List Of Allowed Expenses In Income Tax: Complete Guide To Deductible Business Expenses

Managing taxes isn't just about filing returns on time; it's about knowing how to legally reduce what you owe. Many business owners and professionals often pay more tax than they need to, simply because they are not aware of the expenses they are allowed to claim. Understanding deductible expenses can turn routine spending into valuable tax-saving opportunities.

Knowing what costs are allowed as expenses helps you to plan wiser, keep your records straight, and remain compliant with the tax laws. Understanding these rules helps you avoid penalties and ensures maximum savings and an increase in general financial health, thereby making tax management less stressful and more strategic.

So, read this blog till the end to get an in-depth insight into the list of allowed expenses in income tax.

What Are the Allowed Expenses Under Income Tax?

Allowed expenses under income tax refer to the costs you incur in running your business or profession that you can legally deduct from your taxable income. These will be crucial in reducing your overall liability for taxation and enhancing financial efficiency.

- Deductible Expense Definitions

Deductible expenses include all necessary and reasonable expenditures directly related to earning an income from a business or professional activity. Examples of such expenses are rent, salaries of employees, office supplies, utility bills, travel expenses, and marketing charges. The main purpose of such expenses must be related to business rather than personal.

- Conditions for Claiming Deductions

Taxation authorities allow the deductions because they realise that income cannot be derived if there are no operational costs invested in it. To qualify for a deduction, certain requirements need to be satisfied.

- First, the expense has to be incurred exclusively or wholly for purposes of business or profession. It is worth noting that normally, personal expenses or those incurred partly for personal use may be claimed if there is an identifiable component that can be easily recognised.

- Second, the expense has to be incurred genuinely, with evidence of bills, invoices, or even receipts.

- Relatedly, it is essential that the expense be incurred in an actual financial year. It is against tax laws to deduct expenses incurred in advance or those that belong to another period.

- Lastly, it has to be compliant with tax laws.

Major Categories Of Allowed Expenses

Taxpayers can understand the need for different categories of deductible costs. It helps them manage their resources and claim benefits accordingly. There is a need to provide a list of allowable expenses for income tax. It will help business owners and professionals identify these allowable expense categories for their workforce management activities.

- Business Operating Expenses

Business operating expenses refer to those expenses that are required to operate a business smoothly. These expenses generally entail office rent, electricity expenses, internet costs, stationery, repair costs, marketing costs, transportation costs, and professional fees.

These costs can be regarded as allowable expenses while calculating income tax in India since they are correlated with income generation. These costs may be documented, thereby becoming part of allowable business expenses in India.

- Employee-Related Expenses

The term 'employee-related expenses' refers to the expenses incurred on hiring and retaining employees. Such expenses include salaries, wages, bonuses, provident fund contributions, training costs, and staff welfare.

Any of these expenses comes under the valid business expense deductions category according to the 'expenses under the Income Tax Act of India,' provided the expenditures are genuine, and the receipts are maintained.

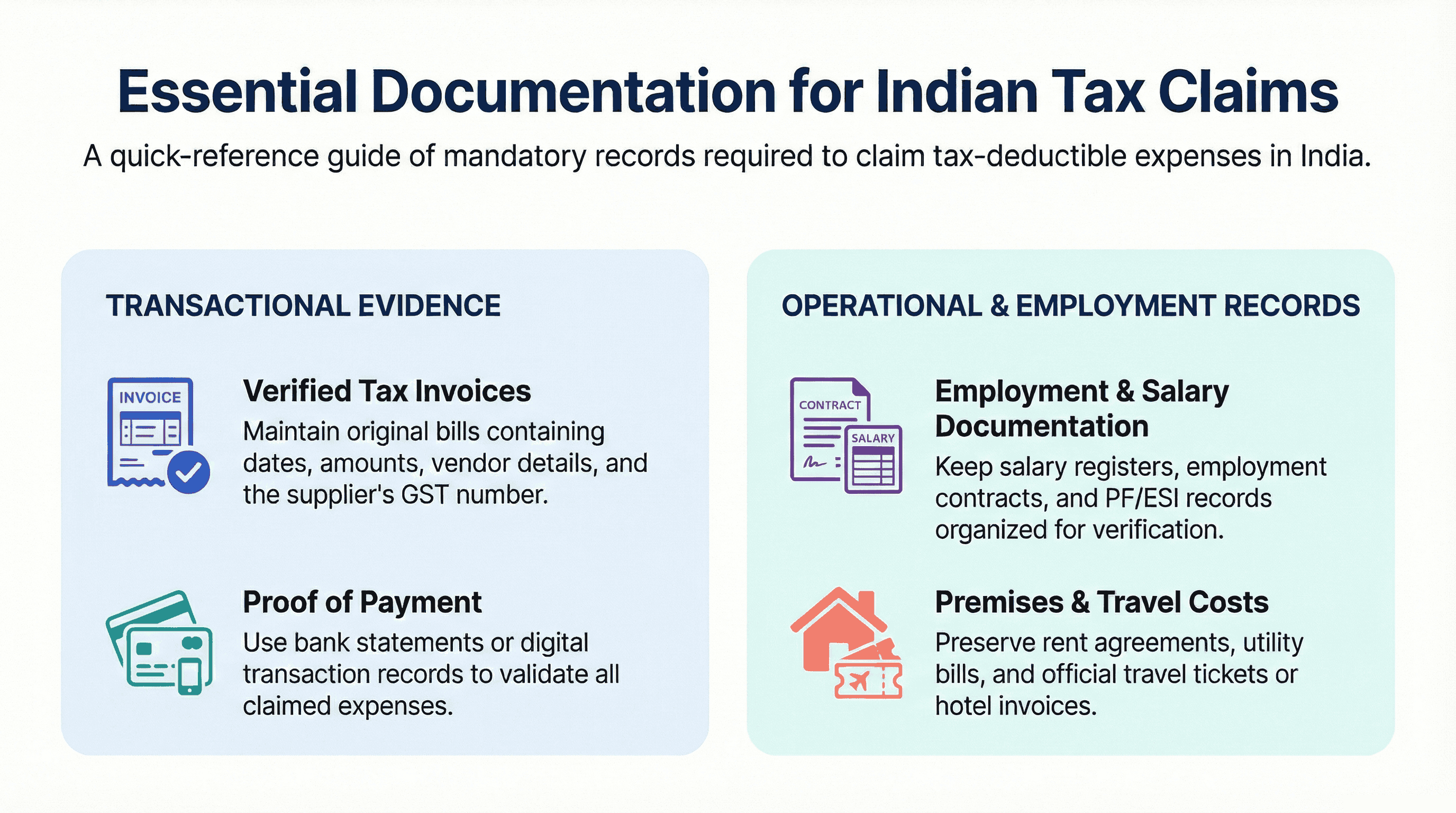

Documentation Required To Claim Expenses

It is valuable to correctly document your records to correctly state your allowed costs in your income tax filing. Even legitimate business deductions can be disallowed if these records are not properly evidenced under the corresponding income tax law.

Invoices and Proof Requirements

To claim allowable expenses for income tax in India, an individual should maintain proper, verifiable records. It is always helpful in ensuring the smooth processing of your tax returns.

- Original bills and tax invoices with date, amount, and vendor details

- The GST number of the supplier, if applicable

- Proof of payment through bank statements or digital transactions

- Salary register, employment contract, and PF/ESI records

- Rent agreements, bills for utilities at business premises, etc.

- Travel Tickets and Hotel Bills from Official Trips

Common Mistakes Taxpayers Make

Inaccurate documentation can cause rejected business expense deductions in India. The following are a few things to avoid in your documentation:

- Claiming expenses without proper proof

- Mixing personal and business spending

- Inability to maintain consistent records

- Claiming of expenses not included under the expenses covered under the Income Tax Act of India

- Not reconciling accounts before filing returns

Optimising Expense Claims Efficiently

The management of expense claims can help reduce financial stress, increase transparency, and facilitate the timely processing of expense claims throughout the year.

Strategies for Expense Tracking

Keeping digital records and scanning invoices regularly will help in tracking expenses and avoiding the loss of important documents. Budgeting apps are useful when allocating funds on a monthly basis, while the categorisation of expenses will facilitate control.

- Maintain digital copies of all bills and receipts for easy access.

- Review monthly spending to identify unnecessary expenses.

- Use budgeting or expense-tracking apps for better monitoring.

- Categorise expenses to simplify reimbursement and tax filing.

Planning Deductions During the Financial Year

Smart tax deductions planning allows individuals to save more by aligning expenses with legal benefits.

Category | Eligible Expense | Best Time to Plan | Benefit |

Medical | Health Insurance Premium | April–June | Tax savings |

Education | Tuition Fees | July–September | Deduction under law |

Housing | Home Loan Interest | Year-round | Reduced taxable income |

Investments | October–January | Long-term savings |

Conclusion

When you understand which expenses you are allowed to claim, you stop overpaying taxes and start managing your money smarter. So, ensure you keep your records clean, plan your deductions in advance, and stay compliant with tax rules. If you stay organised and informed, you will save more and avoid unnecessary tax trouble.

However, keep in mind that investments play a crucial role in efficient tax filings. So, it would be advisable that you regularly invest your savings through trustworthy brokers or investment platforms. One such platform is Grip Invest. It is an intuitive alternative investment platform that allows you to start investing with just INR 1000.

FAQs

1. What expenses are allowed under income tax?

Expenses that are wholly and exclusively incurred for running your business or profession are allowed under income tax. These typically include rent, salaries, electricity bills, internet charges, travel for business, marketing costs, professional fees, and other operational expenses directly related to earning income.

2. Can personal expenses be claimed as deductions?

No, purely personal expenses cannot be claimed as business deductions. However, if an expense is partly personal and partly business-related (for example, phone or vehicle use), you can claim only the business portion, provided you maintain proper records to justify it.

3. What documents are required to claim expenses?

You should maintain original bills, tax invoices, payment proofs (bank statements or digital transactions), salary records, rent agreements, utility bills, and travel tickets. Proper documentation is essential, as expenses without valid proof may be disallowed during assessment.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001