FD Vs PPF: Which Is Better For Long-Term And Tax-Efficient Savings?

Introduction: Why FD Vs PPF Is A Common Dilemma

For conservative Indian investors, the FD vs PPF debate has almost become a rite of passage in financial planning. Fixed Deposits (FDs), also known as term deposits, and the Public Provident Fund (PPF) are often the first investment options individuals encounter in their financial journey.

This is largely driven by recommendations from family members, employers, or trusted advisors. Both instruments have earned widespread acceptance for their safety, stability, and low volatility.

However, as financial awareness deepens, particularly when taxation begins to significantly influence net wealth creation, many investors start reassessing these long-held assumptions.

Rising income levels, reduced tax efficiency of traditional debt instruments, and increasing life expectancy have prompted a critical question: Are FDs sufficient on their own to meet long-term financial goals?

As a result, the discussion around FD vs PPF: which option is better for long-term, tax-efficient savings, has become increasingly relevant for today’s investors.

Also Read: What Are VPF Tax Benefits?

FD Vs PPF: Key Differences

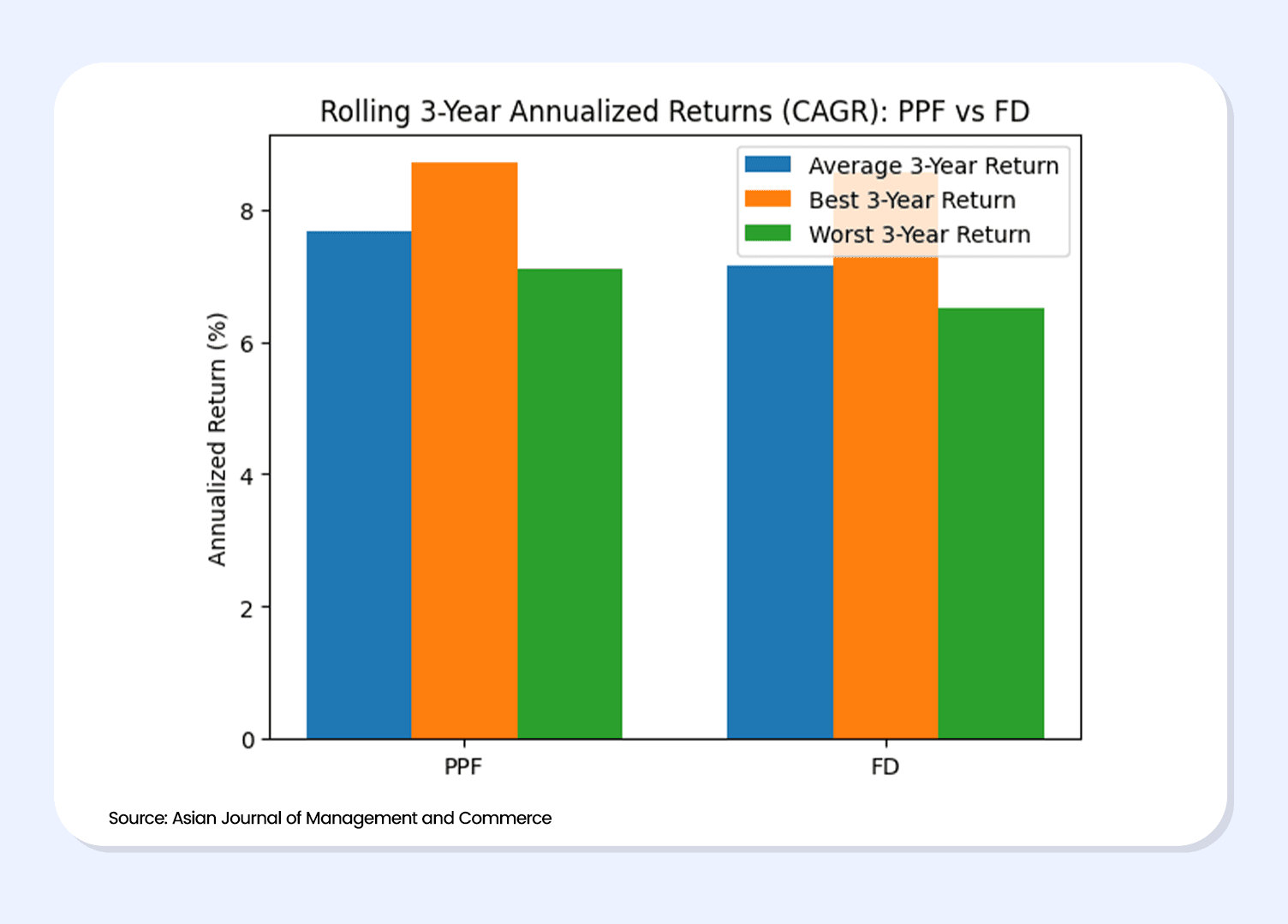

For an insightful comparison of the value of a Fixed Deposit (FD) vs Public Provident Fund (PPF), the performance of both under various time and taxation scenarios needs to be assessed.

1. Returns Predictability

The FD provides certainty about the time period, but the risk for the long-term investor is the possibility of having to reinvest at a lower interest rate if rates fall after maturity.

When comparing FD vs PPF while the PPF rate is not fixed, it receives long-term rate smoothing by the government, making it predictable in the long term to long-term investors.

2. Liquidity

PPFs have long lock-in periods. FDs can be withdrawn earlier, subject to penalties. Hence, from the perspective of liquidity, Fixed Deposits have a slight edge over the PPFs.

On the positive side, PPF’s lock-in mechanism ensures financial discipline, preventing people from withdrawing money impulsively and promoting regular savings. Hence, if the long-term perspective on behavioural discipline is considered, PPFs are a better choice.

3. Tax Treatment

The difference between tax benefits on FD vs PPF becomes all the more important as the number of years, or say investment periods, stretches out. Tax on interest on FD will affect the interest that compounds each year, whereas in PPF, compounding continues unbroken and tax-free for 15 years and above.

Parameter | Fixed Deposit (FD) | Public Provident Fund (PPF) |

Risk | Low | Sovereign (Very Low) |

Returns | Fixed, issuer-dependent | Govt-declared |

Current Avg Returns | 6%–7.5% | 7.1% |

Tax on Returns | Fully taxable | Tax Free |

Lock-in | Flexible | 15 years |

Liquidity | High | Restricted |

Section 80C | Only for tax-free FD Products | Full eligibility |

Ideal For | Short-term needs | Long-term wealth |

For example, assume an investor contributes INR 1 lakh annually for 15 years:

- FD (7%, 30% tax): Effective return - 4.9%

- PPF (7.1%, tax-free): Effective return - 7.1%

After 15 years:

- FD corpus ? INR 27–28 lakh

- PPF corpus ? INR 34–35 lakh

This large difference graphically demonstrates that the difference in interest rates between PPF and FD has more significance than the actual PPF vs FD interest rates charged.

Also Read: What Is City Compensatory Allowance: Are You Eligible?

Which Option Suits Different Investors?

Let’s understand how you can choose between FD vs PPF for various investors.

1. Short-term vs Long-term goals

- Early investors: The PPF helps investors cultivate the habit of saving while reducing their tax expenditure.

- Mid-career individuals: A combination of PPF for retirement and FD accounts for liquidity.

- Retirees: FDs can be preferred if there is a cash-flow requirement, although PPF can be used to increase tax-free income if opened before retirement.

2. Tax Savings Needs

Let’s now compare the FD vs PPF tax benefits. For taxpayers holding investments in the higher tax brackets, the returns offered by the PPF are always better than those of FDs after taxation, solidifying the product’s reputation as one of the leading means of tax saving investments in India.

While assessing the PPF vs fixed deposit safety, the fact that PPF has the backing of the Government of India has made it much more trusted by investors than fixed deposits. In this regard, although fixed deposits are quite safe, they are subject to certain risks related to the financial credibility of the bank or NBFC issuing them.

In the case of fixed deposits, deposits are insured for up to INR 5 lakhs per bank, which may be a concern for those with significant fixed deposit balances. Looking ahead at the likely comparison between PPF and FD returns in 2026, there may be several structural trends at play, such as tax implications, effective return on investment, and the ability of an investment to beat inflation.

Also Read: Best Corporate FDs Of 2026

Beyond FD And PPF: Exploring Predictable Income Alternatives

In this best tax saving FD PPF comparison, with them being the building blocks, they don't have to be mutually exclusive. Government-backed or investment-grade corporate bonds offer steady returns with clearly defined terms, which in many cases prove highly efficient from a post-tax perspective.

Modern platforms like Grip Invest enable investors to discover such opportunities online, thereby filling the gap between conventional savings products and market-linked debt instruments.

While choosing an emergency fund or planning for medium to long term, whilst avoiding all possible risks, fixed deposits are still relevant. However, if you are looking for long-term goals, compounding benefits, and financial discipline, PPF is an excellent investment.

FAQs on FD vs PPF

1. Is PPF safer than FD?

Yes. The PPF has a sovereign guarantee, but the security of an FD relies on the bank as well as deposit insurance limits.

2. Which yields better returns: FD or PPF?

On a post-tax basis over longer time periods, PPF tends to provide higher effective returns.

3. Can I invest in both FD and PPF at the same time?

Yes. Many investors use FDs for liquidity and short-term needs while using PPF for long-term, tax-efficient wealth creation.

4. Does FD interest affect compounding over the long term?

Yes. Since FD interest is taxed every year, the amount available for compounding reduces, lowering effective long-term returns compared to tax-free options like PPF.

5. Is PPF suitable if I already have other tax-saving investments under Section 80C?

It can still be useful. PPF not only offers tax deductions under Section 80C but also provides tax-free maturity and long-term discipline, making it valuable beyond just tax saving.

Reference:

Asian Journal of Management and Commerce, accessed from: https://www.allcommercejournal.com/article/677/6-2-123-981.pdf

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities are subject to risks. Read all the offer-related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading. This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip Invest”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip Invest or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip Invest does not guarantee or assure any return on investments and accepts no liability for the consequences of any actions taken based on the information provided. For more details, please visit https://www.gripinvest.in/.

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001.