VPF Tax Benefits Explained: How Voluntary Provident Fund Helps Reduce Taxes

Successful retirement planning requires an optimal taxability consideration. Various long-term tax-saving options in India, such as the Voluntary Provident Fund (VPF), Employees’ Provident Fund (EPF), and others, offer investors the opportunity to earn significant yield and tax benefits. However, unlike EPF, investors can invest a higher corpus in VPF, resulting in greater tax benefits.

The VPF serves as a low-risk tax-saving option that offers investors EEE (Exempt Exempt Exempt) status, under which the contributions, interest, and withdrawals are tax-free, given certain conditions. This blog decodes the VPF tax benefits and other nuances of this investment medium to aid optimal investment decisions.

What Is A Voluntary Provident Fund (VPF)?

Before exploring the VPF tax benefits, understanding the meaning of VPF is integral.

The Employees Provident Fund Scheme, which is administered by EPFO, can be expanded into the Voluntary Provident Fund. The contribution made to the provident fund account beyond the regular 12% contribution towards EPF of an employee is called Voluntary Provident Fund1.

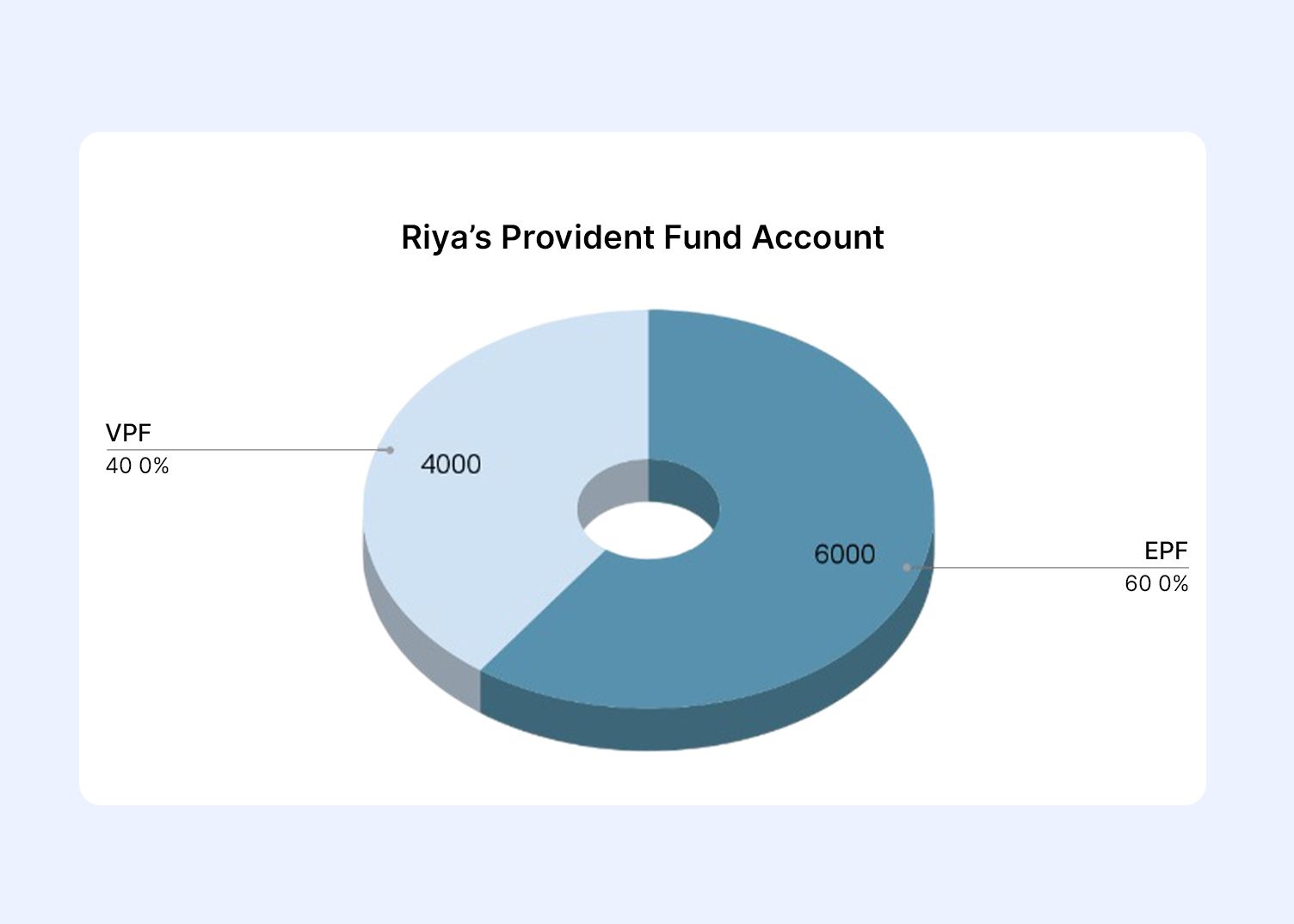

For example, Riya earns INR 50,000 (basic pay) per month. Under the EPF rules, 12% of her basic pay, that is INR 6,000, is the mandatory EPF contribution. However, Riya makes an additional contribution of INR 4,000 per month, making her total provident fund balance INR 10,000. This extra contribution of INR 4,000 is called VPF.

As the name implies, contributions to this optional provident fund are entirely optional and can extend up to 100% of basic salary and dearness allowance. Moreover, the interest earned on VPF is similar to EPF, since it is simply an additional contribution made over and above EPF in the same provident fund account. Currently, for FY 2024-25, the interest rate stands at 8.25%2.

Furthermore, similar to EPF, the voluntary provident fund tax exemption benefits can be used for successful retirement planning. However, there are certain caveats and limits that investors must consider to claim VPF tax benefits.

VPF Tax Benefits Under Section 80C

Although investors can contribute any amount, up to 100% of their basic salary and dearness allowance, as VPF to the provident fund account, there are some limitations as per the Provident Fund Tax Rules India. These limitations must be followed to claim the VPF tax benefits. Listed below are the limitations.

- If the total contribution to the provident fund account, including both EPF and VPF, exceeds INR 5 lakhs in the case of no employer contribution, the interest earned becomes taxable3.

- In case both employee and employer contributed to a provident fund account, but the total contribution made by the employee (including the EPF and VPF) exceeds INR 2.5 lakhs, the interest earned becomes taxable.

- Moreover, if the provident fund balance is withdrawn before 5 years, the total income computation is made as if the fund is not recognised from the beginning.

- Furthermore, section 80C deductions are applicable for contributions up to INR 1.5 lakhs4. Therefore, 80C benefits cannot be claimed if an investor contributes a greater amount.

Therefore, with these conditions in mind, investors can plan their VPF contributions efficiently to claim the employee provident fund tax benefits. Now, let us analyse VPF taxability to understand how it reduces tax burden on investments.

Tax Treatment Of VPF Interest And Maturity

Contributions, interest, and withdrawals from a Voluntary Provident Fund may be tax-free since it is classified as an EEE (Exempt Exempt Exempt) asset. Discussed below is a detailed explanation of VPF tax benefits5.

- VPF Contributions Taxability: According to the VPF tax deduction under 80C, contributions up to INR 1.5 lakhs are tax-deductible.

- VPF Interest Taxability: Interest earned on VPF contributions is tax-free, depending on the limitations discussed in the previous section. It was in the Budget 2021 that interest earned on contributions above INR 2.5 lakhs was made taxable6.

- VPF Withdrawal Taxability: The final maturity amount is also tax-free if the withdrawal is made after 5 years of opening the PF account.

However, similar to VPF, other tax-saving investment options are available as well. Investors must comparatively analyse these options to optimally curate their portfolio.

VPF Vs Other Tax-Saving Investments

The table below compares VPF with PPF, ELSS, and tax-saving fixed deposits to help investors efficiently curate a portfolio.

| Parameters | VPF | PPF | ELSS | Tax-Saving FD |

| Full Form | Voluntary Provident Fund | Public Provident Fund | Equity-Linked Savings Scheme | Tax-Saving Fixed Deposit |

| Meaning | Voluntary contribution exceeding the EPF mandatory limit in the provident fund account held with EPFO | Long-term saving and investment scheme, backed with government guarantee | A diversified equity mutual fund that offers wealth creation, along with tax-saving opportunities. | A fixed deposit scheme that offers tax-saving features. |

| Section 80C7 | Applicable up to INR 1.5 lakh contribution | Applicable up to INR 1.5 lakh contribution | Applicable up to INR 1.5 lakh contribution | Applicable up to INR 1.5 lakh contribution |

| Tenure | To be eligible for tax advantages, it must be kept for a minimum of 5 years | It matures 15 years after the completion of the fiscal year in which it was created8. | It has a lock-in duration of 3 years9 | The lock-in duration is 5 years10 |

| Interest or Returns | In FY 2024-25, the interest is 8.25% | Between 1 April 2020 and 31 March 2026, the interest is 7.1%11 | As of 9 February 2026, the 3-year category average return has been 17.11%12 | Interest varies from one bank to another |

Diversifying Beyond Traditional Tax-Saving Products

The primary EPF vs VPF tax benefits lie in the fact that investors can contribute a greater amount to their provident fund account, exceeding the mandated EPF level, through VPF. However, the tax benefits of PF contributions might come at the expense of capital appreciation. Subsequently, investors might prioritise portfolio diversification to create a balance between tax-saving, capital growth, and stability.

Therefore, along with tax-saving options, investors can also consider allocations into fixed-income assets like corporate bonds or high-yield FDs that can offer stability with growth. Grip houses a range of corporate bonds, along with other assets, that can offer up to 12.5% yield to maturity.

Conclusion

The Voluntary Provident Fund remains one of the most efficient long-term tax-saving instruments for salaried investors who want to strengthen their retirement corpus while enjoying predictable, government-backed returns. With its EEE tax status, disciplined contribution structure, and relatively attractive interest rates compared to many traditional fixed-income options, VPF can play a meaningful role in a retirement-focused portfolio. However, investors should remain mindful of contribution limits, taxation rules on higher deposits, and the importance of balancing tax-saving instruments with growth-oriented investments to achieve well-rounded financial planning.

Alongside traditional tax-saving avenues, investors can also explore fixed-income opportunities such as curated corporate bonds available on Grip Invest , helping diversify portfolios while aiming for stable income potential.

FAQs On VPF Tax Benefits

1. Is VPF eligible for tax deduction under Section 80C?

Yes, a Voluntary Provident Fund (VPF) is eligible for deductions under section 80C if contributions made do not exceed INR 1,50,000.

2. Is VPF interest taxable?

No, VPF interest is tax-free provided that the total contribution of the employee made in the provident fund account, including EPF and VPF, does not exceed INR 2.5 lakhs.

3. What is the maximum tax benefit from VPF?

A Voluntary Provident Fund comes under the EEE (Exempt Exempt Exempt) category, meaning its contributions, interest, as well as withdrawals, are tax-free, provided certain conditions are met. Withdrawal must not be made within 5 years of creating the PF account, contributions should not exceed INR 1.5 lakhs to claim 80C benefits, and the total contribution in the PF account should not exceed INR 2.5 lakhs to claim tax-free interest.

References:

1. PNB, accessed from: https://tinyurl.com/45hxhfw6

2. EPF India, accessed from: https://tinyurl.com/yc73fpry

3. Income tax India, accessed from: https://incometaxindia.gov.in/tutorials/77.taxability-of-retirement-benefits.pdf

4. Income tax India, accessed from: https://incometaxindia.gov.in/_layouts/15/dit/pages/viewer.aspx?grp=act&cname=cmsid&cval=102120000000037018&searchfilter=&k=&isdlg=1

5. Income tax India, accessed from: https://incometaxindia.gov.in/tutorials/77.taxability-of-retirement-benefits.pdf

6. TOI, accessed from: https://timesofindia.indiatimes.com/business/india-business/cheer-for-middle-income-salaried-class-vpf-limit-for-tax-free-interest-may-be-hiked-from-rs-2-5-lakh/articleshow/114533244.cms

7. Income tax India, accessed from: https://incometaxindia.gov.in/_layouts/15/dit/pages/viewer.aspx?grp=act&cname=cmsid&cval=102120000000037018&searchfilter=&k=&isdlg=1

8. NSI, accessed from: https://www.nsiindia.gov.in/(S(tlgyhlybk53cp4jlnlnih0rh))/InternalPage.aspx?Id_Pk=55

9. SBI, accessed from: https://www.sbisecurities.in/blog/what-are-elss-mutual-funds-how-to-invest-in-elss-funds

10. ICICI, accessed from: https://www.icici.bank.in/personal-banking/blogs/deposits/fixed-deposits/tax-saving-fixed-deposits

11. NSI, accessed from: https://www.nsiindia.gov.in/(S(j1lznd55rwfmzajjcrp1iw55))/InternalPage.aspx?Id_Pk=178

12. Morning star, accessed from: https://www.morningstar.in/tools/mutual-fund-category-performance.aspx

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001