How To Open An FCNR Account Online: Eligibility, Documents And Step-by-Step Process

An FCNR account helps NRIs keep foreign earnings in foreign currency with an Indian bank. The full form is Foreign Currency Non-Resident Bank account, commonly called FCNR(B).

FCNR(B) is not a savings account. It is a term deposit, which means the money stays locked for a fixed period and earns interest as per the bank’s rate card.1

The account has gained fresh attention after the RBI’s recent foreign-currency measures brought FCNR(B) deposits back into public discussion. Banks can revise their rates depending on currency, tenure and market conditions.

FCNR(B) deposits must run for at least 1 year and cannot exceed 5 years. The deposit is held in permitted foreign currency. This helps NRIs avoid converting overseas savings into INR immediately.

How to open FCNR account? The online opening process can vary across banks. Some banks allow existing NRI customers to book FCNR deposits through NetBanking. Others may first ask the applicant to open an NRE or NRO account, complete KYC and then place the FCNR deposit.

Eligibility To Open FCNR Account

An FCNR(B) deposit can be opened by an NRI or a Person of Indian Origin. RBI also treats an Overseas Citizen of India cardholder who lives outside India as a PIO for this purpose.

The account is mainly useful for people who earn abroad and want to keep part of their savings in foreign currency with an Indian bank.

An FCNR(B) deposit can usually be opened:

- In the name of one eligible NRI, PIO or OCI

- Jointly with another eligible NRI, PIO or OCI

- Jointly with a resident relative on a “former or survivor” basis, where permitted

- Through fresh inward remittance from abroad

- Through funds already available in an NRE or existing FCNR account

The joint holding rule needs careful reading. If a resident relative is added, the resident cannot operate the account in the same way as the primary NRI depositor. The arrangement works only under the permitted mode.

New NRI customers should also check whether the bank allows an end-to-end service to open an FCNR account online. In many cases, the FCNR booking becomes easier after the customer already has an active NRE account with completed FCNR KYC requirements.2

Documents Required For FCNR Account Opening

The exact document list for the FCNR account opening process differs by bank. Still, most banks ask for the same core details because they need to confirm identity, NRI status, overseas address and tax declarations.

Requirement | FCNR eligibility documents |

Identity proof | Valid passport |

NRI status proof | Visa, work permit, residence permit or OCI card |

Overseas address proof | Utility bill, overseas bank statement, residence card, driving licence or employer letter |

Indian address proof, if available | Aadhaar, voter ID, driving licence or other accepted document |

Tax details | PAN or Form 60 |

Photograph | Recent passport-size photograph |

Declarations | FATCA, CRS and bank-specific forms |

Deposit request | FCNR deposit application form or online deposit instruction |

Source: RBI,3

RBI’s FCNR KYC requirements framework recognises officially valid documents such as a passport, driving licence, proof of possession of an Aadhaar number, voter ID, NREGA job card, and National Population Register letter.

For an NRI, the passport and overseas status document carry particular weight. Banks may also ask for attested copies if the person is applying from outside India. Attestation rules differ, but banks may accept attestation by an Indian embassy, overseas branch of an Indian bank, notary or authorised official.

How To Open FCNR Account Online?

The steps below give a general online NRI account opening journey. The process may look different across banks, but the broad sequence remains similar.

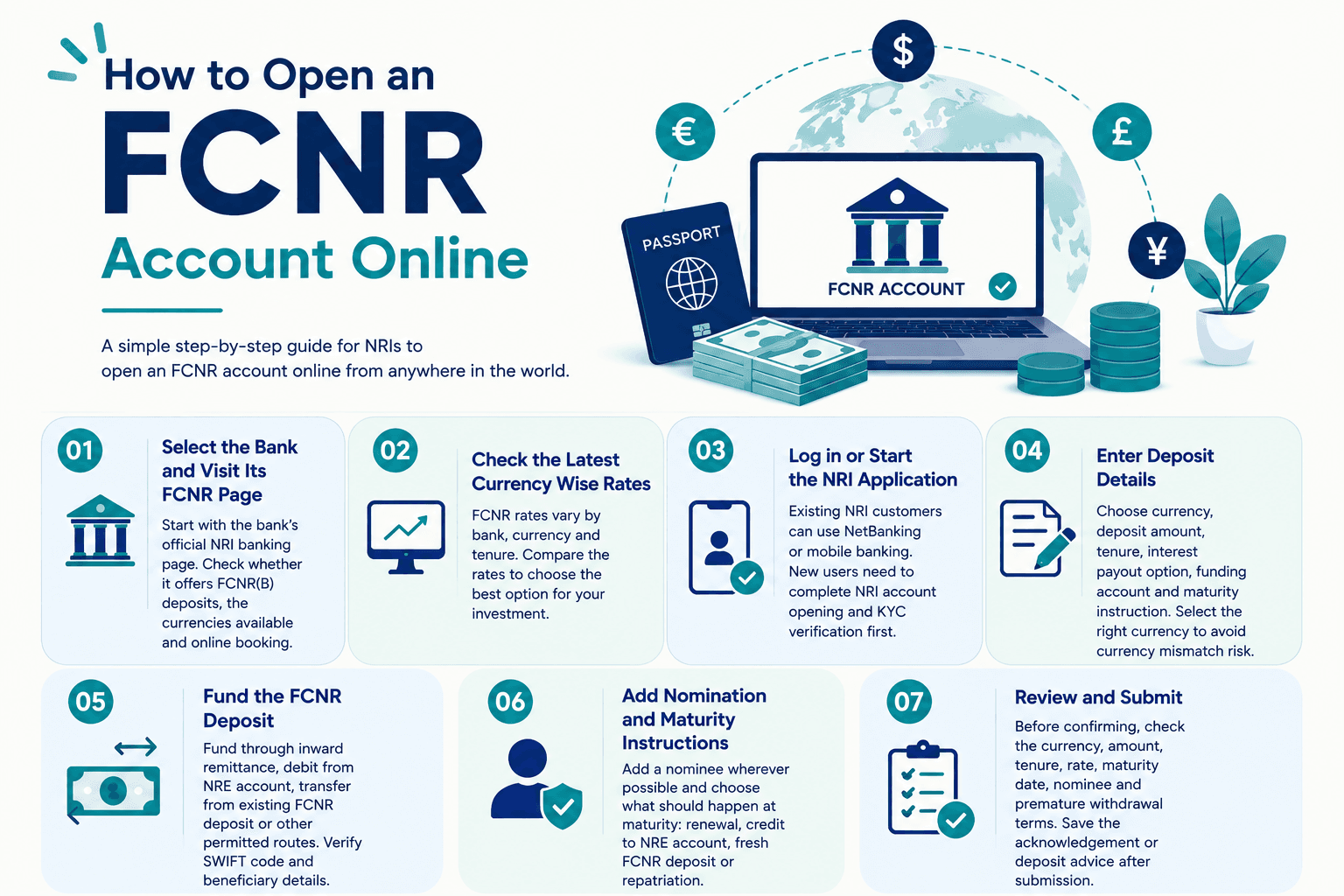

Step 1: Select the bank and visit its FCNR page

Start with the bank’s official NRI banking page. Check whether it offers FCNR(B) deposits, the currencies available and whether online booking is possible.

Step 2: Check the latest currency wise rates

FCNR rates are not uniform. They change by bank, currency and tenure. For example, one bank may offer deposits in USD, GBP, EUR, CAD, AUD and JPY, while another may offer fewer currencies.

Step 3: Log in or start the NRI application

Existing NRI customers can often proceed through NetBanking or mobile banking. For example, the process might look like: Accounts > Transact > Open FCNR FD > Fill in required details > Confirm.

New customers may need to begin with NRI account opening, upload KYC documents and wait for verification before placing the deposit.

Step 4: Enter deposit details

The FCNR deposit form will usually ask for currency, deposit amount, tenure, interest payout option, funding account and maturity instruction.

Choose the currency with care. A higher rate in another currency may not help if your income and future expenses are mainly in USD or GBP. Currency mismatch can quietly reduce the benefit.

Step 5: Fund the FCNR deposit

Banks may allow funding through inward remittance, debit from NRE account, transfer from existing FCNR deposit or other permitted routes.

If you remit money from abroad, check the SWIFT code, beneficiary details, purpose code and correspondent bank details. A small error can delay the credit.

Step 6: Add nomination and maturity instructions

Add a nominee wherever the bank allows online nomination. Then choose what should happen at maturity: renewal, credit to NRE account, fresh FCNR deposit or repatriation.

Step 7: Review and submit

Before confirming, check the currency, amount, tenure, rate, maturity date, nominee and premature withdrawal terms. Save the acknowledgement or deposit advice after submission.

Choosing The Right FCNR Account

The right FCNR account is not just the one with the highest rate. The better question is whether the currency, tenure and withdrawal terms match your money plan.

Factor | What to check |

Tenure | Minimum 1 year and maximum 5 years |

Currency | Match it with income, savings or future spending needs |

Rate | Compare bank-wise, currency-wise and tenure-wise rates. For example, HDFC Bank lists 6% p.a. for USD FCNR deposits of 3 years to 5 years, effective June 10, 2026.4 |

Minimum deposit | This varies across banks and currencies. For example, SBI lists USD 1,000, GBP 1,000, EUR 1,000, CAD 1,000, AUD 1,000 or JPY 100,000 as the minimum deposit.5 |

Tax treatment | Interest may be exempt under Section 10(15)(iv)(fa), subject to conditions.6 |

Repatriability | Principal and interest are generally repatriable |

Premature withdrawal | Penalty and interest rules vary by bank. For example, HDFC Bank says no interest is paid if the FCNR deposit is closed before 1 year.7 |

Renewal | Check maturity and overdue renewal instructions |

The tax point deserves care. FCNR interest is generally exempt in India for eligible non-residents and resident but not ordinarily resident individuals or HUFs under Section 10(15)(iv)(fa), subject to the conditions in the law.

However, Indian tax exemption does not automatically mean tax exemption in the country where the NRI lives. A US, UK, UAE, Singapore or Canada-based NRI should check local reporting rules separately.

Also read the premature withdrawal terms before booking. RBI allows banks to levy premature withdrawal penalties as per their board-approved policy. That means the charge, or even the interest impact, can differ from one bank to another.

Common Mistakes While Opening FCNR Account

The first mistake is assuming that all banks follow the same online process. They do not. One bank may allow instant FCNR booking for existing NRI customers, while another may need forms, document checks or branch coordination.

The second mistake is choosing only by rate. Rate matters, but currency matters more. A deposit in the wrong currency can expose the NRI to avoidable conversion risk later.

Avoid these common errors:

- Treating FCNR as a savings account instead of a term deposit

- Ignoring the 1-year minimum and 5-year maximum tenure rule

- Not checking the latest official rate page before applying

- Missing PAN, Form 60, FATCA or CRS details

- Uploading unclear passport or visa copies

- Using an incorrect remittance route or SWIFT detail

- Forgetting nomination and maturity instructions

- Assuming premature withdrawal rules are the same across banks

- Believing Indian tax exemption covers overseas tax rules as well

A final caveat is useful. Do not depend only on relationship manager messages or social media screenshots. FCNR rates and terms can move quickly, especially when banks revise foreign-currency deposit offerings.

An FCNR account can be a practical option for NRIs who want to keep foreign earnings in foreign currency while banking in India. The key is to verify the rules, choose the right currency, read the withdrawal terms and save all application records before funding the deposit.

Conclusion

Opening an FCNR(B) account can help NRIs manage overseas earnings while keeping their deposits in a foreign currency with an Indian bank. Since it is a term deposit and not a regular savings account, understanding the tenure, currency options, interest rates, tax rules and withdrawal conditions is important before investing.

The FCNR account opening process has become simpler with online banking options, but requirements can differ across banks. Before booking a deposit, NRIs should compare available currencies, check the latest rates, verify eligibility and ensure all KYC documents are updated.

A well chosen FCNR(B) deposit can offer convenience, currency flexibility and a structured way to hold foreign earnings in India. However, reviewing both Indian regulations and the tax rules of the country of residence is essential before making a decision.

FAQs On How To Open FCNR Account Online

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001