to pay taxes only on the interest portion.

Scenario B: The Spouse Safety Net (Clubbing Rules)

Example: Mr. Khanna (in the 30% tax bracket) gifts INR 10 Lakh FD to his homemaker wife to earn independent interest.

Result: The gift is tax-free (gift fixed deposit to spouse), but clubbing of income on FD gifts applies. The interest will be taxed in Mr. Khanna’s hand, not his wife’s, as per FD gift from spouse tax rules.

Situation C: The Major Child (Tax Efficiency)

For example: One parent gifts INR 5 Lakh to their 21-year-old daughter to open an FD.

Result: Since she is a Major, clubbing of income on FD gifts does not apply. The interest is liable to tax at her rate of slabs. If she does not earn any other income, she might not have to pay a penny of taxes on the interest she is earning. This makes it a highly tax-efficient method.

Note: As investors look for diversification, they increasingly turn to alternatives to bank FDs. Services such as Grip Invest allow individuals to explore the option of corporate bonds and other fixed-rate investments that could even make for a gifted investment.

Financial Gift Comparison: At A Glance

| Feature | Cash/Cheque | Fixed Deposit (FD) | Corporate Bonds |

| Liquidity | High | Moderate (Penalty on break) | Varies |

| Returns | None | Fixed (6.5% - 8.2%) | Often Higher than FDs |

| Tax on Gift | Exempt for relatives | Exempt for relatives | Exempt for relatives |

| Best For | Immediate needs | Stability/Milestones | Wealth Growth |

Things To Check Before Gifting An FD

In order to gift an FD, it

- Section 56(2)(x) Compliance: Gifting FD to family members (spouse, brothers and sisters, parents, lineal ascendants/descendants) are exempted from taxes. Gifts to non-relatives above INR 50,000 are liable to taxes.

- Income Clubbing: When gifts are made to a spouse or minor, be aware of the tax on gifted fixed deposit interest being added back to your income.

- Documentation: For valuable gifts, draft a gift deed for fixed deposit. This stamp paper document proves the transfer was voluntary, preventing future tax hurdles.

- TDS on FD interest: TDS will be deducted by the bank from the interest received on the fixed deposits if the interest amount exceeds INR 40,000 (INR 50,000 in the case of individuals above 60 years of age). It must be confirmed whether the beneficiary files form 15G/15H in case their

FAQs On How To Gift A Fixed Deposit To Someone

1. Can I gift an FD to someone else?

Yes, but you can not transfer an existing FD. You must open a fresh FD in their name with them as a joint account holder, gift them money to open one, etc.

2. Is gifted FD taxable?

A gift received from a “specified relative” and gifts received during a wedding are tax-free. Gifts received from friends and above INR 50,000 are taxed as “Income from Other Sources.”

3. Who pays tax on FD interest after gifting?

If a gift is made to an important child or a parent, then it is paid by the recipient as tax. When a gift is made to a spouse or to a minor, then as a rule, it is clubbed and paid as tax by the giver.

4. Is a gift deed mandatory when gifting a fixed deposit?

A gift deed is not legally mandatory for all FD gifts, but it is strongly recommended for high-value gifts to avoid future tax scrutiny or ownership disputes.

5. Can NRIs gift a fixed deposit to residents in India?

Yes. NRIs can gift money to resident Indians, who can then open an FD. However, the transfer must comply with FEMA rules and applicable tax provisions.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001