Interest Coverage Ratio In Corporate FDs: Why Investors Should Check It

Corporate fixed deposits may seem attractive due to their comparatively higher returns than bank FDs. But higher returns come with higher risks. Before committing your hard-earned money to any corporate FD, there is one critical metric you must understand: the interest coverage ratio in corporate FD issuers.

This single number can reveal whether a company can comfortably meet its debt obligations or is teetering on the edge of financial distress. Let us decode this essential financial indicator.

What Is Interest Coverage Ratio

The interest coverage ratio meaning is simple. It measures how many times a company can pay its interest obligations using its operating profits. The interest coverage ratio formula is equally simple:

ICR = EBIT ÷ Interest Expense

Where EBIT is Earnings Before Interest and Tax, the company's operating profit before accounting for interest payments and taxes.

Let us examine real examples to understand this calculation and its implications:

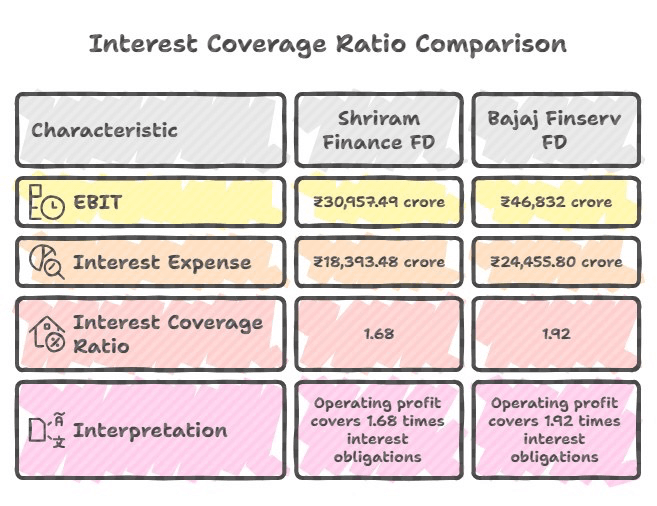

Example 1: Shriram Finance FD

Based on Shriram Finance's FY2025 financial statements1:

- EBIT: INR 30,957.49 crore

- Interest Expense: INR 18,393.48 crore2

- Interest Coverage Ratio = INR 30,957.49 ÷ INR 18,393.48 = 1.68

This calculation reveals a concerning picture. An ICR of 1.69 means Shriram Finance's operating profit covers 1.68 times of its interest obligations.

Example 2: Bajaj Finserv FD

Based on Bajaj Finance's (the lending arm of Bajaj Finserv) FY 2024 financials:

- EBIT (Operating Profit): INR 46,832 crore3

- Interest Expense: INR 24,455.80 crore4

- Interest Coverage Ratio = INR 46,832 ÷ INR 24,455.80 = 1.92

This ICR of 1.92 indicates that Bajaj Finance generates operating profits 1.92 times its interest obligations. The company earns INR 1.92 for every INR 1 it must pay in interest.

An ICR of at least 2 or 3 times+ is often considered a good interest coverage ratio for NBFC FDs.

Why Interest Coverage Ratio Matters For Investors

The interest coverage ratio in corporate FD evaluation is an early warning system for potential financial distress. Understanding why this metric matters can protect your capital.

- Measures Ability to Repay Debt

The fundamental purpose of ICR is to assess debt servicing capacity. When you invest in a corporate FD, you are lending money to the company. Your returns depend entirely on the company's ability to generate sufficient cash flow to pay interest and return your principal.

A company with an ICR of 3.0 generates three times the profit needed to cover interest payments. Even if business conditions deteriorate and profits drop by 50%, the company still comfortably meets its obligations. On the other hand, a company with an ICR of 1.2 operates with minimal cushion; a 20% profit decline could trigger debt servicing difficulties.

- Indicator of Financial Health

Beyond immediate debt servicing, ICR reveals broader financial health patterns. Consistently declining ICR over multiple quarters signals deteriorating business performance or increasing debt burden. Either scenario raises red flags for corporate FD safety.

March 2024. IL&FS, which defaulted on its obligations affecting thousands of investors, showed steadily declining ICR in the years preceding its collapse. Investors who monitored this metric had early warning signs, though many ignored them while chasing the company's attractive FD rates.

The ratio also indicates management's financial prudence. Companies maintaining healthy ICR demonstrate disciplined borrowing and effective capital allocation. Those with perpetually low ICR may be overleveraged or operating in structurally challenged industries.

Interpreting Interest Coverage Ratios

Understanding what is a good interest coverage ratio requires industry context and comparative analysis.

1. ICR above 2-3: Generally considered healthy for traditional corporates. The company generates a comfortable surplus beyond interest obligations.

2. ICR between 1-5-2: Acceptable but requires monitoring. The company meets obligations but has a limited cushion for downturns.

3. ICR between 1.0-1.5: Concerning territory. The company barely covers interest from operating profits, leaving minimal room for error.

4. ICR below 1.0: Red flag. The company cannot cover interest from operations and may be using reserves or additional borrowing to meet obligations.

The ideal ICR for corporate FD safety varies significantly across sectors. Capital-intensive industries like infrastructure or real estate typically operate with lower ICR than technology or pharmaceutical companies.

NBFCs may show lower ratios due to their business model of borrowing to lend.

Evaluating Fixed Income Investments

While ICR is a critical component, comprehensive credit risk analysis extends beyond it.

Before investing in any corporate FD, evaluate multiple dimensions for interpreting ICR for company deposits:

1. Interest Coverage Ratio: As discussed, this measures immediate debt servicing capacity

2. Credit Ratings: CRISIL, ICRA, and CARE ratings incorporate ICR along with other factors

3. Debt-to-Equity Ratio: Indicates overall leverage levels

4. Current Ratio: Measures short-term liquidity

5. Return on Equity: Reflects profitability and efficiency

6. Industry Position: Market share and competitive advantages

The challenge for retail investors lies in accessing and interpreting this financial data. Company annual reports contain the necessary information, but extracting and analysing it requires financial literacy and time investment.

Many modern investment platforms, such as Grip Invest, have emerged to address this complexity. These platforms conduct comprehensive corporate FD risk analysis on behalf of investors. They feature only companies meeting stringent financial health criteria, effectively pre-screening investment options.

While this doesn't eliminate risk entirely, it significantly reduces the probability of investing in financially distressed companies.

Conclusion

The interest coverage ratio in corporate FD is your first line of defence against potential defaults. While chasing higher returns remains tempting, understanding whether a company can comfortably service its debt obligations protects your hard-earned capital from unnecessary risk. Remember, the best investment is not always the one offering the highest rate, but the one that reliably returns your money with the promised interest.

FAQs On Interest Coverage Ratio In Corporate FDs

1. What is the interest coverage ratio?

The interest coverage ratio measures how many times a company can pay its interest obligations using operating profits, calculated as EBIT divided by interest expense.

2. What is a good interest coverage ratio?

A good ICR typically exceeds 2 for traditional corporates, indicating comfortable debt servicing capacity.

3. Why is it important for corporate FD investors?

ICR reveals whether a company can reliably meet debt obligations. Strong ICR reduces default risk, protecting your principal and ensuring timely interest payments on corporate FDs.

References:

1. MoneyControl, accessed from: https://www.moneycontrol.com/india/stockpricequote/finance-leasinghire-purchase/shriramfinance/STF

2. CDN, accessed from: https://cdn.shriramfinance.in/sfl-kalam/files/2025-06/Shriram_Finance-AR-2024-25.pdf

3. MoneyControl, accessed from: https://www.moneycontrol.com/india/stockpricequote/finance-nbfc/bajajfinance/BAF

4. CMS, accessed from: https://cms-assets.bajajfinserv.in/is/content/bajajfinance/annual-report-fy-2025pdf?scl=1&fmt=pdf

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks and shenanigans that take place in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001